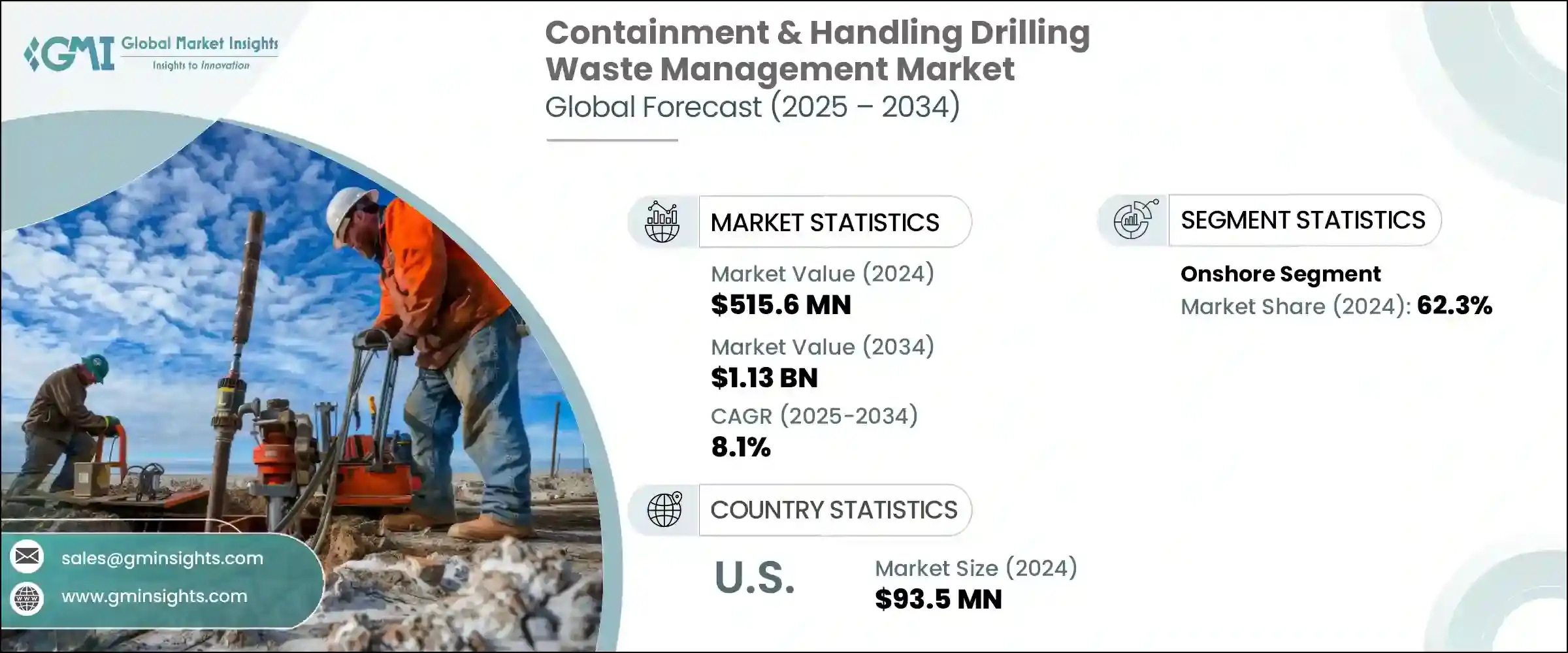

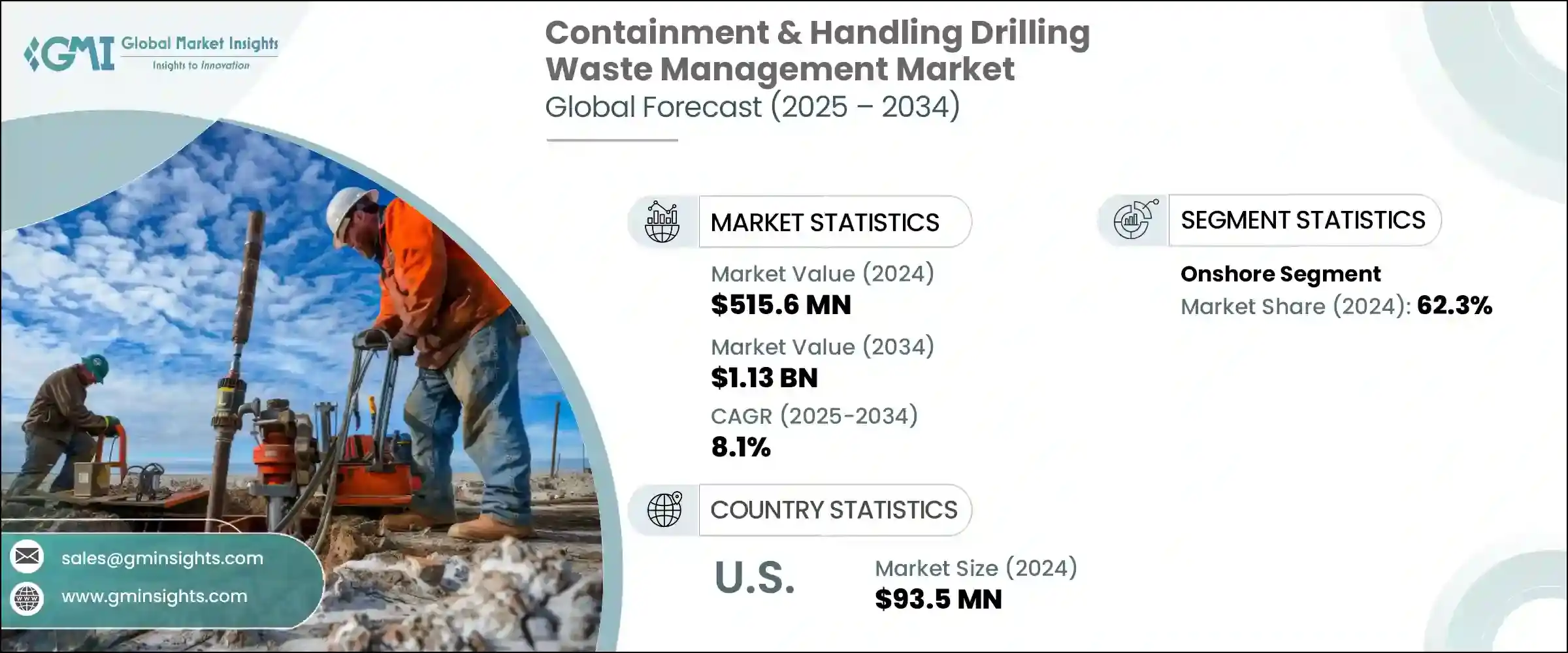

시추 폐기물 봉쇄 및 취급 세계 시장은 2024년에는 5억 1,560만 달러로 평가되었고, CAGR 8.1%로 성장하여 2034년에는 11억 3,000만 달러에 이를 것으로 추정되고 있습니다.

시추 폐기물 처리에 대한 환경 규제가 점점 더 엄격해지고 있는 것이 시장 성장의 주요 요인으로 작용하고 있습니다. 각국 정부는 시추 진흙, 시추 폐기물 및 관련 오염 물질의 관리, 격리 및 최종 처리와 관련하여 생태계에 대한 피해를 최소화하기 위해 더욱 엄격한 정책을 시행하고 있습니다. 이러한 규제 프레임워크의 강화로 인해 기업들은 보다 진보된 폐기물 처리 솔루션을 채택할 수밖에 없습니다.

또한, 현장 폐기물 처리의 개선과 기존의 유성 또는 합성 진흙에 비해 유해 폐기물 발생이 적은 수성 시추 진흙으로 전환하는 것이 시장 역학에 영향을 미치고 있습니다. 그러나 일부 유성 시추 폐기물은 여전히 환경 당국에 의해 유해 폐기물로 분류되어 더 복잡하고 비용이 많이 드는 폐기 처리가 요구되고 있습니다. 이러한 환경적 감시의 강화는 기술 혁신의 급격한 증가를 촉진하고 업계 전반에 걸쳐 대규모 투자를 유치하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 5억 1,560만 달러 |

