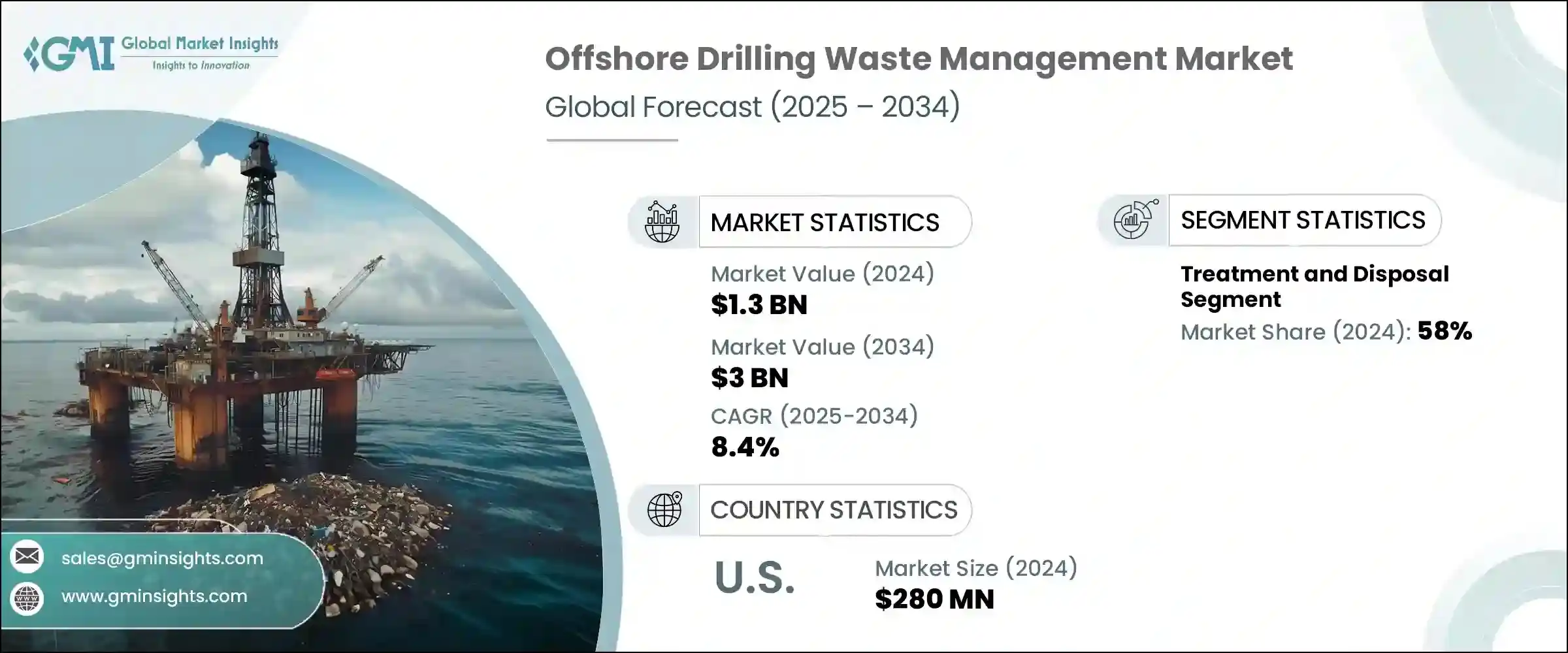

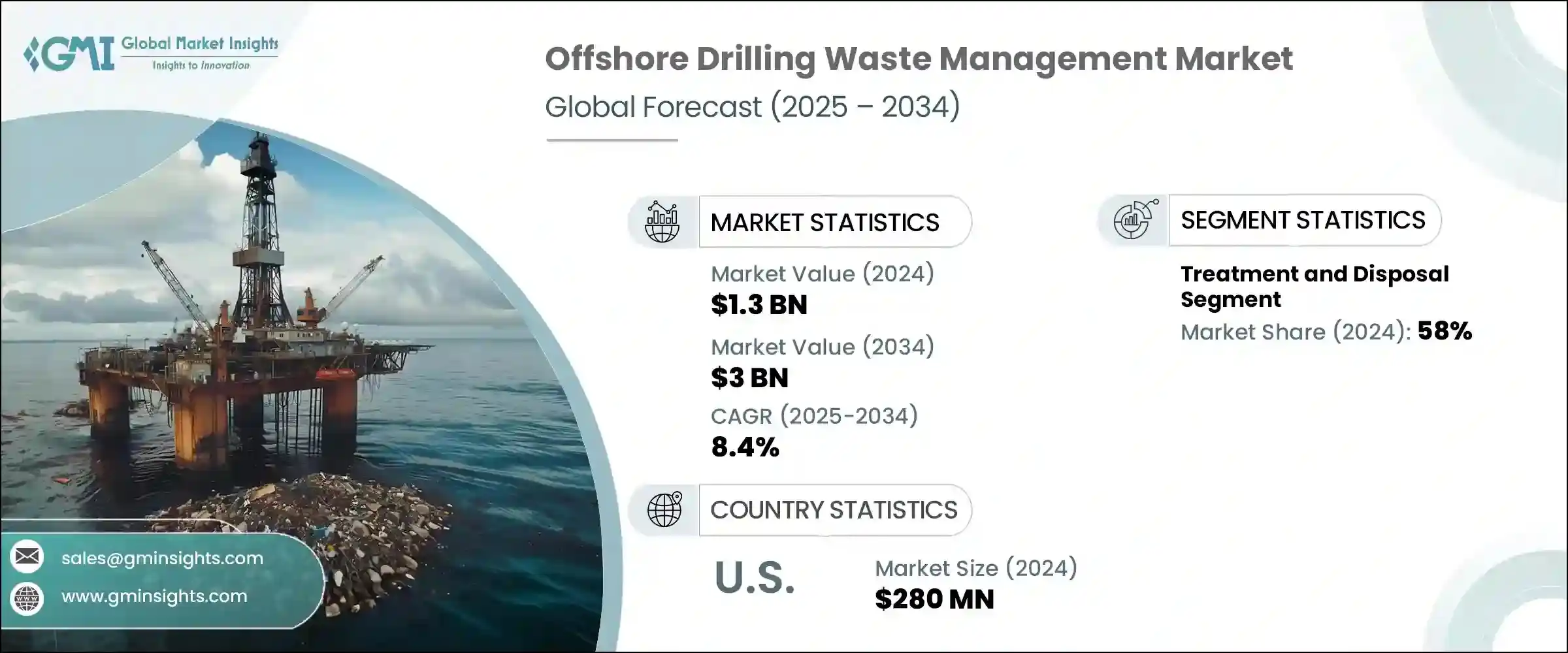

해양 시추 폐기물 관리 세계 시장 규모는 2024년에 13억 달러로 평가되었고, CAGR 8.4%로 성장하여 2034년에는 30억 달러에 이를 것으로 예측됩니다.

이러한 시장 확대는 특히 환경에 미치는 영향이 큰 해양 시추 구역에서 엄격한 환경 규제가 도입되고 있는 것이 주요 요인으로 작용하고 있습니다. 탐사 활동이 심해 및 초심해 지역으로 계속 이동함에 따라 시추 폐기물의 양과 복잡성이 증가하고 있으며, 이에 따라 보다 진보된 고도의 폐기물 관리 솔루션이 요구되고 있습니다. 이러한 성장은 석유 및 가스 산업에서 지속가능성에 대한 관심이 높아짐에 따라 더욱 가속화되고 있으며, 사업자들은 생산 효율을 유지하면서 환경 발자국을 줄여야 하는 상황에 직면해 있습니다.

해양 시추에서는 스추액, 드릴링 찌꺼기, 생산수 등 다양한 폐기물 흐름이 발생하는데, 환경 오염을 방지하기 위해 적절한 봉쇄, 처리 및 처리가 필요합니다. 이에 대응하기 위해 기업들은 해양 환경에서 이러한 물질을 처리하기 위해 특별히 고안된 기술에 많은 투자를 하고 있습니다. 여기에는 폐쇄형 루프 시스템, 특히 생태학적으로 영향을 받기 쉬운 해양 해역에서의 무방류 작업을 지원하는 솔루션이 포함됩니다. 여러 지역의 규제 당국이 규제 준수 조치를 강화함에 따라, 시추 업체들은 폐기물 처리 방법을 개선하고 더 높은 환경 기준을 유지해야 합니다. 이에 따라 해양 폐기물 관리 서비스에 대한 수요가 급증하고 있으며, 이는 책임감 있고 지속 가능한 운영을 향한 업계 전반의 변화를 반영하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 13억 달러 |

