교통안전 시장 : 제공 제품별, 전개 모델별, 시행 유형별, 데이터 유형별, 용도별, 최종사용자별, 지역별 - 예측(-2030년)

Road Safety Market by Offering (Traffic Control, ANPR, ALPR, Incident Response, Enforcement, Smart Signals, RSUS, Sensors, Cameras, AI, ML, Analytics), Application (Accident Prevention, Work Zone Safety, Violation Management) - Global Forecast to 2030

상품코드:1797405

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 380 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

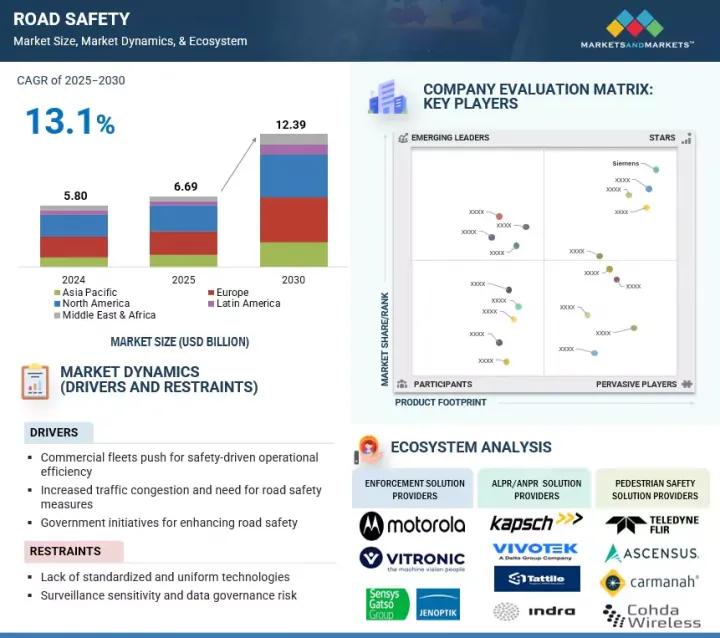

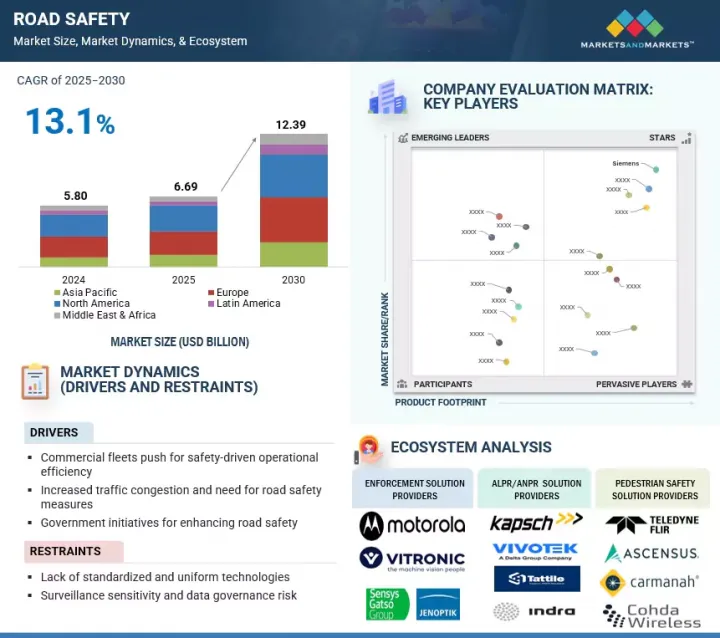

교통안전 시장 규모는 급속하게 확대되고 있으며, 2025년 66억 9,000만 달러에서 2030년에는 123억 9,000만 달러로 확대되고, 예측 기간 중 연평균 복합 성장률(CAGR)은 13.1%를 나타낼 전망입니다.

사고 비용을 줄이고, 자산을 보호하고, 규제를 준수하기 위해 현재 차량 사업자들은 교통 안전에 초점을 맞추었습니다. 그 결과, 운전자 행동 모니터링, AI 대시 캠, 텔레매틱스, 피로 감지 솔루션 등의 기술 채택률이 빠르게 증가하고 있습니다.

조사 범위

조사 대상 연도

2020-2030년

기준연도

2024년

예측 기간

2025-2030년

검토 단위

달러(100만 달러)

부문

제공 제품별, 전개 모델별, 시행 유형별, 데이터 유형별, 용도별, 최종사용자별, 지역별

대상 지역

북미, 유럽, 아시아태평양, 중동 및 아프리카, 라틴아메리카

첨단 안전기술에 대한 접근성과 함께, 업무용 차량은 현재 운전자의 책임감 향상, 보험료 할인, 전반적인 효율성 향상 등의 혜택을 누리고 있습니다. 그 결과, 차량에 맞게 조정된 교통 안전 솔루션에 대한 수요가 증가하여 전체 교통 안전 시장의 성장과 혁신을 촉진하고 있습니다.

