Groundwater Management Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035

상품코드:1892715

리서치사:Global Market Insights Inc.

발행일:2025년 12월

페이지 정보:영문 150 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

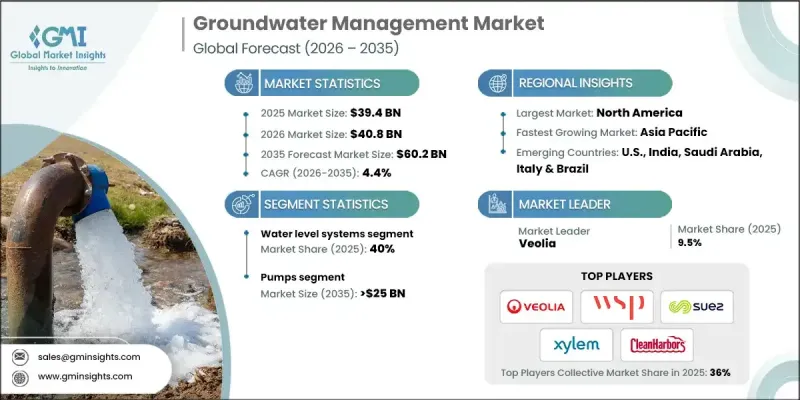

세계의 지하수 관리 시장은 2025년에 394억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.4%로 성장하여 602억 달러에 이를 것으로 예측됩니다.

시장 성장은 모듈화 및 단순화된 설계의 지속적인 혁신과 고도의 자동화 기술의 결합에 의해 촉진되고 있습니다. 스마트 센서와 원격 측정 시스템을 도입하여 운영자는 지하수위, 수질, 함양률을 실시간으로 모니터링 할 수 있습니다. 예측 분석은 과잉 채취와 오염을 방지할 수 있는 실행 가능한 인사이트를 제공하며, 이는 지하수 관리 솔루션에 대한 수요를 촉진하고 있습니다. 지하수 관리는 지하수 자원의 지속 가능한 이용과 보호를 보장하기 위해 고안된 전문 기술과 시스템을 포함합니다. 그 기능에는 대수층 수위 모니터링, 취수량 조절, 오염 방지 및 함양 과정 지원 등이 포함됩니다. 이 분야는 기본적인 취수를 넘어 자원 효율성 최적화, 오염 위험 관리, 지속가능성 목표를 지원하는 전략적 역할로 진화하고 있습니다. 재충전 전략과 처리수 재사용을 통합하여 운영 효율성과 비용 효율성을 더욱 향상시킬 수 있습니다.

시장 범위

개시 연도

2025년

예측 연도

2026-2035년

개시 연도 시장 규모

394억 달러

예측 금액

602억 달러

CAGR

4.4%

수위 시스템 부문은 2025년 40%의 점유율을 차지했습니다. 강화된 규제 요건과 지속 가능한 물 사용에 대한 강조는 첨단 수위 모니터링 시스템의 도입을 촉진하고 있습니다. 휴대성, 비용 효율성, 설치 용이성을 갖춘 센서에 대한 수요 증가가 보급을 촉진하고 있으며, 특히 지방에서 두드러지게 나타나고 있습니다. 이 장비들은 현재 pH, 탁도, 용존산소, 오염물질의 정확한 측정을 제공하여 엄격한 수질 기준을 준수할 수 있도록 보장합니다.

펌프 부문은 2025년 45%의 점유율을 차지할 것으로 예상되며, 2035년까지 250억 달러 규모로 성장할 것으로 전망됩니다. 가변 속도 구동 장치(VFD)와 자동 유량 조절 기능의 통합으로 펌프 효율을 향상시키고 낭비를 줄입니다. 탄소 감축 이니셔티브에 따라 태양광 발전 및 하이브리드 펌프 시스템에 대한 수요가 증가하고 있습니다. 각 제조업체들은 다양한 수문지질 조건에서 신뢰성을 확보하기 위해 모듈식 설계와 내식성 소재에 집중하고 있습니다.

