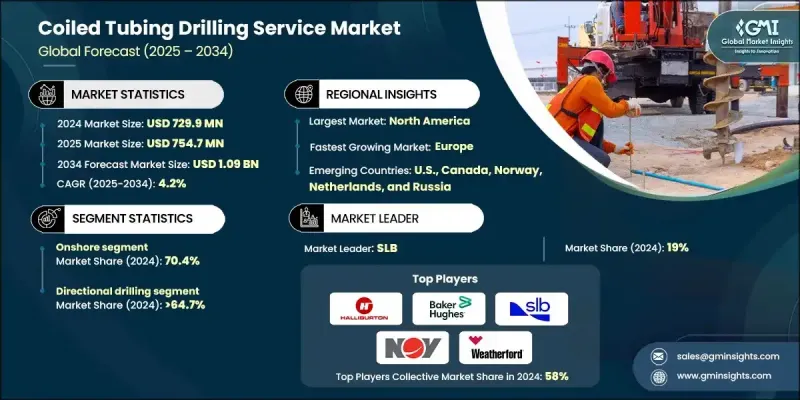

세계의 코일드 튜빙 시추 서비스 시장은 2024년에 7억 2,990만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 4.2%로 성장하여 10억 9,000만 달러에 이를 것으로 예측됩니다.

세계 에너지 수요 증가와 노후화된 석유 및 가스 자산에 대한 유지관리 필요성이 증가하면서 첨단 유정 개입 및 시추 기술에 대한 투자가 가속화되고 있습니다. 특히 재진입 작업이 필요한 저류층에서 복잡한 유정 개입 작업을 보다 안전하고 효율적으로 수행할 수 있는 방법을 찾는 작업자에게 현대식 코일 튜빙 솔루션은 필수 불가결한 요소로 자리 잡고 있습니다. 수평 시추 및 셰일 추출 활동을 지원하는 비재래식 자원의 개발 확대는 코일 튜빙 시스템에 대한 수요를 더욱 증가시키고 있습니다. 어려운 저류층에서 생산량을 극대화하기 위해 노력하는 사업자들은 고성능 추출 전략을 지원하는 통합형 코일 튜빙 기술에 대한 관심이 높아지고 있습니다. 디지털 전환은 산업 구조를 변화시키고 있으며, 자동화와 실시간 모니터링을 통해 특히 해양 환경에서 운영의 정확성과 안전성을 향상시키고 있습니다. 워크플로우의 효율성과 현장의 신뢰성을 강화하고자 하는 기업들 사이에서 최적화된 고효율 시추 솔루션을 제공하는 서비스 제공업체가 점점 더 많이 선택되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 7억 2,990만 달러 |

| 예측 금액 | 10억 9,000만 달러 |

| CAGR | 4.2% |

육상 부문은 2024년 70.4%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 4%로 성장할 것으로 전망됩니다. 셰일 개발의 확대와 광범위한 성숙 인프라의 존재는 육상에서의 지속적인 채택을 뒷받침하고 있으며, 수직, 수평, 방향성 기술을 포함한 다양한 시추 기술이 비재래식 매장량에 접근하기 위해 활용되고 있습니다. 해상 활동 대비 낮은 운영 비용도 부문 성장에 기여하고 있습니다.

방향성 시추 부문은 2024년 64.7%의 점유율을 차지했으며, 2034년까지 연평균 3.5%의 성장이 예상됩니다. 더 깊은 지층과 비재래식 탄화수소 자원에 대한 접근에 대한 요구가 정밀한 유정 제어에 대한 수요를 주도하고 있습니다. 자동 조향 기술과 데이터 기반 시스템의 발전으로 유정 정확도가 향상되고 운영상의 위험성이 감소함에 따라 이 부문이 더욱 확대될 것으로 예측됩니다.

미국 코일 튜빙 시추 서비스 시장은 2024년 62%의 점유율을 차지하며 1억 8,240만 달러의 수익을 창출할했습니다. 타이트 오일과 셰일 유전의 견조한 생산이 시장 발전을 계속 주도하고 있습니다. 실시간 데이터 시스템, 자동화 도구, 강화된 재료 기술의 개선으로 드릴링 성능이 향상되었습니다. 배출량 감소와 유정 건전성 향상을 위한 규제 이니셔티브가 기존 시추공의 효율적인 대안으로 코일 튜빙의 보급을 촉진하는 데 기여하고 있습니다.

The Global Coiled Tubing Drilling Service Market was valued at USD 729.9 million in 2024 and is estimated to grow at a CAGR of 4.2% to reach USD 1.09 billion by 2034.

Rising global energy requirements and the growing need to maintain aging oil and gas assets are accelerating investment in advanced well intervention and drilling technologies. Modern coiled tubing solutions are becoming essential as operators seek safer and more efficient methods for handling complex well interventions, particularly in reservoirs that require re-entry operations. Expanding development of unconventional resources, supported by horizontal drilling and shale extraction activity, is further elevating demand for coiled tubing systems. Operators working to maximize output in challenging reservoirs are showing greater interest in integrated coiled tubing technologies that support high-performance extraction strategies. Digital transformation is also reshaping the landscape, with automation and real-time monitoring improving operational precision and safety, especially in offshore environments. Service providers offering optimized, high-efficiency drilling solutions are increasingly preferred as companies look to streamline workflows and strengthen field reliability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $729.9 Million |

| Forecast Value | $1.09 Billion |

| CAGR | 4.2% |

The onshore segment held a 70.4% share in 2024 and is forecasted to grow at a CAGR of 4% through 2034. Expansion in shale development and the presence of extensive mature infrastructure continue to support onshore adoption, where a wide range of drilling approaches, including vertical, horizontal, and directional techniques, are used to access unconventional reserves. Lower operational expenses compared with offshore activity also contribute to segment growth.

The directional drilling segment held a 64.7% share in 2024 and is anticipated to grow at a 3.5% through 2034. The need to reach deeper formations and unconventional hydrocarbon sources is driving demand for precise wellbore control. Advancements in automated steering technologies and data-driven systems are improving well accuracy and reducing operational hazards, supporting further expansion of this segment.

U.S. Coiled Tubing Drilling Service Market held a 62% share in 2024 and generated USD 182.4 million. Strong production from tight oil and shale fields continues to shape market progress. Improvements in real-time data systems, automation tools, and enhanced material technologies are strengthening drilling performance. Regulatory initiatives aimed at lowering emissions and improving well integrity are encouraging broader adoption of coiled tubing as an efficient alternative to conventional drilling practices.

Prominent companies in the industry include Hunting PLC, TAQA KSA, SLB, Tenaris, Nabors Industries Ltd., AnTech Ltd, GOES GmbH, Halliburton, Oilserv, Weatherford, National Petroleum Services Company (NAPESCO), Baker Hughes, Stena Drilling US Inc., Kleen, HI LONG OIL SERVICE & ENGINEERING CO., LTD., AFG Holdings, Inc., EXCEED (XCD) Holdings Ltd., Blade Energy Partners, Pruitt, FracJet-Volga LLC, and Granite Construction Inc. Companies operating in the Global Coiled Tubing Drilling Service Market are adopting targeted strategies to strengthen their competitive position. Many are upgrading their service portfolios with automation-based drilling systems, high-strength tubing materials, and enhanced downhole tools to improve performance in complex reservoir conditions. Partnerships with operators and technology developers are helping service providers expand capabilities and deliver integrated solutions tailored to unconventional and offshore environments. Firms are also investing in digital monitoring platforms, predictive maintenance technologies, and real-time analytics to boost operational safety and increase efficiency.