교통안전 기술에는 큰 개선 가능성이 있지만, 모니터링 방법의 기밀성 및 데이터 관리와 관련된 위험에 대한 우려가 커지면서 시장 확대의 큰 억제요인으로 작용하고 있습니다. AI가 탑재된 카메라, 자동 번호판 인식, 운전자 모니터링 시스템의 보급으로 공공의 감시와 데이터 프라이버시에 대한 우려에 대한 검토가 진행되고 있습니다.

정부 기관과 지방 자치 단체는 교통 안전 솔루션을 광범위하게 채택하고 있습니다. 그들은 인식 개선 프로그램부터 종합적인 안전 인프라 및 단속 시스템의 관리 및 배포에 이르기까지 모든 것을 감독하는 데 큰 역할을 담당하고 있습니다. 그들은 교통 안전 시장에서 매우 중요하며, 규제와 안전 정책의 시행자로서의 역할을 하고 있습니다. 자금을 지원하고 프로그램을 개발함으로써 공공의 안전에 큰 영향을 미칠 수 있습니다. 정부 기관과 지자체는 법 준수를 단속하고 인프라 구축에 필요한 예산을 배분할 책임이 있습니다.

도로의 신호등과 표지판 관리, 적신호 및 과속 단속을 위한 카메라 배치, AI를 활용한 위반 근절, 실시간 교통관리 시스템 도입 등을 하고 있습니다. 2024년 11월, 캐나다 브램턴시는 Jenoptik과 협력하여 스쿨존 준수율을 높이기 위해 180대 이상의 자동 과속 단속 카메라를 도입했습니다.

사고 감지 및 대응 부문은 교통 안전 시장의 중요한 부분으로 부상자, 사망자, 교통 장애를 최소화하기 위해 교통 사고를 신속하게 감지하고 응급 서비스에 신속하게 통보하는 데 중점을 두고 있습니다. 사고 감지 및 대응 분야는 스마트 모니터링, 통신 인프라, 자동 대응을 통합하여 도로의 안전성을 높이고, 사고 및 위험 상황에서의 대응 시간을 단축하는 방식으로 스마트 모니터링, 통신 인프라, 자동 대응을 통합하고 있습니다.

이 부문은 응급 서비스가 문서를 분석하고 조기 개입을 통해 위험을 줄일 수 있도록 함으로써 교통사고 사망자 수를 줄이는 것을 목표로 하고 있습니다. 교통사고 사망자 수를 줄임으로써 사고 감지 및 대응 부문은 사고로 인한 지연과 정체를 줄여 궁극적으로 전체 교통 효율을 향상시킬 수 있습니다. 또한, 이 분야는 비전 제로, 지능형 교통 시스템(ITS), 자율주행차 준비라는 목표에 크게 기여하며, 세계 교통안전 생태계에서 고성장 분야로 자리매김하고 있습니다.

북미는 현재 교통안전 시장에서 가장 큰 시장 점유율을 차지하고 있는데, 이는 디지털 기술의 보급, 스마트 인프라 기술, 대형 교통안전 벤더의 존재 등이 그 배경입니다. 북미 정부는 비전 제로, 미국 교통안전전략(NRSS), 캐나다 교통안전전략 2025 등 더 안전한 도로 이용자, 더 안전한 차량, 더 스마트한 인프라에 우선순위를 두는 다양한 프로그램을 도입하고 있습니다. 미국 교통부는 또한 AI 기반 단속 프로그램 시행, 자동 과속 단속 카메라 배치, 스마트 신호등 및 보행자 보호 장치 설치에 50억 달러를 투자하는 'Safe Streets and Roads for All(SS4A)' 프로그램을 통해 교통 안전 혁신을 장려하고 있습니다.

아시아태평양은 전 세계 교통안전 상황에서 가장 빠르게 성장하고 있는 지역으로 부상하고 있습니다. 도시화가 진행되면서 자동차 보유율이 상승하고 교통사고 사망을 억제하려는 정부의 의지가 높아졌기 때문입니다. 이에 따라 인도, 중국, 일본, 일본, 한국, 호주가 지능형 교통 시스템(ITS), 진화하는 스마트시티 프로그램, 교통 단속 기술에 대한 대규모 투자로 선두를 달리고 있습니다.