북미 지하수 관리 시장은 2035년까지 180억 달러 규모에 달할 것으로 예측됩니다. 지자체와 산업체들은 엄격한 환경 규제에 대응하기 위해 첨단 센서와 자동 펌프 시스템 도입을 확대하고 있습니다. 공공 기관과 민간 기업의 강력한 협력, 그리고 지속적인 인프라 투자가 결합되어 시장 성장을 가속화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

원재료 가용성과 조달 분석

제조능력 평가

공급망 회복력과 리스크 요인

유통 네트워크 분석

규제 상황

업계에 대한 영향요인

성장 촉진요인

업계의 잠재적 리스크&과제

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

지하수 관리 비용 구조 분석

새로운 기회와 동향

디지털화와 IoT 통합

투자 분석과 전망

제4장 경쟁 구도

서론

기업의 시장 점유율 분석 : 지역별

북미

유럽

아시아태평양

중동 및 아프리카

라틴아메리카

전략적 대시보드

전략적 이니셔티브

주요 제휴 및 협력 관계

주요 M&A 활동

제품 혁신과 신제품 발매

시장 확대 전략

경쟁 벤치마킹

혁신과 지속가능성 상황

제5장 시장 규모와 예측 : 감시별, 2022-2035

주요 동향

수질 센서

수위 시스템

IoT 로거

지형공간 분석

제6장 시장 규모와 예측 : 추출 방법별, 2022-2035

주요 동향

펌프

시추공 시추

케이싱 및 스크린

통합 침투 시스템

제7장 시장 규모와 예측 : 함양 방법별, 2022-2035

주요 동향

인공 충진구조물

MAR 시스템

충진 우물

우수 침투

제8장 시장 규모와 예측 : 처리 방법별, 2022-2035

주요 동향

여과 시스템

펌프 및 트리트

탈염처리 및 화학 처리

생물학적/현장 처리

제9장 시장 규모와 예측 : 최종 용도별, 2022-2035

주요 동향

농업 분야

자치체

산업

제10장 시장 규모와 예측 : 지역별, 2022-2035

주요 동향

북미

미국

캐나다

유럽

독일

프랑스

영국

이탈리아

스페인

아시아태평양

중국

일본

인도네시아

인도

호주

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

이란

남아프리카공화국

이집트

라틴아메리카

브라질

아르헨티나

칠레

제11장 기업 개요

Arcadis

Black &Veatch

Clean Harbors Environmental Services

DMT Group

Envirogen Technologies

GEI Consultants

Grundfos

HEPACO

HPC AG

iFLUX

INDUS Environmental Services

Koop Wasserbau

Minetek

Remedial Construction Services

Sensoil Innovations

Stantec

SUEZ

Sweco AB

Tetra Tech

The Groundwater Company

Veolia

WJ Group

WSP Global

Xylem Water Solutions

LSH

영문 목차

영문목차

The Global Groundwater Management Market was valued at USD 39.4 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 60.2 billion by 2035.

Market growth is driven by continuous innovations in modular and simplified designs combined with advanced automation technologies. The deployment of smart sensors and telemetry systems allows operators to monitor groundwater levels, water quality, and recharge rates in real time. Predictive analytics provide actionable insights to prevent over-extraction and contamination, which fuels demand for groundwater management solutions. Groundwater management encompasses specialized techniques and systems designed to ensure sustainable utilization and protection of subsurface water resources. Its functions include monitoring aquifer levels, regulating extraction rates, preventing contamination, and supporting recharge processes. The sector has evolved beyond basic water extraction to a strategic role in optimizing resource efficiency, controlling contamination risks, and supporting sustainability goals. Incorporating recharge strategies and treated water reuse further enhances operational efficiency and cost-effectiveness.

Market Scope

Start Year

2025

Forecast Year

2026-2035

Start Value

$39.4 Billion

Forecast Value

$60.2 Billion

CAGR

4.4%

The water level systems segment held a 40% share in 2025. Increasing regulatory mandates and emphasis on sustainable water use are driving the adoption of advanced water level monitoring systems. Rising demand for portable, cost-effective, and easy-to-install sensors is boosting penetration, particularly in rural areas. These devices now provide accurate measurements of pH, turbidity, dissolved oxygen, and contaminants, ensuring compliance with strict water quality standards.

The pumps segment held a 45% share in 2025 and is expected to grow to USD 25 billion by 2035. The integration of variable frequency drives and automated flow regulation improves pumping efficiency and reduces wastage. Demand is rising for solar and hybrid pump systems that align with carbon reduction initiatives. Manufacturers are focusing on modular designs and corrosion-resistant materials to ensure reliability across diverse hydrogeological conditions.

North America Groundwater Management Market will reach USD 18 billion by 2035. Municipal and industrial operators are increasingly deploying advanced sensors and automated pumping systems to comply with strict environmental regulations. Strong collaboration between public agencies and private enterprises, coupled with ongoing infrastructure investments, is accelerating market growth.

