Metal Forming Equipment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1913279

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 237 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

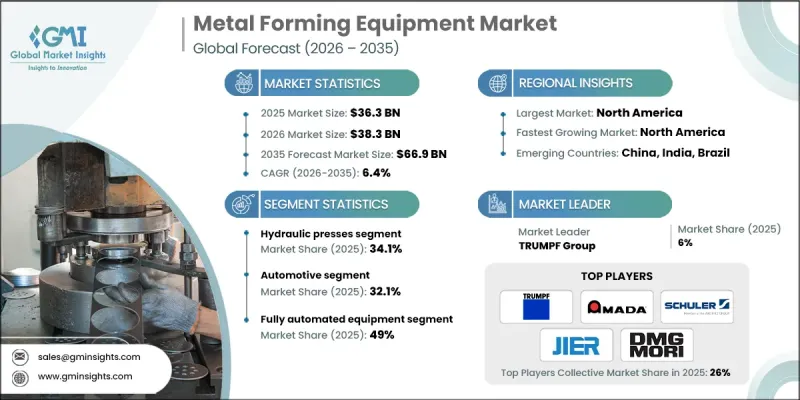

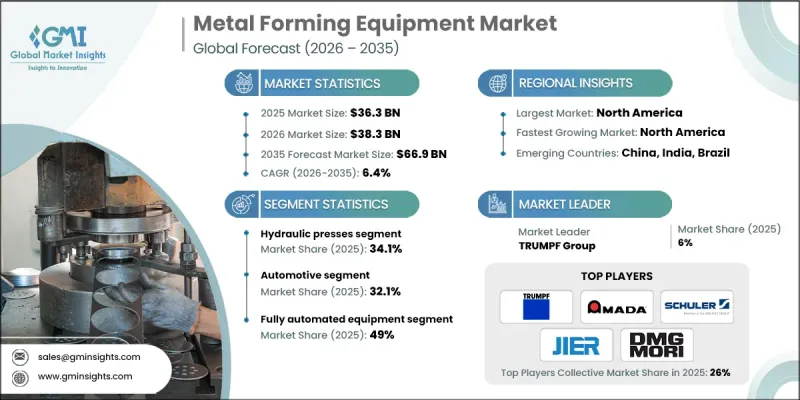

세계 금속 성형 장비 시장은 2025년 363억 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 6.4%로 성장하여 669억 달러에 이를 것으로 예측됩니다.

제조업체가 첨단 디지털 제조 기술과 차세대 장비 아키텍처를 채택함에 따라 업계는 구조적 변화를 겪고 있습니다. 스마트 제조 프레임워크에서는 정밀도, 일관성, 가동 신뢰성 향상을 위해 센서 기반 모니터링, 실시간 데이터 처리, 예지보전의 통합이 점차 진행되고 있습니다. 디지털화된 생산 환경에서는 성형 파라미터의 엄격한 제어가 가능해져 에너지 효율과 출력 품질의 향상을 도모할 수 있습니다. 또한 기존의 대체품에 비해 뛰어난 모션 제어와 저에너지 소비를 실현하는 서보 전동 프레스 시스템의 보급이 진행되고 주요 기술적 전환도 진행 중입니다. 산업이 경량 재료와 복잡한 형상을 우선시함에 따라 수요 패턴은 더욱 진화하여 성형 방법과 공구 설계의 혁신을 추진하고 있습니다. 운송 장비 및 항공우주 제조 분야에서 전기화의 추세는 높은 정밀도와 재현성을 갖춘 성형 솔루션에 대한 요구를 강화하고 있습니다. 이러한 요인들이 결합되어 설비 투자 전략이 재구성되고 장비 공급업체는 보다 스마트하고 유연하며 자동화 지원 플랫폼을 제공하도록 요구되고 있습니다. 시장은 장기적인 산업 현대화 이니셔티브와 세계 생산 기지의 고성능 제조 설비에 대한 지속적인 수요의 혜택을 누리고 있습니다.