세계의 교통 안전 시장에 대해 조사했으며, 제공 제품별, 전개 모델별, 구현 유형별, 데이터 유형별, 용도별, 최종사용자별, 지역별 동향, 시장 진출기업 프로파일 등의 정보를 정리하여 전해드립니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 프리미엄 인사이트

제5장 시장 개요와 업계 동향

서론

시장 역학

2025년 미국 관세가 교통안전 시장에 미치는 영향

교통안전 솔루션 진화

공급망 분석

생성형 AI가 교통안전 시장에 미치는 영향

생태계 분석

투자 상황과 자금조달 시나리오

사례 연구 분석

기술 분석

관세 및 규제 상황

무역 분석

특허 분석

가격 분석

주요 컨퍼런스 및 이벤트(2025년-2026년)

Porter의 Five Forces 분석

구입자에게 영향을 미치는 동향과 혼란

주요 이해관계자와 구입 기준

기술 로드맵

파트너십과 에코시스템 전략

이해관계자에게 있어서의 전략적 필수사항

제6장 교통안전 시장(제공 제품별)

서론

솔루션

서비스

제7장 교통안전 시장(전개 모델별)

서론

고정 설비

이동식/트레일러 탑재형 시스템

휴대용/일시적인 솔루션

클라우드 기반 플랫폼

제8장 교통안전 시장(시행 유형별)

서론

자동

수동

하이브리드

제9장 교통안전 시장(데이터 유형별)

서론

비디오 및 영상

센서 데이터

통합 빅데이터

제10장 교통안전 시장(용도별)

서론

위반 관리

트래픽 최적화

사고 방지

긴급 대응

성장 촉진요인 행동 모니터링

공공인식/교육

보행자 및 VRU 보호

작업 구역 안전 관리

보험 리스크 평가

제11장 교통안전 시장(최종사용자별)

서론

정부 및 지방자치단체

고속도로 당국

법집행기관

민간 통행요금 징수 업자

스마트 시티 인테그레이터

건설회사

기타

제12장 교통안전 시장(지역별)

서론

북미

북미 : 교통안전 시장 성장 촉진요인

북미 : 거시경제 전망

미국

캐나다

유럽

유럽 : 교통안전 시장 성장 촉진요인

유럽 : 거시경제 전망

영국

독일

프랑스

이탈리아

스페인

기타

아시아태평양

아시아태평양 : 교통안전 시장 촉진 역

아시아태평양 : 거시경제 전망

중국

일본

인도

호주 및 뉴질랜드

ASEAN

한국

기타

중동 및 아프리카

중동 및 아프리카 : 교통안전 시장 성장 촉진요인

중동 및 아프리카 : 거시경제 전망

사우디아라비아

아랍에미리트(UAE)

남아프리카공화국

카타르

기타

라틴아메리카

라틴아메리카 : 교통안전 시장 성장 촉진요인

라틴아메리카 : 거시경제 전망

브라질

멕시코

아르헨티나

기타

제13장 경쟁 구도

개요

주요 시장 진출기업의 전략/강점, 2022년-2025년

매출 분석, 2020년-2024년

시장 점유율 분석, 2024년

제품 비교 분석

기업 평가와 재무 지표

기업 평가 매트릭스 : 주요 시장 진출기업, 2024년

기업 평가 매트릭스 : 스타트업/중소기업(하드웨어), 2024년

기업 평가 매트릭스 : 스타트업/중소기업(소프트웨어), 2024년

경쟁 시나리오와 동향

제14장 기업 개요

주요 시장 진출기업

JENOPTIK

KAPSCH TRAFFICCOM

SENSYS GATSO GROUP

VERRA MOBILITY

TELEDYNE FLIR

MOTOROLA SOLUTIONS

IDEMIA

SWARCO

VITRONIC

SIEMENS

CONDUENT

CUBIC CORPORATION

DAHUA TECHNOLOGY

LASER TECHNOLOGIES

기타 기업

TRAFFIC MANAGEMENT TECHNOLOGIES

TRIFOIL

KRIA

SYNTELL

TRUVELO

CLEARVIEW INTELLIGENCE

SIMICON

FRED ENGINEERING

KODIAK ROBOTICS

HUMANISING AUTONOMY

VEBITS AI

CONNECTED WISE LLC

SAFEROAD

LIVEROAD ANALYTICS

VIVACITY

NOTRAFFIC

VALERANN

ACUSENSUS

제15장 인접 시장과 관련 시장

제16장 부록

LSH

영문 목차

영문목차

The road safety market is expanding rapidly, with a projected market size rising from USD 6.69 billion in 2025 to USD 12.39 billion by 2030, at a CAGR of 13.1% during the forecast period. To reduce accident costs and to protect assets and comply with regulations, fleet operators are now focusing on road safety. This is resulting in the rapid adoption rates of technologies such as the monitoring of driver behavior, AI dashcams, telematics, and even fatigue detection solutions.

