특수 유전용 화학제품 시장 : 유형별, 저류층 유형별, 용도별, 지역별 예측(-2030년)

Specialty Oilfield Chemicals Market by Type, Reservoir Type, Application (Production, Well Stimulation, Drilling Fluids, Enhanced Oil Recovery, Cementing, and Workover & Completion), and Region - Global Forecast to 2030

상품코드:1804852

리서치사:MarketsandMarkets

발행일:2025년 08월

페이지 정보:영문 318 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

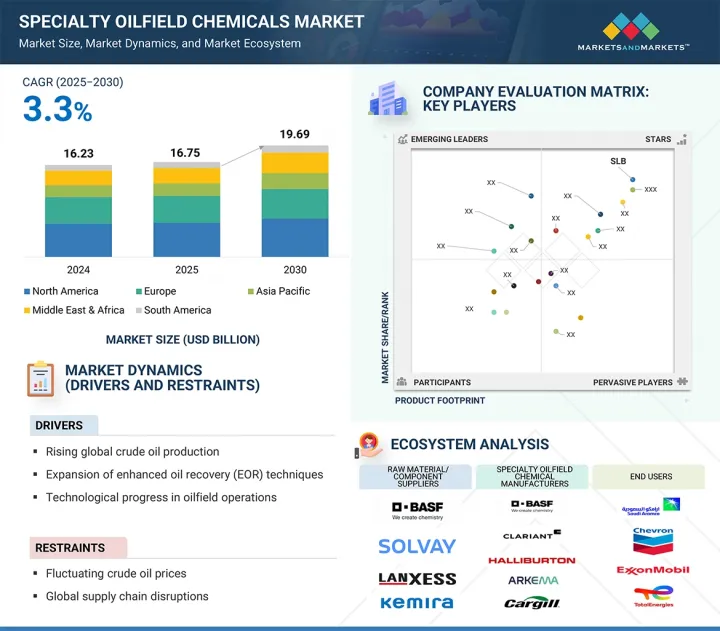

특수 유전용 화학제품 시장 규모는 예측기간 동안 3.3%의 연평균 성장률(CAGR)로 확대되어 2025년 167억 5,000만 달러에서 2030년에는 196억 9,000만 달러에 이를 것으로 예측되고 있습니다.

조사 범위

조사 대상 연도

2021-2030년

기준 연도

2024년

예측 기간

2025-2030년

검토 단위

금액(100만 달러) 및 킬로톤(KT)

부문

유형별, 저류층 유형별, 용도별, 지역별

대상 지역

북미, 아시아태평양, 유럽, 중동, 아프리카, 남미

특수 유전용 화학제품 시장은 지속 가능하고 효율적인 유전 화학 제품에 대한 상류 석유 및 가스 운영의 수요로 인해 꾸준한 성장을 경험하고 있습니다. 심해 및 비전통적 저류층과 같은 극한 환경에서 이러한 화학 물질은 유정의 무결성을 유지하고 시추 작업을 최적화하면서 저류층에서 석유 추출을 향상시킵니다.

이 사업은 화학 물질 사용, 독성 및 환경 영향에 대해 더 엄격한 규칙을 시행하고 있는 미국 환경 보호국(EPA) 및 유럽 화학 물질청(ECHA)과 같은 규제 기관의 지원을 받아 왔습니다. 제조업체들은 이에 대응하여 더 지속 가능하고 생분해성이며 저휘발성 유기화합물(VOC) 제품을 개발하고 있습니다. 이러한 규제 움직임은 정밀 화학 및 친환경 제품 개발의 진전을 가속화했습니다. 이러한 제품 접근 방식에서 점점 더 보편화되는 특징은 신속한 대응과 규정 준수를 개선하기 위한 실시간 모니터링 및 스마트 화학 물질 공급 시스템입니다. 특수 유전용 화학 제품은 탐사가 어려운 지역으로 확장됨에 따라 상류 에너지 작업이 안전하고 효율적이며 환경적으로 지속 가능하도록 보장하는 데 중요합니다.