시장 범위

시작 연도

2025년

예측 연도

2026-2035년

시작 금액

363억 달러

예측 금액

669억 달러

CAGR

6.4%

자동차 부문은 2035년까지 연평균 복합 성장률(CAGR) 7.3%로 성장하여 설비 혁신의 주요 추진력으로서의 지위를 강화합니다. 전동화 이동성 플랫폼으로의 전환은 경량의 고강도 재료를 다루면서 정확성과 구조적 무결성을 유지할 수 있는 첨단 성형 시스템에 대한 수요를 증가시키고 있습니다.

2025년 현재 완전 자동화 금속 성형 장비 부문은 49%의 점유율을 차지했습니다. 인건비 상승, 노동력 부족, 연속 생산에 대한 수요가 증가함에 따라 제조업체는 로봇 공학, 지능형 제어 및 최소한의 인위적 개입을 통합한 자동화 기술 도입을 촉진하고 있습니다.

미국 금속 성형 장비 시장은 82.1%의 점유율을 차지했고, 115억 달러의 매출과 7%의 연평균 복합 성장률(CAGR)을 달성했습니다. 강력한 연방 투자 프로그램과 산업 현대화 이니셔티브는 여러 분야에서 정밀 성형 부품 수요를 이끌고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 현황

수익률

단계별 부가가치

밸류체인에 영향을 주는 요인

업계에 미치는 영향요인

성장 촉진요인

전기자동차(EV)의 대두와 경량화

Industry 4.0과 자동화의 통합

세계적인 인프라 개발과 산업화

업계의 잠재적 위험 및 과제

고액의 자본 투자와 장기적인 투자 회수 기간

숙련 노동자 및 기술자의 부족

기회

신흥 경제국의 미개척 시장

물리적 및 디지털 영역의 융합(STEAM)

친환경 제조 및 에너지 효율 장비

공급망 리쇼어링 및 니어쇼어링

성장 가능성 분석

장래 시장 동향

기술과 혁신 동향

현재의 기술 동향

신흥기술

가격 동향

지역별

유형별

규제 상황

규격 및 컴플라이언스 요건

지역별 규제 프레임워크

인증기준

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

확대 계획

제5장 시장 추정 및 예측 : 유형별, 2022-2035

유압 프레스

기계식 프레스

압연기

기타

제6장 시장 추정 및 예측 : 용도별, 2022-2035

자동차

항공우주 및 방위

건설

전자기기

기타

제7장 시장 추정 및 예측 : 자동화 레벨별, 2022-2035

완전 자동화 설비

반자동화 설비

제8장 시장추정 및 예측 : 유통채널별, 2022-2035

온라인

오프라인

제9장 시장추정 및 예측 : 지역별, 2022-2035

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

TRUMPF Group

Amada Co., Ltd.

Schuler AG

JIER Machine-Tool Group

DMG Mori

AIDA Engineering

Komatsu Ltd.

Fagor Arrasate

Haas Automation

BYSTRONIC

Mitsubishi HI Machine Tool

Cincinnati Incorporated

LVD Group

MAG IAS

Bliss-Bret Industries

WardJet

Prima Industrie

Salvagnini

Ermaksan

Hyundai Rotem

SHW

영문 목차

영문목차

The Global Metal Forming Equipment Market was valued at USD 36.3 billion in 2025 and is estimated to grow at a CAGR of 6.4% to reach USD 66.9 billion by 2035.

The industry undergoes a structural transformation as manufacturers adopt advanced digital manufacturing practices and next-generation equipment architectures. Smart manufacturing frameworks increasingly integrate sensor-based monitoring, real-time data processing, and predictive maintenance to enhance precision, consistency, and operational reliability. Digitalized production environments allow tighter control over forming parameters while improving energy efficiency and output quality. A major technological transition also takes shape as servo-electric press systems gain wider acceptance due to their superior motion control and reduced energy consumption when compared to legacy alternatives. Demand patterns further evolve as industries prioritize lightweight materials and complex geometries, driving innovation in forming methods and tooling design. Electrification trends across transportation and aerospace manufacturing intensify requirements for highly accurate and repeatable forming solutions. These converging factors reshape capital investment strategies and push equipment suppliers to deliver smarter, more flexible, and automation-ready platforms. The market benefits from long-term industrial modernization initiatives and sustained demand for high-performance manufacturing equipment across global production hubs.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$36.3 Billion