Scope of the Report

Years Considered for the Study

2020-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

USD (Million)

Segments

Offering, Deployment Model, Data Type, Enforcement Type, Application, End User, and Region

Regions covered

North America, Europe, Asia Pacific, Middle East & Africa, and Latin America

Along with access to advanced safety technologies, the commercial fleet now benefits from improved driver accountability, insurance discounts, and overall higher efficiency levels. Consequently, the demand for road safety solutions tailored to fleets is rising, driving growth and innovation across the road safety market.

Although road safety technologies have great potential for improvement, rising worries about the sensitivity of surveillance methods and risks related to data management pose significant restraints to market expansion. The widespread use of AI-powered cameras, automatic license plate recognition, and driver monitoring systems has led to increased examination of public surveillance and data privacy concerns.

"By end user, government & municipalities segment will likely hold the largest market share during the forecast period"

Government agencies and municipalities widely adopt road safety solutions. They play a major role in overseeing everything from awareness programs to managing and deploying comprehensive safety infrastructure and enforcement systems. They are crucial in the road safety market, acting as regulators and implementers of safety policies. By providing funding and developing programs, they can significantly influence public safety. Government agencies and municipalities are responsible for enforcing compliance with legislation and also allocating budgets for infrastructure improvements.

They manage traffic signals and signs on roadways, deploy cameras for red light and speed enforcement, combat violations using AI, and implement real-time traffic management systems. In November 2024, the city of Brampton in Canada worked with Jenoptik to deploy over 180 automated speed enforcement cameras to improve the compliance rate in school zones.

"By solution type, incident detection & response to account for the fastest growth rate during the forecast period"

The incident detection and response segment is a key part of the road safety market, focusing on quickly detecting traffic incidents and promptly notifying emergency services to minimize injuries, fatalities, and traffic disruptions. The incident detection and response segment integrates smart surveillance, communications infrastructure, and automated responses in a way that increases the safety of roadways and decreases response time in accidents or dangerous situations.

This segment aims to reduce road fatalities by enabling emergency services to analyze documentation and mitigate risks through early intervention. By decreasing road fatalities, the incident detection and response segment will also lessen delays and congestion caused by accidents, ultimately improving overall traffic efficiency. Additionally, this segment contributes significantly to the goals of Vision Zero, intelligent transport systems (ITS), and the readiness for autonomous vehicles, making it a high-growth area within the global road safety ecosystem.

"North America leads in market share while Asia Pacific emerges as the fastest-growing region in the road safety market"

North America currently holds the largest market share in the road safety market, driven by widespread digital adoption, smart infrastructure technologies, and the presence of major road safety vendors. North American governments are introducing various programs, such as Vision Zero, the U.S. National Roadway Safety Strategy (NRSS), and Canada's Road Safety Strategy 2025, that focus their priorities on safer road users, safer vehicles, and smarter infrastructure. The U.S. Department of Transportation is also encouraging innovation in road safety with its Safe Streets and Roads for All (SS4A) program, which is backed by USD 5 billion to implement AI-based enforcement programs, deploy automated speed cameras, and install smart traffic signals and pedestrian protections.

The Asia Pacific region is emerging as the fastest-growing region in the global road safety landscape, as it continues to urbanize, with increasing motorization rates and increased government desire to curb road traffic fatalities. In line with this, India, China, Japan, South Korea, and Australia are leading the way with their large investments into intelligent transportation systems (ITS), evolving smart city programs, and traffic enforcement technologies.

Breakdown of Primaries

In-depth interviews were conducted with Chief Executive Officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the road safety market.

By Company: Tier I - 34%, Tier II - 43%, and Tier III - 23%

By Designation: C-Level Executives - 50%, D-Level Executives -30%, and others - 20%

By Region: North America - 30%, Europe - 30%, Asia Pacific - 25%, Middle East & Africa - 10%, and Latin America - 5%

The report profiles key players in the road safety market, including JENOPTIK (Germany), Kapsch TrafficCom (Austria), Sensys Gatso Group (Sweden), IDEMIA (France), Teledyne FLIR (US), Motorola Solutions (US), Verra Mobility (US), SWARCO (Austria), Siemens (Germany), Cubic Corporation (US), Conduent (US), VITRONIC (Germany), Dahua Technology (China), Laser Technology (US), Traffic Management Technology (South Africa), Truvelo (UK), Kria (Italy), Syntell (South Africa), Clearview Intelligence (UK), Simicon (Russia), FRED Engineering (Italy), Kodiak Robotics (US), Humanising Autonomy (UK), Vebit AI (US), Connected Wise LLC (US), Saferoad (Germany), LiveRoad Analytics (US), Acusensus (Australia), Valerann (UK), NoTraffic (Israel), and Vivacity (UK).

