실리콘 나노와이어 배터리 기술 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Silicon Nanowire Battery Technology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1885869

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

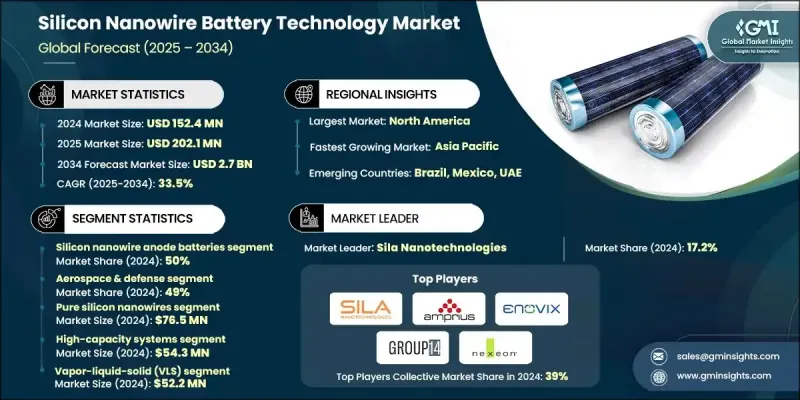

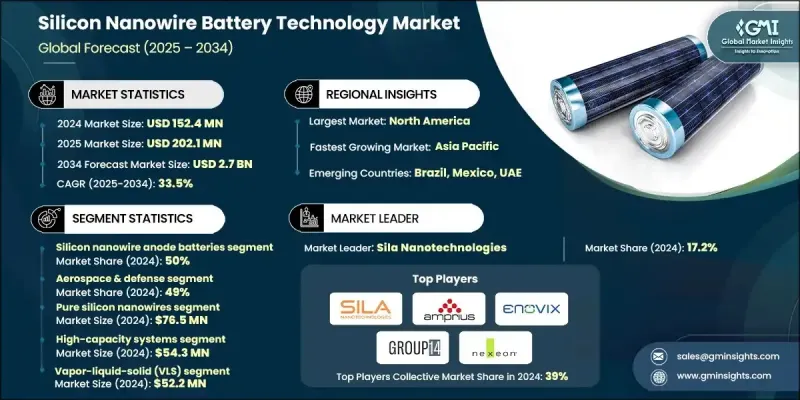

세계의 실리콘 나노와이어 배터리 기술 시장은 2024년 1억 5,240만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 33.5%를 나타낼 것으로 예측되며 27억 달러로 성장할 전망입니다.

이러한 강력한 성장 동력은 고에너지밀도 저장 시스템으로의 전환, 급증하는 전기 모빌리티, 그리고 소비자 가전, 자동차, 고정형 에너지 저장 등 주요 산업 전반에 걸친 첨단 배터리 화학 기술의 확대 적용에서 비롯됩니다. 에너지 저장 요구사항이 높은 내구성, 빠른 충전, 긴 수명을 요구하는 방향으로 진화함에 따라 제조업체들은 재료 과학, 확장 가능한 제조 기술, 디지털로 강화된 개발 경로의 혁신에 점점 더 집중하고 있습니다. 이러한 노력은 안전성, 실제 성능, 상용화 준비를 보장하기 위한 것입니다. 또한 정교한 엔지니어링 도구의 통합이 개발을 간소화하고 프로토타이핑 기간을 단축시켜 기업들이 차세대 배터리를 주류로 채택하도록 추진함으로써 시장 발전이 더욱 강화되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 가치

1억 5,240만 달러

예측 가치

27억 달러

CAGR

33.5%

AI 기반 소재 연구, IoT 연계 모니터링 플랫폼, 클라우드 기반 배터리 관리 시스템에 대한 의존도가 높아지면서 나노 소재 배터리 기술의 진화 방식이 변화하고 있습니다. 이러한 솔루션은 개발자에게 전기화학적 활동에 대한 지속적인 인사이트을 제공하고, 열화 추세를 조기에 예측할 수 있게 하며, 연구 단위, 파일럿 시설 및 통합 파트너 간에 동기화된 워크플로우 관리를 지원합니다. 디지털 트윈, 머신 러닝 시뮬레이션 및 자동화 테스트 플랫폼의 사용은 검증 주기를 가속화하고, 에너지 유지력을 향상시키며, 개발 비용을 절감하여 지능형 배터리 생태계로의 전환을 지원합니다.

실리콘 나노와이어 음극 배터리 부문은 2024년 50%의 점유율을 기록했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR)은 32.9%로 성장할 것으로 예상됩니다. 이러한 음극 시스템은 에너지 밀도, 전도성 및 내구성을 획기적으로 개선하도록 설계되었습니다. 그 구조는 기존 흑연에서 발견된 한계를 해결하면서 더 많은 리튬 이온 흡수를 가능하게 합니다. 운송, 전자기기, 항공우주 부문에서 배터리 수명 연장에 대한 수요가 증가함에 따라 산업계가 더 신뢰할 수 있고 고출력 저장 기술을 추구하면서 순수 실리콘 나노와이어 음극의 채택이 지속적으로 강화되고 있습니다.