Forecast Value

$66.9 Billion

CAGR

6.4%

The automotive segment will grow at a CAGR of 7.3% through 2035, reinforcing its position as the primary catalyst for equipment innovation. The shift toward electrified mobility platforms increases demand for advanced forming systems capable of handling lightweight and high-strength materials while maintaining precision and structural integrity.

The fully automated metal forming equipment segment accounted for 49% share in 2025. Rising labor costs, workforce shortages, and demand for continuous production encourage manufacturers to deploy automation technologies that integrate robotics, intelligent controls, and minimal human intervention.

U.S. Metal Forming Equipment Market held 82.1% share, generating USD 11.5 billion and achieving a CAGR of 7%. Strong federal investment programs and industrial modernization initiatives drive demand for precision-formed components across multiple sectors.

Key companies operating in the Global Metal Forming Equipment Market include Schuler AG, TRUMPF Group, Amada Co., Ltd., DMG Mori, BYSTRONIC, Komatsu Ltd., Haas Automation, AIDA Engineering, Fagor Arrasate, JIER Machine-Tool Group, Mitsubishi HI Machine Tool, LVD Group, Cincinnati Incorporated, Salvagnini, MAG IAS, Ermaksan, Prima Industrie, WardJet, Bliss-Bret Industries, and Hyundai Rotem. Companies strengthen their position through continuous investment in automation, digital integration, and energy-efficient equipment design. Many manufacturers focus on developing modular systems that offer flexibility across multiple applications while reducing downtime. Strategic partnerships with end users support the co-development of customized solutions aligned with evolving production needs. Expanding service capabilities, including remote monitoring and lifecycle support, improves customer retention and operational reliability.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Age group

2.2.4 Distribution channel

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rise of Electric Vehicles (EVs) & Lightweighting

3.2.1.2 Integration of Industry 4.0 & Automation

3.2.1.3 Global Infrastructure Development & Industrialization

3.2.2 Industry pitfalls & challenges

3.2.2.1 High Capital Investment and Long ROI

3.2.2.2 Shortage of Skilled Labor and Technicians

3.2.3 Opportunities

3.2.3.1 Untapped Markets in Emerging Economies

3.2.3.2 Convergence of Physical and Digital Play (STEAM)

3.2.3.3 Green Manufacturing & Energy-Efficient Equipment

3.2.3.4 Reshoring and Near-shoring of Supply Chains

3.3 Growth potential analysis

3.4 Future market trends

3.5 Technology and innovation landscape

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.6 Price trends

3.6.1 By region

3.6.2 By type

3.7 Regulatory landscape

3.7.1 Standards and compliance requirements

3.7.2 Regional regulatory frameworks

3.7.3 Certification standards

3.8 Porter's analysis

3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East and Africa

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2022 - 2035 (USD Billion) (Thousand Units)

5.1 Key trends

5.2 Hydraulic Presses

5.3 Mechanical Presses

5.4 Rolling Machines

5.5 Others

Chapter 6 Market Estimates and Forecast, By Application, 2022 - 2035 (USD Billion) (Thousand Units)

6.1 Key trends

6.2 Automotive

6.3 Aerospace & Defense

6.4 Construction

6.5 Electronics

6.6 Others

Chapter 7 Market Estimates and Forecast, By Automation level, 2022 - 2035 (USD Billion) (Thousand Units)

7.1 Key trends

7.2 Fully Automated Equipment

7.3 Semi Automated Equipment

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2022 - 2035 (USD Billion) (Thousand Units)

8.1 Key trends

8.2 Online

8.3 Offline

Chapter 9 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Billion) (Thousand Units)