Research Coverage

This research report categorizes the road safety market based on offering [solution (type {enforcement solution, incident detection and response, ALPR/ANPR, traffic monitoring & control, pedestrian safety}, and component {hardware and software}) and services], deployment model (fixed installation, mobile/trailer-mounted systems, portable/temporary solutions, and cloud-based platforms), data type (video & image, sensor data and integrated big data), enforcement type (automated, manual, or hybrid), application (violation management, traffic optimization, accident prevention, emergency response, and public awareness & training, pedestrian & VRU protection, work zone safety management, insurance risk assessment), end user (government & municipalities, highway authorities, law enforcement agencies, private toll operators, smart city integrators, construction companies, others {fleet operators and insurance providers}) and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the road safety market. A detailed analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, and mergers and acquisitions; and recent developments associated with the road safety market. Competitive analysis of upcoming startups in the road safety market ecosystem was also covered in this report.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall road safety market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to improve their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (commercial fleets push for safety-driven operational efficiency, Enforcement to improve compliance with governments, the adoption of digitalization and technologies in the road safety market, government initiatives for enhancing road safety, urban surge fuels smart road safety revolution amid rising traffic risks), restraints (Lack of standardized and uniform technologies, data privacy and surveillance concerns hinder adoption of road safety technologies), opportunities (improved intelligent transportation systems for road safety, integration of AI and predictive analytics in traffic management systems, growth evolving 5G technology and transformation of road safety systems), and challenges (Digital reluctance and fragmentation in legacy fleet segments, infrastructure gaps and budget constraints limit road safety technology deployment)

Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the road safety market

Market Development: Comprehensive information about lucrative markets - the report analyses the road safety market across varied regions

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the road safety market

Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like JENOPTIK (Germany), Kapsch TrafficCom (Austria), Sensys Gatso Group (Sweden), IDEMIA (France), Teledyne FLIR (US), Motorola Solutions (US), Verra Mobility (US), SWARCO (Austria), Siemens (Germany), Cubic Corporation (US), Conduent (US), VITRONIC (Germany), Dahua Technology (China), Laser Technology (US), Traffic Management Technology (South Africa), Truvelo (UK), Kria (Italy), Syntell (South Africa), Clearview Intelligence (UK), Simicon (Russia), FRED Engineering (Italy), Kodiak Robotics (US), Humanising Autonomy (UK), Vebit AI (US), Connected Wise LLC (US), Saferoad (Germany), LiveRoad Analytics (US), Acusensus (Australia), Valerann (UK), NoTraffic (Israel), and Vivacity (UK)

The report also helps stakeholders understand the pulse of the road safety market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION AND SCOPE

1.2.1 INCLUSIONS AND EXCLUSIONS

1.3 MARKET SCOPE

1.3.1 MARKET SEGMENTATION

1.3.2 YEARS CONSIDERED

1.4 CURRENCY CONSIDERED

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.2 PRIMARY DATA

2.1.2.1 List of primary participants

2.1.2.2 Breakdown of primaries

2.1.2.3 Key industry insights

2.2 MARKET BREAKUP AND DATA TRIANGULATION

2.3 MARKET SIZE ESTIMATION

2.3.1 TOP-DOWN APPROACH

2.3.2 BOTTOM-UP APPROACH

2.4 MARKET FORECAST

2.5 RESEARCH ASSUMPTIONS

2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES IN ROAD SAFETY MARKET

4.2 ROAD SAFETY MARKET: TOP THREE APPLICATIONS

4.3 NORTH AMERICA: ROAD SAFETY MARKET, BY DATA TYPE AND ENFORCEMENT TYPE

5.7.1.2 ALPR/ANPR (automatic number plate recognition)

5.7.1.3 Incident detection & response

5.7.1.4 Traffic monitoring & control

5.7.1.5 Pedestrian safety solutions

5.8 INVESTMENT LANDSCAPE AND FUNDING SCENARIO

5.9 CASE STUDY ANALYSIS

5.9.1 USE CASE 1: SIEMENS HELPED YUNEX TRAFFIC WITH ADAPTIVE TRAFFIC CONTROL AND MANAGEMENT, HIGHWAY, AND TUNNEL AUTOMATION AS WELL AS SMART SOLUTIONS FOR V2X AND ROAD USER CHARGING (TOLLING)

5.9.2 USE CASE 2: MOTOROLA SOLUTIONS HELPED VICTORIA POLICE WITH NUMBER PLATE RECOGNITION WITH ANPR TECHNOLOGY

5.9.3 USE CASE 3: CONDUENT AND HAYDEN AI ANNOUNCED TECHNOLOGY PARTNERSHIP TO IMPROVE BUS LANE PERFORMANCE AND TRAFFIC SAFETY

