시추 유체 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Drilling Fluid Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1885828

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 160 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

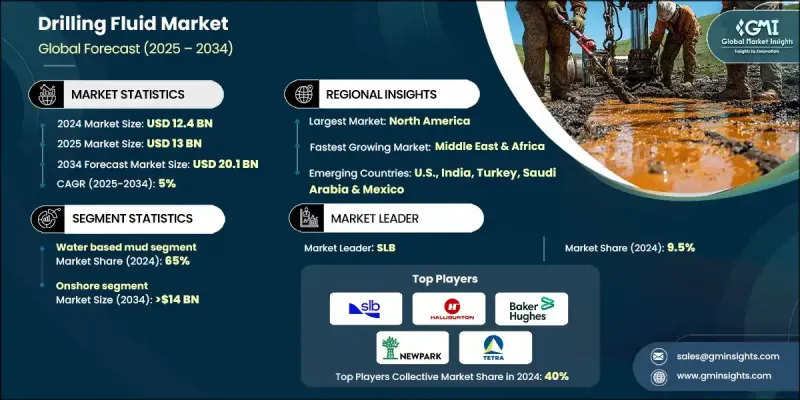

세계의 시추 유체 시장은 2024년에 124억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5%로 성장할 전망이며, 201억 달러에 이를 것으로 예측됩니다.

업계의 확대는 환경 규제 강화 및 운영 효율성과 갱정의 무결성에 대한 주목 증가에 의해 추진되고 있습니다. 현대 시추 작업은 지속가능성 목표와 운영 효율성을 모두 지원하기 위해 지상 손상을 최소화하면서 시추 성능을 향상시키는 환경 친화적인 고성능 유체 시스템의 사용이 증가하고 있습니다. 시추 유체(수계, 유계, 합성계를 불문하고)는 석유 및 가스 탐사에 있어서, 드릴 비트의 냉각 및 윤활, 굴삭 쓰레기의 지표에 대한 반송, 갱정 안정성의 유지를 목적으로 사용되는 화학적으로 설계된 배합제입니다. 그 역할은 단순한 순환 기능을 넘어 갱정 압력 제어, 성능 최적화, 비용 효율화를 위한 전략적 도구로 진화하고 있습니다. 재사용가능하고 재활용가능한 제제는 경제적 우위를 더욱 높여 현대의 시추 작업에서 중요한 자산으로서의 지위를 강화하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 시 가치

124억 달러

예측 금액

201억 달러

CAGR

5%

수계 진흙 부문은 2024년에 65%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 5%로 성장할 것으로 예측됩니다. 적응성 및 환경 친화적인 특성으로 인해 얕은 층과 중층 우물에서 우선적으로 선택됩니다. 지속가능한 드릴링 기법에 중점을 두고 낮은 독성 유체에 대한 규제 지원이 채택 확대와 시장 성장을 지속적으로 추진할 것입니다.

육상 시추 유체 부문은 2024년에 75.3%의 점유율을 획득했으며, 2034년까지 140억 달러에 이를 것으로 예측됩니다. 육상 작업은 비용 효율적이고 환경에 안전한 유체를 선호하며 육상 탐사 프로젝트의 규모에서 안정적인 수요가 예상됩니다. 각국이 국내 석유 및 가스 생산을 확대함에 따라 갱정 개발이 확대되고 시추액 공급업체에게 안정적인 기회가 창출되어 시장 확대를 지지하고 있습니다.

미국의 시추 유체 시장은 2024년에 72%의 점유율을 차지했으며, 43억 달러의 규모가 되었습니다. 규제 준수와 환경을 배려한 유체에 대한 정부 지원책이 맞물려 시장 상황이 강화되고 있습니다. 생산성이 높은 분지에 있어서 국내 석유 및 가스 생산에 대한 주력이 고성능 굴삭 유체의 높은 수요를 견인하고 있어, 공급업자에게 있어서 계속적인 성장 기회가 확보되고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

원재료 가용성 및 조달 분석

제조 능력 평가

공급망의 회복력 및 리스크 요인

유통 네트워크 분석

규제 상황

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 위험 및 과제

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

시추 유체의 비용 구조 분석

새로운 기회 및 동향

디지털화 및 IoT 통합

투자 분석 및 전망

제4장 경쟁 구도

서문

기업의 시장 점유율 분석 : 지역별

북미

유럽

아시아태평양

중동 및 아프리카

라틴아메리카

전략적 대시보드

전략적 노력

주요 제휴 및 협력관계

주요 M&A 활동

제품 혁신 및 신제품 출시

시장 확대 전략

경쟁 벤치마킹

혁신과 지속가능성의 정세

제5장 시장 규모 및 예측 : 제품 유형별(2021-2034년)

주요 동향

수계 진흙

유성 진흙

합성계 진흙

기타

제6장 시장 규모 및 예측 : 용도별(2021-2034년)

주요 동향

온쇼어

오프쇼어

제7장 시장 규모 및 예측 : 우물 유형별(2021-2034년)

주요 동향

기존

HPHT

제8장 시장 규모 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

튀르키예

루마니아

영국

이탈리아

러시아

네덜란드

노르웨이

아시아태평양

중국

일본

인도네시아

인도

호주

태국

중동 및 아프리카

사우디아라비아

아랍에미리트(UAE)

카타르

이집트

알제리

리비아

나이지리아

쿠웨이트

오만

라틴아메리카

브라질

멕시코

콜롬비아

아르헨티나

제9장 기업 프로파일

AES Drilling Fluids

Baker Hughes

BCS Fluids

Cargill

CES Energy Solutions Corp

Chevron Phillips Chemical Company

Di-Corp

Eco Drilling Fluids

Gumpro Drilling Fluids

Halliburton

INEOS

Ingevity

International Drilling Fluids

National Energy Services Reunited Corp

Newpark Drilling Fluids

SLB

Stellar Drilling Fluids

SumiSaujana

SUPREME DRILLING FLUID CHEMICALS

Universal Performance Chemicals

AJY

영문 목차

영문목차

The Global Drilling Fluid Market was valued at USD 12.4 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 20.1 billion by 2034.