| 예측 금액 | 11억 3,000만 달러 |

| CAGR | 8.1% |

기업들은 규제 당국의 요구사항을 충족하는 것은 물론 이를 뛰어넘는 첨단 기술과 스마트한 솔루션을 개발하기 위해 노력하고 있습니다. 이러한 움직임은 AI 기반 분석, 실시간 모니터링, 자동 보고 시스템과 같은 최첨단 도구의 채택을 촉진하고 있습니다. 투자자들은 지속 가능한 관행에 장기적인 가치가 있다는 것을 인식하고, 환경 규정 준수와 운영 효율성을 우선시하는 기업에 자본을 투자하고 있습니다. 그 결과, 이 업계는 R&D를 가속화하고, 전략적 파트너십을 구축하며, 제품 포트폴리오를 확장하여 비즈니스 성장을 지원하면서 진화하는 환경 문제에 대응할 수 있도록 설계되고 있습니다.

2024년에는 육상 사업 부문이 62.3%의 점유율을 차지했으며, 이는 다양한 신흥 경제국에서 수압파쇄가 확대되고 있는 데 따른 것입니다. 이러한 대규모 시추 활동은 대량의 드릴스크랩, 역류액, 생산수를 발생시킵니다. 이 모든 물은 하류에서 처리하거나 폐기하기 전에 현장에서 안전한 봉쇄 솔루션이 필요합니다. 자원이 풍부한 지역에서 시추가 강화됨에 따라 확장 가능하고 법규를 준수하는 폐기물 처리 시스템에 대한 수요가 급증하고 있습니다. 운영자들은 환경 규정 준수와 운영 효율성 기준을 모두 충족하기 위해 격리 장비와 현장별 인프라에 대한 투자를 우선순위에 두고 있습니다.