5.9.4 USE CASE 4: SWARCO ROAD MARKING SYSTEMS AND ISAC GMBH MEASURED DETECTABILITY OF ROAD MARKINGS

5.9.5 CASE STUDY 6: DATA COLLECTION LIMITED ENHANCED ROAD INFRASTRUCTURE MANAGEMENT WITH TELEDYNE FLIR IMAGING SOLUTIONS

5.10 TECHNOLOGY ANALYSIS

5.10.1 KEY TECHNOLOGIES

5.10.1.1 Artificial intelligence (AI)

5.10.1.2 Internet of things (IoT)

5.10.1.3 Geographic information systems (GIS)

5.10.1.4 Automatic number plate recognition (ANPR)

5.10.1.5 Vehicle-to-infrastructure (V2I) and vehicle-to-everything (V2X)

5.10.2 COMPLEMENTARY TECHNOLOGIES

5.10.2.1 Big data and analytics

5.10.2.2 Edge computing

5.10.2.3 5G

5.10.3 ADJACENT TECHNOLOGIES

5.10.3.1 Advanced traffic management systems (ATMS)

5.10.3.2 Smart city solutions

5.10.3.3 Blockchain

5.11 TARIFF AND REGULATORY LANDSCAPE

5.11.1 TARIFF RELATED TO ROAD SAFETY SOLUTIONS

5.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.11.3 KEY REGULATIONS

5.11.3.1 North America

5.11.3.2 Europe

5.11.3.3 Asia Pacific

5.11.3.4 Middle East & Africa

5.11.3.5 Latin America

5.12 TRADE ANALYSIS

5.12.1 EXPORT SCENARIO OF ELECTRICAL SIGNALING AND TRAFFIC CONTROL EQUIPMENT (HS CODE 853080)

5.12.2 IMPORT SCENARIO OF ELECTRICAL SIGNALING AND TRAFFIC CONTROL EQUIPMENT (HS CODE 853080)

5.13 PATENT ANALYSIS

5.13.1 METHODOLOGY

5.13.2 PATENTS FILED, BY DOCUMENT TYPE

5.13.3 INNOVATION AND PATENT APPLICATIONS

5.14 PRICING ANALYSIS

5.14.1 AVERAGE SELLING PRICE OF OFFERING, BY KEY PLAYER, 2025

5.14.2 INDICATIVE PRICING, BY APPLICATION, 2025

5.15 KEY CONFERENCES AND EVENTS (2025-2026)

5.16 PORTER'S FIVE FORCES ANALYSIS

5.16.1 THREAT OF NEW ENTRANTS

5.16.2 THREAT OF SUBSTITUTES

5.16.3 BARGAINING POWER OF BUYERS

5.16.4 BARGAINING POWER OF SUPPLIERS

5.16.5 INTENSITY OF COMPETITIVE RIVALRY

5.17 TRENDS AND DISRUPTIONS IMPACTING BUYERS

5.18 KEY STAKEHOLDERS AND BUYING CRITERIA

5.18.1 KEY STAKEHOLDERS IN BUYING PROCESS

5.18.2 BUYING CRITERIA

5.19 TECHNOLOGY ROADMAP

5.19.1 ROAD SAFETY TECHNOLOGY ROADMAP TILL 2030

5.19.1.1 Short-term roadmap (2024-2026)

5.19.1.2 Mid-term roadmap (2026-2028)

5.19.1.3 Long-term roadmap (2028-2030)

5.20 PARTNERSHIP & ECOSYSTEM STRATEGIES

5.20.1 PARTNERSHIP & ECOSYSTEM STRATEGIES

5.21 STRATEGIC IMPERATIVES FOR STAKEHOLDERS

5.21.1 STRATEGIC IMPERATIVES FOR STAKEHOLDERS

6 ROAD SAFETY MARKET, BY OFFERING

6.1 INTRODUCTION

6.1.1 OFFERING: ROAD SAFETY MARKET DRIVERS

6.2 SOLUTION

6.2.1 ENABLING SAFER ROADS THROUGH END-TO-END INTELLIGENT TRAFFIC ENFORCEMENT AND MANAGEMENT SOLUTIONS

6.2.2 SOLUTION TYPE

6.2.2.1 Enforcement solutions

6.2.2.1.1 Red light enforcement

6.2.2.1.2 Speed enforcement systems

6.2.2.1.3 Seat belt & mobile phone enforcement

6.2.2.1.4 DUI enforcement

6.2.2.1.5 Temporary speed enforcement

6.2.2.2 ALPR/ANPR

6.2.2.2.1 Fixed ALPR systems