Industry expansion is driven by rising environmental compliance requirements and an increased focus on operational efficiency and well integrity. Modern drilling operations are increasingly utilizing eco-friendly, high-performance fluid systems to enhance drilling outcomes while minimizing formation damage, supporting both sustainability objectives and operational efficiency. Drilling fluids, whether water-based, oil-based, or synthetic, are engineered chemical formulations used in oil and gas exploration to cool and lubricate the drill bit, transport cuttings to the surface, and maintain wellbore stability. Their role has evolved beyond basic circulation to a strategic tool for wellbore pressure control, performance optimization, and cost efficiency. Reusable and recyclable formulations have created additional economic advantages, reinforcing their position as critical assets in modern drilling operations.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$12.4 Billion

Forecast Value

$20.1 Billion

CAGR

5%

The water-based mud segment accounted for a 65% share in 2024 and is projected to grow at 5% CAGR through 2034. Its adaptability and environmentally friendly nature make it the preferred choice for shallow and medium-depth wells. The emphasis on sustainable drilling practices and regulatory support for low-toxicity fluids will continue to drive adoption and market growth.

The onshore drilling fluid segment captured a 75.3% share in 2024 and is expected to reach USD 14 billion by 2034. Onshore operations favor cost-effective, environmentally safe fluids, fueling consistent demand due to the volume of land-based exploration projects. As countries increase domestic oil and gas production, well development expands, creating steady opportunities for drilling fluid suppliers and supporting market expansion.

U.S. Drilling Fluid Market held a 72% share in 2024, generating USD 4.3 billion. Regulatory compliance, combined with government incentives for greener fluids, has enhanced the market landscape. High demand for high-performance drilling fluids is being driven by a focus on domestic oil and gas production in prolific basins, ensuring continuous growth opportunities for suppliers.

Key players in the Global Drilling Fluid Market include Stellar Drilling Fluids, Eco Drilling Fluids, Baker Hughes, Universal Performance Chemicals, Di-Corp, INEOS, Newpark Drilling Fluids, Halliburton, BCS Fluids, Cargill, Gumpro Drilling Fluids, Tetra Technologies, Chevron Phillips Chemical Company, CES Energy Solutions Corp, AES Drilling Fluids, Ingevity, Supreme Drilling Fluid Chemicals, and SumiSaujana. Companies in the Drilling Fluid Market are prioritizing innovation to develop environmentally friendly and high-performance fluid formulations. Investment in research and development ensures that fluids meet evolving regulatory standards while enhancing wellbore stability and drilling efficiency. Strategic partnerships with drilling contractors, service providers, and oilfield operators expand market access and strengthen supply chains. Firms are leveraging reusable and recyclable fluid technologies to reduce operational costs and appeal to sustainability-focused clients. Geographic expansion into high-growth regions ensures access to emerging drilling projects.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates and calculations

1.2.1 Base year calculation

1.2.2 Market estimates & forecast parameters

1.3 Forecast

1.3.1 Key trends for market estimates

1.3.2 Quantified market impact analysis

1.3.2.1 Mathematical impact of growth parameters on forecast

1.3.3 Scenario analysis framework

1.4 Primary research and validation

1.4.1 Some of the primary sources (but not limited to)

1.5 Data mining sources

1.5.1 Paid Sources

1.5.2 Sources, by region

1.6 Research trail & scoring components

1.6.1 Research trail components

1.6.2 Scoring components

1.7 Research transparency addendum

1.7.1 Source attribution framework

1.7.2 Quality assurance metrics

1.7.3 Our commitment to trust

1.8 Market definitions

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021 - 2034

2.2 Business trends

2.3 Product type trends

2.4 Application trends

2.5 Well type trends

2.6 Regional trends

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Raw material availability & sourcing analysis

3.1.2 Manufacturing capacity assessment

3.1.3 Supply chain resilience & risk factors

3.1.4 Distribution network analysis

3.2 Regulatory landscape

3.3 Industry impact forces

3.3.1 Growth drivers

3.3.2 Industry pitfalls & challenges

3.4 Growth potential analysis

3.5 Porter's analysis

3.5.1 Bargaining power of suppliers

3.5.2 Bargaining power of buyers

3.5.3 Threat of new entrants

3.5.4 Threat of substitutes

3.6 PESTEL analysis

3.6.1 Political factors

3.6.2 Economic factors

3.6.3 Social factors

3.6.4 Technological factors

3.6.5 Legal factors

3.6.6 Environmental factors

3.7 Cost structure analysis of drilling fluid

3.8 Emerging opportunities & trends

3.9 Digitalization & IoT integration

3.10 Investment analysis & future outlook

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis, by region, 2024

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.2.4 Middle East & Africa

4.2.5 Latin America

4.3 Strategic dashboard

4.4 Strategic initiatives

4.4.1 Key partnerships & collaborations

4.4.2 Major M&A activities

4.4.3 Product innovations & launches

4.4.4 Market expansion strategies

4.5 Competitive benchmarking

4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product Type, 2021 - 2034 (USD Million)

5.1 Key trends

5.2 Water based mud

5.3 Oil based mud

5.4 Synthetic based mud

5.5 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Million)

6.1 Key trends

6.2 Onshore

6.3 Offshore

Chapter 7 Market Size and Forecast, By Well Type, 2021 - 2034 (USD Million)

7.1 Key trends

7.2 Conventional

7.3 HPHT

Chapter 8 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)