항공우주 및 방위 부문은 2024년 49%의 점유율을 기록했으며, 2034년까지 연평균 복합 성장률(CAGR)은 33.1%로 성장할 것으로 예상됩니다. 이 부문의 우위는 가혹한 운영 환경에서도 작동 가능한 경량, 고용량, 고성능 전력 솔루션에 대한 필요성에 의해 주도됩니다. 실리콘 나노와이어 음극 시스템은 높은 출력 대 중량 비율, 빠른 충전, 강력한 운영 내구성을 제공하여 해당 부문의 첨단 장비 요구를 지원합니다. 탄력적인 에너지 시스템에 대한 수요가 증가함에 따라 나노구조 재료, 첨단 열 제어 시스템, AI 기반 모델링 도구에 대한 지속적인 투자가 해당 부문의 리더십을 강화하고 있습니다.

미국의 실리콘 나노와이어 배터리 기술 시장은 2024년에 88%의 점유율을 차지하며 약 4,960만 달러 시장 규모를 창출했습니다. 이 위상은 확립된 전기차 및 배터리 생산 환경, 강력한 연구개발 인프라, 선도적 나노소재 혁신 기업들의 상당한 참여에 의해 뒷받침됩니다. 고용량 실리콘 나노와이어 배터리의 채택은 전기 운송, 소비자 기기, 그리드 수준 저장 부문에서 가속화되고 있습니다. 미국 전역의 기업들은 배터리 안전성 향상, 효율성 개선, 운영 지능 강화를 위해 인공지능 기반 진단, 사물인터넷 연결 모니터링 솔루션, 클라우드 지원 관리 소프트웨어를 도입하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

고에너지밀도 배터리 수요 증가

나노소재 공학 및 AI 기반 소재 최적화 발전

급속 충전 인프라와 고전력 용도 성장

자동차 OEM 및 배터리 제조업체의 투자 증가

업계의 잠재적 위험 및 과제

높은 생산비용과 확장성의 과제

기계적 불안정성과 열화 위험

시장 기회

전기자동차(EV)의 보급 확대와 차량 전동화

거치형 에너지 저장의 확대

그리드 규모 및 재생 에너지 저장 시스템으로의 확장

순환 경제에 부합하는 재활용 기술 개발

성장 가능성 분석

규제 상황

나노소재 규제 및 TSCA(유해 물질 규제법)에 준거

노동안전보건요건 및 NIOSH 가이드라인

환경 영향 규제 및 EPA 기준

국제 규격과 조화를 위한 대처

제품 안전 및 시험 요건

인증 공정 및 품질 보증

규제 타임라인과 미래 정책 변경

규정 준수 비용 분석 및 구현 전략

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

기술 진화의 타임라인과 이정표

기술별 성능 향상 예측

비용 절감 로드맵과 경제 목표

제조 스케일 업의 타임라인과 생산 능력 계획

신흥기술의 통합과 융합

시장 침투 시나리오와 보급 곡선

파괴적 기술에 의한 위협과 시장에 미치는 영향

장기적인 시장 기회와 전략적 비전

기술 이전과 상업화의 길

혁신 생태계와 협력 네트워크

가격 동향

지역별

제품별

생산 통계

생산 거점

소비 거점

수출과 수입

비용 내역 분석

특허 분석

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산의 에너지 효율

환경에 배려한 대처

최상의 시나리오

제조의 확장성과 상업화 로드맵

대체 기술과의 성능 비교 매트릭스

설비 투자와 자금 조달 환경

성능 열화와 사이클 수명 분석

전해액 및 세퍼레이터의 혁신 동향

배터리 팩 통합 및 시스템 레벨 설계

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

주요 동향

실리콘 나노와이어 음극 배터리

실리콘 나노와이어 복합 배터리

하이브리드 나노구조 배터리

제6장 시장 추계 및 예측 제조 방법별(2021-2034년)

주요 동향

기체-액체-고체(VLS) 성장

금속 보조 화학 에칭(MACE)

화학 기상 성장법(CVD)

용액 기반 성장법

전기화학적 증착법

제7장 시장 추계 및 예측 : 성능 카테고리별(2021-2034년)

주요 동향

대용량 시스템

급속 충전 시스템

긴 수명 사이클 시스템

비용 최적화 시스템

제8장 시장 추계 및 예측 : 재료 조성별(2021-2034년)

주요 동향

순수 실리콘 나노와이어

실리콘 탄소 복합재료

실리콘 산화물 복합재료

실리콘 합금 나노와이어

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

항공우주 및 방위

자동차

소비자 가전

거치형 에너지 저장

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

벨기에

네덜란드

스웨덴

아시아태평양

중국

인도

일본

호주

싱가포르

한국

베트남

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

아랍에미리트(UAE)

남아프리카

사우디아라비아

제11장 기업 프로파일

세계적 기업

Amprius Technologies

BTR New Material

Group14 Technologies

LG Energy Solution

Nexeon

OneD Material

Panasonic Energy

SamsungSDI

Shanshan Technology

Sila Nanotechnologies

지역 기업

DAEJOO Electronic Materials

Enevate

Gotion High-tech

GUIBAO Science &Technology

IOPSILION

KINGi New Materials

LeydenJar Technologies

NanoGraf

NEO Battery Materials

StoreDot

신흥 기업

11.3.1. DBattery

Advano

HKG Energy

Nanoramic Laboratories

Solid Power

HBR

영문 목차

영문목차

The Global Silicon Nanowire Battery Technology Market was valued at USD 152.4 million in 2024 and is estimated to grow at a CAGR of 33.5% to reach USD 2.7 billion by 2034.