6.2.2.2.2 Mobile ALPR systems

6.2.2.2.3 Portable ALPR

6.2.2.2.4 ALPR analytics

6.2.2.3 Incident detection and response

6.2.2.3.1 Violation detection

6.2.2.3.2 Accident detection

6.2.2.3.3 Emergency vehicle preemption and notification

6.2.2.3.4 Congestion/Queue detection

6.2.2.3.5 Driver behavior monitoring systems

6.2.2.4 Traffic monitoring & control

6.2.2.4.1 Smart traffic signals

6.2.2.4.2 Variable message signs

6.2.2.4.3 Road weather information systems (RWIS)

6.2.2.4.4 Dynamic lane management

6.2.2.5 Pedestrian safety

6.2.2.5.1 Smart crosswalks

6.2.2.5.2 VRU detection

6.2.2.5.3 Pedestrian alert system

6.2.3 COMPONENT

6.2.3.1 Hardware

6.2.3.1.1 Cameras

6.2.3.1.2 Sensors

6.2.3.1.3 Smart signs & signals

6.2.3.1.4 Roadside units (RSUS)

6.2.3.1.5 Other hardware

6.2.3.2 Software

6.2.3.2.1 Violation detection engines

6.2.3.2.2 AI/ML analytics platform

6.2.3.2.3 LPR/OCR recognition software

6.2.3.2.4 Command & simulation tools

6.2.3.2.5 Other software

6.3 SERVICES

6.3.1 OFFER PROFESSIONAL AND MANAGED SERVICES FOR INSTALLATION, COMMISSIONING, CALIBRATION, AND FUNCTIONAL TESTING OF CRITICAL ROAD SAFETY EQUIPMENT

8.2.1 DEPLOYING INTELLIGENT TECHNOLOGY-DRIVEN SYSTEMS TO ENABLE CONTINUOUS, UNBIASED, AND FULLY AUTOMATED ENFORCEMENT OF TRAFFIC VIOLATIONS ACROSS DIVERSE ENVIRONMENTS

8.3 MANUAL ENFORCEMENT

8.3.1 CONDUCTING FIELD-LEVEL ENFORCEMENT OPERATIONS THROUGH HUMAN INTERVENTION TO ENSURE REGULATORY COMPLIANCE AND ADDRESS SITUATIONAL ROAD SAFETY CHALLENGES

8.4 HYBRID ENFORCEMENT

8.4.1 ENSURE RELIABLE, FLEXIBLE, AND REAL-TIME AI DELIVERY WITH ADVANCED MODEL DEPLOYMENT AND SERVING FUNCTIONALITIES

9 ROAD SAFETY MARKET, BY DATA TYPE

9.1 INTRODUCTION

9.1.1 DATA TYPE: ROAD SAFETY MARKET DRIVERS

9.2 VIDEO & IMAGE

9.2.1 HARNESSING REAL-TIME AND HIGH-RESOLUTION VISUAL EVIDENCE THROUGH AI-ENABLED CAMERA NETWORKS TO AUTOMATE VIOLATION DETECTION AND ENHANCE INCIDENT TRACEABILITY IN TRAFFIC ECOSYSTEMS

9.3 SENSOR DATA

9.3.1 CONDUCTING DEPLOYING HIGH-PRECISION ROADWAY AND ROADSIDE SENSORS TO CAPTURE REAL-TIME VEHICLE AND TRAFFIC BEHAVIOR DATA FOR CONTINUOUS, NON-VISUAL MONITORING

9.4 INTEGRATED BIG DATA

9.4.1 AGGREGATING CROSS-DOMAIN AND MULTI-SOURCE DATASETS INTO SCALABLE PLATFORMS TO ENABLE PREDICTIVE ROAD SAFETY INTELLIGENCE, OPTIMIZE ENFORCEMENT STRATEGIES

10 ROAD SAFETY MARKET, BY APPLICATION

10.1 INTRODUCTION

10.1.1 APPLICATION: ROAD SAFETY MARKET DRIVERS

10.2 VIOLATION MANAGEMENT

10.2.1 IMPLEMENTING INTELLIGENT ROAD SAFETY SOLUTIONS TO AUTOMATE VIOLATION DETECTION AND STREAMLINE CITATION PROCESSING FOR SAFER ROAD NETWORKS

10.3 TRAFFIC OPTIMIZATION

10.3.1 USING DATA-DRIVEN CONTROL STRATEGIES AND REAL-TIME OPTIMIZATION TECHNOLOGIES WILL REDUCE CONGESTION AND ENHANCE MOBILITY ACROSS URBAN ROAD NETWORKS