Key players in the Groundwater Management Market include Arcadis, Black & Veatch, Clean Harbors Environmental Services, DMT Group, Envirogen Technologies, GEI Consultants, Grundfos, HEPACO, HPC AG, iFLUX, INDUS Environmental Services, Koop Wasserbau, Minetek, Remedial Construction Services, Sensoil Innovations, Stantec, SUEZ, Sweco AB, Tetra Tech, The Groundwater Company, Veolia, WJ Group, WSP Global, and Xylem Water Solutions.

Companies in the Groundwater Management Market are employing several strategies to enhance their market presence. They are investing in R&D to develop smart, automated, and modular systems with improved monitoring and predictive capabilities. Strategic partnerships with municipalities, industrial operators, and environmental agencies expand market reach and accelerate adoption. Businesses are also focusing on geographic expansion into regions facing water scarcity. Integration of renewable-powered pumps and corrosion-resistant materials ensures adaptability in diverse hydrogeological conditions. Additionally, companies are offering value-added services such as data analytics, maintenance support, and training programs to strengthen client relationships, enhance operational efficiency, and drive long-term growth.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates and calculations

1.2.1 Base year calculation

1.2.2 Market estimates & forecast parameters

1.3 Forecast

1.3.1 Key trends for market estimates

1.3.2 Quantified market impact analysis

1.3.2.1 Mathematical impact of growth parameters on forecast

1.3.3 Scenario analysis framework

1.4 Primary research and validation

1.4.1 Some of the primary sources (but not limited to)

1.5 Data mining sources

1.5.1 Paid Sources

1.5.2 Sources, by region

1.6 Research trail & scoring components

1.6.1 Research trail components

1.6.2 Scoring components

1.7 Research transparency addendum

1.7.1 Source attribution framework

1.7.2 Quality assurance metrics

1.7.3 Our commitment to trust

1.8 Market definitions

Chapter 2 Executive Summary

2.1 Industry synopsis, 2022 - 2035

2.2 Business trends

2.3 Monitoring trends

2.4 Extraction trends

2.5 Recharge trends

2.6 Treatment trends

2.7 End use trends

2.8 Regional trends

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Raw material availability & sourcing analysis

3.1.2 Manufacturing capacity assessment

3.1.3 Supply chain resilience & risk factors

3.1.4 Distribution network analysis

3.2 Regulatory landscape

3.3 Industry impact forces

3.3.1 Growth drivers

3.3.2 Industry pitfalls & challenges

3.4 Growth potential analysis

3.5 Porter's analysis

3.5.1 Bargaining power of suppliers

3.5.2 Bargaining power of buyers

3.5.3 Threat of new entrants

3.5.4 Threat of substitutes

3.6 PESTEL analysis

3.6.1 Political factors

3.6.2 Economic factors

3.6.3 Social factors

3.6.4 Technological factors

3.6.5 Legal factors

3.6.6 Environmental factors

3.7 Cost structure analysis of groundwater management

3.8 Emerging opportunities & trends

3.9 Digitalization & IoT integration

3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis, by region, 2025

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.2.4 Middle East & Africa

4.2.5 Latin America

4.3 Strategic dashboard

4.4 Strategic initiatives

4.4.1 Key partnerships & collaborations

4.4.2 Major M&A activities

4.4.3 Product innovations & launches

4.4.4 Market expansion strategies

4.5 Competitive benchmarking

4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Monitoring, 2022 - 2035 (USD Million)

5.1 Key trends

5.2 Water quality sensors

5.3 Water level systems

5.4 IoT loggers

5.5 Geospatial analysis

Chapter 6 Market Size and Forecast, By Extraction, 2022 - 2035 (USD Million)

6.1 Key trends

6.2 Pumps

6.3 Borewell drilling

6.4 Well casing & screens

6.5 Integrated infiltration systems

Chapter 7 Market Size and Forecast, By Recharge, 2022 - 2035 (USD Million)

7.1 Key trends

7.2 Artificial recharge structures

7.3 MAR systems

7.4 Recharge wells

7.5 Stormwater infiltration

Chapter 8 Market Size and Forecast, By Treatment, 2022 - 2035 (USD Million)

8.1 Key trends

8.2 Filtration systems

8.3 Pump & treat

8.4 Desalination & chemical treatment

8.5 Biological & in-situ remediation

Chapter 9 Market Size and Forecast, By End Use, 2022 - 2035 (USD Million)

9.1 Key trends

9.2 Agriculture

9.3 Municipal

9.4 Industrial

Chapter 10 Market Size and Forecast, By Region, 2022 - 2035 (USD Million)