| 예측 금액 | 30억 달러 |

| CAGR | 8.4% |

이 시장에서는 효율성 향상, 배출가스 감소, 해양 오염 최소화에 초점을 맞춘 기술 혁신도 눈에 띄게 발전하고 있습니다. 사업자들은 최적의 성능과 규정 준수를 보장하기 위해 실시간 데이터 추적 및 자동화를 제공하는 통합 폐기물 관리 시스템을 도입하는 경향이 증가하고 있습니다. 이러한 디지털 솔루션은 폐기물 구성 및 처리 결과에 대한 통찰력을 제공하여 신속한 의사결정과 비용 관리를 개선할 수 있도록 지원합니다. 이러한 기술의 통합은 업무를 간소화하고 수작업 감독에 대한 의존도를 줄임으로써 폐기물 관리 업무를 혁신적으로 변화시키고 있습니다.

주요 서비스 부문 중 처리 및 폐기 부문은 2024년 시장에서 가장 큰 비중을 차지하며 전체 수익의 약 58%를 차지했습니다. 이 부문에는 열처리, 화학적 중화, 고형화, 생물학적 처리 등 다양한 처리 방법이 포함됩니다. 환경 친화적이고 저배출 처리 솔루션에 대한 선호도가 높아짐에 따라 기존 방식에서 벗어나 장기적인 환경 부채를 줄이는 데 중점을 둔 기업들은 서비스 제공 방식을 바꾸고 있습니다. 해양 사업자들은 특히 폐기물을 현장에서 처리할 수 있는 원위치 처리 옵션을 선호하여 대규모 운송의 필요성을 줄이고 환경 리스크를 최소화하고 있습니다.

미국 시장은 큰 모멘텀을 보이고 있으며, 해양 시추 폐기물 관리 분야 시장 규모는 2022년 2억 3,000만 달러, 2023년 2억 5,000만 달러, 2024년 2억 8,000만 달러에 달했습니다. 이러한 성장에는 엄격한 환경 정책 시행, 해양 시추 프로젝트 확대, 지속가능성에 대한 업계 전반의 관심 증가 등 다양한 요인이 복합적으로 작용하고 있습니다. 시추 강도 증가로 인한 폐기물 발생량 증가는 고급 폐기물 처리 및 봉쇄 솔루션에 대한 수요 증가로 이어졌습니다. 규제 당국이 감시를 강화하고 기술 표준을 강화함에 따라 사업자들은 기존 시스템을 업그레이드하고 보다 안전하고 효과적인 폐기물 처리 방법을 채택해야 할 필요성이 대두되고 있습니다.

시장 경쟁 구도는 다국적 기업과 지역 기업에 의해 형성되고 있으며, 2024년 상위 5개 기업(Baker Hughes, Halliburton, Weatherford, SLB, TWMA)이 세계 시장 점유율의 30% 이상을 차지했습니다. 이들 기업은 종합적인 서비스 포트폴리오, 세계 운영 능력, 기술 혁신의 조합을 통해 그 입지를 굳건히 하고 있습니다. 폐기물 격리부터 처리, 운송, 최종 처리까지 엔드 투 엔드 폐기물 관리 솔루션을 제공할 수 있는 능력은 복잡한 오프쇼어 프로젝트에 대응하는 데 있어 탁월한 강점을 가지고 있습니다. 대형 기업뿐만 아니라, 명성 있는 지역 기업 및 틈새 시장 서비스 제공업체들의 네트워크는 경쟁력을 강화하고 기술 및 운영 모범 사례의 지속적인 발전을 촉진하고 있습니다.

주요 기업들은 효율성과 컴플라이언스를 강화하기 위해 서비스 통합과 디지털 전환을 전략적으로 우선순위에 두고 있습니다. 이들은 단일 서비스 우산 아래 완전한 폐기물 관리 생태계를 제공함으로써 해외 고객의 벤더 조정을 간소화하고, 성능을 최적화하며, 운영 비용을 절감하고 있습니다. 또한, 이들 기업은 실시간 모니터링 시스템과 데이터 분석을 통해 폐기물 처리 프로세스의 추적성을 개선하고 프로젝트 수명주기 전반에 걸쳐 더 나은 의사결정을 내릴 수 있도록 돕고 있습니다. 시장이 진화함에 따라 이러한 혁신은 경쟁력을 유지하고 규제와 지속가능성에 대한 기대치가 높아짐에 따라 이를 충족시키는 데 필수적인 요소가 될 것으로 보입니다.