10.4 ACCIDENT PREVENTION

10.4.1 DEPLOYING PREDICTIVE ANALYTICS AND ENVIRONMENTAL SENSING TECHNOLOGIES TO IDENTIFY RISK ZONES AND IMPLEMENT PROACTIVE MEASURES

10.5 EMERGENCY RESPONSE

10.5.1 ENABLING ACCELERATED INCIDENT DETECTION AND REAL-TIME COORDINATION OF EMERGENCY SERVICES TO REDUCE RESPONSE TIME

10.6 DRIVER BEHAVIOR MONITORING

10.6.1 LEVERAGING IN-VEHICLE ANALYTICS AND SENSOR FUSION TO TRACK AND CORRECT UNSAFE DRIVING BEHAVIORS FOR LONG-TERM BEHAVIORAL CHANGE AND CRASH REDUCTION

10.7 PUBLIC AWARENESS/TRAINING

10.7.1 PROMOTING ROAD SAFETY CULTURE THROUGH IMMERSIVE AWARENESS PROGRAMS AND STRUCTURED TRAINING

10.8 PEDESTRIAN & VRU PROTECTION

10.8.1 INTEGRATING SMART INFRASTRUCTURE AND DETECTION SYSTEMS TO SAFEGUARD PEDESTRIANS AND VULNERABLE ROAD USERS THROUGH REAL-TIME ALERTS

10.9 WORK ZONE SAFETY MANAGEMENT

10.9.1 ENHANCING SAFETY IN ACTIVE WORK ZONES BY DEPLOYING CONNECTED ENFORCEMENT SYSTEMS AND DYNAMIC WARNINGS TO PREVENT COLLISIONS AND PROTECT ROAD CREWS

10.10 INSURANCE RISK ASSESSMENT

10.10.1 UTILIZING BEHAVIORAL ANALYTICS AND TELEMATICS TO ACCURATELY ASSESS DRIVER RISK PROFILES AND INFORM DYNAMIC, USAGE-BASED INSURANCE AND SAFETY STRATEGIES

11 ROAD SAFETY MARKET, BY END USER

11.1 INTRODUCTION

11.1.1 END USER: ROAD SAFETY MARKET DRIVERS

11.2 GOVERNMENT & MUNICIPALITIES

11.2.1 GOVERNMENTS AND MUNICIPALITIES LEAD ROAD SAFETY EFFORTS THROUGH FUNDING, REGULATION, AND SMART CITY INITIATIVES

11.3 HIGHWAY AUTHORITIES

11.3.1 HIGHWAY AUTHORITIES ADOPT SMART INFRASTRUCTURE TO ENSURE SAFETY ON HIGH-SPEED ROAD NETWORKS

11.4 LAW ENFORCEMENT AGENCIES

11.4.1 LAW ENFORCEMENT AGENCIES EMBRACE SURVEILLANCE AND ANALYTICS TO MONITOR AND CONTROL TRAFFIC VIOLATIONS

11.5 PRIVATE TOLL OPERATORS

11.5.1 TOLL OPERATORS INVEST IN INTELLIGENT SYSTEMS TO ENSURE SAFE, EFFICIENT, AND COMPLIANT ROAD USAGE

11.6 SMART CITY INTEGRATORS

11.6.1 SMART CITY INTEGRATORS EMBED ROAD SAFETY WITHIN BROADER URBAN DIGITAL INFRASTRUCTURE

11.7 CONSTRUCTION COMPANIES

11.7.1 CONSTRUCTION FIRMS IMPLEMENT SAFETY PROTOCOLS AND TECHNOLOGIES ACROSS ROAD DEVELOPMENT PHASES

11.8 OTHER END USERS

12 ROAD SAFETY MARKET, BY REGION

12.1 INTRODUCTION

12.2 NORTH AMERICA

12.2.1 NORTH AMERICA: ROAD SAFETY MARKET DRIVERS

12.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

12.2.3 US

12.2.3.1 Institutionalized cross-sector data integration and predictive enforcement to scale vision zero across diverse urban and rural mobility ecosystems

12.2.4 CANADA

12.2.4.1 Align safety modernization with climate goals through municipal co-funding, open data mandates, and community-based AI enforcement

12.3 EUROPE

12.3.1 EUROPE: ROAD SAFETY MARKET DRIVERS

12.3.2 EUROPE: MACROECONOMIC OUTLOOK

12.3.3 UK

12.3.3.1 UK's nationwide deployment of AI-powered speed enforcement, smart crossings, and connected mobility zones to drive toward zero fatalities

12.3.4 GERMANY

12.3.4.1 Germany scaling road safety through V2X integration, dynamic lane controls, and urban zero-vision zones