Strong momentum comes from the shift toward high-energy-density storage systems, surging electric mobility, and broader use of advanced battery chemistries across major sectors such as consumer electronics, automotive, and stationary energy storage. As energy storage requirements evolve to demand higher durability, faster charging, and longer life cycles, manufacturers are increasingly focusing on breakthroughs in material science, scalable fabrication techniques, and digitally enhanced development pathways. These efforts are aimed at ensuring safety, real-world performance, and readiness for commercial deployment. The market's progress is also reinforced by greater integration of sophisticated engineering tools that streamline development and reduce prototyping timelines, enabling companies to push next-generation batteries toward mainstream adoption.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$152.4 Million

Forecast Value

$2.7 Billion

CAGR

33.5%

Growing reliance on AI-driven material research, IoT-linked monitoring platforms, and cloud-based battery management systems is transforming how nanomaterial battery technologies evolve. These solutions give developers continuous insight into electrochemical activity, allow early prediction of degradation trends, and support synchronized workflow management across research units, pilot facilities, and integration partners. The use of digital twins, machine-learning simulations, and automated testing platforms helps accelerate validation cycles, enhance energy retention, and cut down development expenditures, supporting the transition toward intelligent battery ecosystems.

The silicon nanowire anode batteries segment captured a 50% share in 2024 and is estimated to grow at a CAGR of 32.9% between 2025 and 2034. These anode systems are engineered to deliver substantial improvements in energy density, conductivity, and durability. Their structure enables greater lithium-ion intake while addressing limitations found in conventional graphite. Rising demand for extended battery life in transportation, electronics, and aerospace applications continues to strengthen the adoption of pure silicon nanowire anodes as industries pursue more reliable and high-output storage technologies.

The aerospace and defense segment held a 49% share in 2024 and is expected to grow at a CAGR of 33.1% through 2034. Its dominance is driven by the need for lightweight, high-capacity, and high-performance power solutions capable of functioning in harsh operating environments. Silicon nanowire anode systems offer high power-to-weight ratios, rapid charging, and strong operational endurance, which support the sector's advanced equipment needs. Continuous investments in nanostructured materials, advanced thermal-control systems, and AI-based modeling tools strengthen the segment's leadership as demand for resilient energy systems grows.

United States Silicon Nanowire Battery Technology Market held an 88% share in 2024, generating approximately USD 49.6 million. This position is supported by a well-established EV and battery production landscape, strong R&D infrastructure, and significant involvement from leading nanomaterials innovators. Adoption of high-capacity silicon nanowire batteries has accelerated across electric transportation, consumer devices, and grid-level storage. Companies across the U.S. are deploying AI-enabled diagnostics, IoT-connected monitoring solutions, and cloud-supported management software to increase battery safety, improve efficiency, and enhance operational intelligence.

Key companies active in the Silicon Nanowire Battery Technology Market include Amprius Technologies, BTR New Material, Enevate, ENOVIX, Group14 Technologies, Nexeon, OneD Battery Sciences, ShinEtsu Chemical, Sila Nanotechnologies, and XG Sciences. Companies involved in the Silicon Nanowire Battery Technology Market are focusing on several strategic approaches to strengthen their competitive standing. Many firms are expanding their manufacturing capacities to support commercialization and ensure a consistent supply. Heavy emphasis is placed on R&D programs that enhance energy density, improve cycle stability, and optimize nanowire structures. Collaborations with EV makers, electronics brands, and defense contractors help accelerate real-world adoption. Businesses are also integrating AI-based analytics, digital twins, and automated testing systems to shorten development cycles and reduce costs.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Fabrication Method

2.2.4 Performance Category

2.2.5 Material Composition

2.2.6 Application

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising demand for high-energy-density batteries

3.2.1.2 Advancements in nanomaterial engineering and ai-based material optimization

3.2.1.3 Growth of fast-charging infrastructure and high-power applications

3.2.1.4 Increasing investments from automotive OEMs and battery manufacturers

3.2.2 Industry pitfalls and challenges

3.2.2.1 High production costs and scalability challenges

3.2.2.2 Mechanical instability and degradation risks

3.2.3 Market opportunities

3.2.3.1 High EV adoption and fleet electrification

3.2.3.2 Expansion of stationary energy storage

3.2.3.3 Expansion into grid-scale and renewable energy storage systems

3.2.3.4 Development of circular-economy-aligned recycling technologies