2024년 미국 시장 규모는 9,350만 달러에 달했습니다. 미국과 캐나다는 특히 배출가스, 수자원 안전, 토지 이용에 대한 엄격한 연방 및 지역 환경 규제에 대한 압력이 지속적으로 증가하고 있습니다. 이러한 규제 환경은 셰일암이 많은 지층에서 시추 활동이 활발해지면서 첨단 봉쇄 기술과 지속 가능한 폐기물 처리 체제로의 전환을 가속화하고 있습니다. 생산량을 유지하면서 생태학적 위험을 줄이는 데 중점을 두고 있는 북미에서는 시추 폐기물 관리 관행의 세계 표준을 형성하는 데 있어 북미의 역할이 더욱 강화되고 있습니다.

이 시장에서 활발히 활동하는 기업으로는 Baker Hughes,Schlumberger,Clean Harbors,Halliburton,GN Solids Control,Newpark Resources,TWMA,Derrick Equipment,Secure Energy Services,Imdex,Ridgeline Canada,Imdex,Ridgeline Canada,Soli-Bond,Soli-Bond,Select Water Solutions,Weatherford,Ugean,NOV 등이 있습니다. 시장에서의 입지를 굳히기 위해 주요 기업들은 규제 요구사항에 맞춘 첨단 현장 폐기물 처리 및 봉쇄 시스템 등 기술력 확대에 주력하고 있습니다.

이들 기업은 생태계에 미치는 영향을 줄이고, 보다 안전하고 효율적인 처리 솔루션을 개발하여 진화하는 환경 기준을 준수하는 것을 우선순위로 삼고 있습니다. 전략적 파트너십과 인수는 서비스 제공과 지리적 범위를 넓히기 위해 흔히 이루어지고 있습니다. 많은 기업들이 특히 점성 물질이나 유해 물질과 같은 까다로운 폐기물 흐름을 처리하는 제품 혁신을 강화하기 위해 RandD에 투자하고 있습니다.

The Global Containment and Handling Drilling Waste Management Market was valued at USD 515.6 million in 2024 and is estimated to grow at a CAGR of 8.1% to reach USD 1.13 billion by 2034. Increasingly stringent environmental regulations around the disposal of drilling waste are a primary force shaping market growth. Governments worldwide are enforcing tougher policies on the management, containment, and final disposal of drilling muds, cuttings, and related pollutants to minimize ecological harm. This tightening regulatory framework is compelling companies to adopt more advanced waste-handling solutions.

Additionally, improvements in on-site waste treatment and a shift toward water-based drilling fluids, which produce less hazardous waste compared to traditional oil-based or synthetic muds, are influencing market dynamics. However, some oil-based drilling waste remains classified as hazardous by environmental authorities, leading to more complex and costly disposal requirements. This increasing environmental scrutiny is fueling a surge in innovation and attracting significant investment across industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $515.6 Million |

| Forecast Value | $1.13 Billion |

| CAGR | 8.1% |

Companies are motivated to develop advanced technologies and smarter solutions that not only meet but exceed regulatory demands. This push is encouraging the adoption of cutting-edge tools such as AI-driven analytics, real-time monitoring, and automated reporting systems. Investors recognize the long-term value in sustainable practices, directing capital toward firms that prioritize environmental compliance and operational efficiency. As a result, the industry is witnessing accelerated research and development efforts, strategic partnerships, and expanded product portfolios designed to address evolving environmental challenges while supporting business growth.

In 2024, the onshore operations segment captured a 62.3% share, driven by the expanding footprint of hydraulic fracturing across various emerging economies. These high-volume drilling activities result in significant amounts of drill cuttings, flowback fluids, and produced water-all of which require secure on-site containment solutions before any downstream processing or disposal. As drilling intensifies in resource-rich territories, the demand for scalable and compliant waste-handling systems is rising sharply. Operators are prioritizing investments in containment equipment and site-specific infrastructure to align with both environmental compliance and operational efficiency standards.

United States Containment and Handling Drilling Waste Management Market was valued at USD 93.5 million in 2024. The U.S. and Canada continue to face mounting pressure from rigorous federal and regional environmental regulations, particularly around emissions, water safety, and land use. Combined with heightened drilling activity in shale-rich formations, this regulatory environment has accelerated the shift toward advanced containment technologies and sustainable waste-handling frameworks. The region's focus on reducing ecological risks while maintaining production output further solidifies North America's role in shaping global standards for drilling waste management practices.

Companies actively operating in this market include Baker Hughes, Schlumberger, Clean Harbors, Halliburton, GN Solids Control, Newpark Resources, TWMA, Derrick Equipment Company, Secure Energy Services, Imdex, Ridgeline Canada, Soli-Bond, Select Water Solutions, Weatherford, Augean, and NOV. To solidify their market position, leading players focus on expanding technological capabilities, including advanced on-site waste treatment and containment systems tailored to regulatory demands.

They prioritize compliance with evolving environmental standards by developing safer, more efficient handling solutions that reduce ecological impact. Strategic partnerships and acquisitions are common to broaden service offerings and geographic reach. Many companies invest in RandD to enhance product innovation, particularly around handling challenging waste streams like viscous or hazardous materials.