The Global Offshore Drilling Waste Management Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 3 billion by 2034. The expansion of this market is largely driven by the growing implementation of stringent environmental regulations, particularly in offshore drilling zones where environmental impact is a significant concern. As exploration activities continue to shift toward deepwater and ultra-deepwater locations, the volume and complexity of drilling waste are also rising, demanding more advanced and compliant waste management solutions. This growth is further supported by the increasing emphasis on sustainability within the oil and gas industry, with operators under pressure to reduce their environmental footprint while maintaining production efficiency.

Offshore drilling generates a variety of waste streams, including drilling fluids, drill cuttings, and produced water, all of which require proper containment, treatment, and disposal to prevent environmental contamination. In response, companies are investing heavily in technologies specifically designed to handle these materials in offshore environments. This includes solutions that support closed-loop systems and zero-discharge operations, especially in ecologically sensitive offshore areas. Regulatory agencies across multiple regions are reinforcing compliance measures, compelling drilling companies to adopt advanced waste handling practices and maintain higher environmental standards. As a result, the demand for offshore waste management services has surged, reflecting a broader industry shift toward responsible and sustainable operations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $3 Billion |

| CAGR | 8.4% |

The market has also seen notable advancements in technology, with innovations focused on improving efficiency, reducing emissions, and minimizing marine pollution. Operators are increasingly implementing integrated waste management systems that offer real-time data tracking and automation to ensure optimal performance and compliance. These digital solutions provide insights into waste composition and treatment outcomes, enabling quicker decision-making and improved cost control. The integration of these technologies is transforming waste management practices by streamlining operations and reducing reliance on manual oversight.

Among the key service segments, treatment and disposal accounted for the largest share of the market in 2024, commanding approximately 58% of the overall revenue. This segment includes a wide array of treatment methods such as thermal processing, chemical neutralization, solidification, and biological treatment. The growing preference for eco-friendly and low-emission treatment solutions is reshaping service offerings, with companies moving away from conventional practices and focusing on reducing long-term environmental liabilities. Offshore operators are particularly inclined toward in-situ treatment options that allow waste to be processed on-site, cutting down the need for extensive transport and minimizing environmental risk.

The market in the United States has shown significant momentum, with the offshore drilling waste management sector valued at USD 230 million in 2022, USD 250 million in 2023, and USD 280 million in 2024. This growth is fueled by a combination of factors, including the enforcement of rigorous environmental policies, expansion in offshore drilling projects, and a growing industry-wide focus on sustainability. The rise in waste generation due to increased drilling intensity has led to greater demand for advanced waste processing and containment solutions. With regulatory authorities stepping up oversight and refining technical standards, operators are being pushed to upgrade existing systems and adopt safer, more effective methods for waste handling.

The competitive landscape of the offshore drilling waste management market is shaped by a mix of multinational corporations and regional players. In 2024, the top five companies- Baker Hughes, Halliburton, Weatherford, SLB, and TWMA-together held over 30% of the global market share. These companies have cemented their positions through a combination of comprehensive service portfolios, global operational capabilities, and technological innovation. Their ability to deliver end-to-end waste management solutions-from waste containment to treatment, transportation, and final disposal-gives them a distinct edge in servicing complex offshore projects. Alongside the major players, a network of established regional firms and niche local service providers adds to the competitive intensity, encouraging continuous advancements in technology and operational best practices.

Strategically, leading companies are prioritizing service integration and digital transformation to enhance efficiency and compliance. By offering complete waste management ecosystems under a single service umbrella, they are simplifying vendor coordination for offshore clients while optimizing performance and reducing operational costs. These players are also adopting real-time monitoring systems and data analytics to improve the traceability of waste handling processes and drive better decision-making across project lifecycles. As the market evolves, such innovations are likely to become essential for maintaining competitiveness and meeting rising regulatory and sustainability expectations.