2024년 특수 유전용 화학제품 시장에서 유동점 강하제가 가장 큰 비중을 차지했는데, 이는 저온 환경에서 원유 흐름을 촉진하는 데 핵심적인 역할을 하기 때문입니다. 이 화학 물질은 왁스 결정이 형성되는 온도를 낮춰 파이프라인 막힘을 방지하고, 특히 추운 기후와 해양 작업에서 효과적인 원유 수송을 가능하게 합니다. 러시아, 캐나다, 중동 일부 지역과 같은 고왁스 및 고점도 원유 지역에서 이들의 사용은 특히 중요합니다. 심해 및 북극 유전의 생산 증가와 함께 신뢰할 수 있는 유동성 보장 솔루션에 대한 수요 증가가 특수 유전용 화학제품 시장 내 유동점 저하제의 우위를 지속적으로 뒷받침하고 있습니다.

효율적인 추출 방법에 대한 요구로 유전 운영의 복잡성이 증가함에 따라 2024년 생산 부문이 특수 유전 화학 시장 주도권을 장악했습니다. 인프라 보호와 함께 증강된 석유·가스 생산 및 수율 증대를 위해서는 스케일 억제제 및 부식 억제제와 함께 유화분리제가 필수적으로 사용되어야 합니다. 특히 산업 및 전력 부문의 에너지 수요가 지속적으로 증가함에 따라 전통적 및 현대적 유전 모두에서 생산 활동이 증가하고 있습니다. 이 부문은 까다로운 조건을 위한 화학 공식 발전과 환경 규제 준수를 통해 시장 선도적 위치를 유지하며, 전 세계 시장에서 안전하고 경제적인 석유 생산을 실현합니다.

2024년 북미는 퍼미안 셰일층, 버켄 셰일층, 이글퍼드 셰일층에서 활발한 업스트림 활동을 위해 특수 유전용 화학제품 시장을 독점했습니다. 이 지역에서는 석유증진회수법(EOR)의 보급과 함께 선진적인 굴삭기술이 이용되고 있으며, 환경에 배려한 화학처리를 장려하는 규칙도 정비되고 있습니다. 부식방지제, 스케일방지제, 탈유화제 등의 고성능 화학제품에 대한 수요 증가는 비재래형 매장량으로부터의 생산량 증가에 의해 촉진되고 있습니다. 또한 심해 유전과 타이트 오일 프로젝트에 대한 지속적인 투자와 운영 효율성 개선 및 환경 컴플라이언스에 대한 주력으로 세계의 특수 유전용 화학제품 시장에서 북미 리더십이 확고해지고 있습니다.

대상 기업 : BASF(독일), Clariant(스위스), Dow(미국), Syensqo(벨기에), SLB(미국), Halliburton(미국), Baker Hughes Company(미국), Arkema(프랑스), Cargill, Incorporated(미국), Chevron Phillips Chemical Company LLC(미국)가 대상.

본 조사에서는 특수 유전용 화학제품 시장에서 이러한 주요 기업에 대해 기업 프로파일, 최근 동향, 주요 시장 전략 등의 상세한 경쟁 분석을 제공합니다.

조사 대상

이 조사 보고서는 특수 유전용 화학제품 시장을 유형별, 저류층 유형별, 용도별, 지역별로 분류하고 있습니다. 본 보고서의 조사 범위는 특수 유전용 화학제품 시장의 성장에 영향을 주는 촉진요인 및 시장억제요인과 과제 및 기회에 관한 상세정보를 망라하고 있습니다. 주요 업계 진출 기업을 상세하게 분석하여 사업 개요, 제공 제품, 특수 유전용 화학제품 시장과 관련된 제휴, 협력, 합병, 인수, 제품 발매, 사업 확대 등 주요 전략에 대한 인사이트력을 제공합니다. 이 보고서는 특수 유전용 화학제품 시장 생태계에서 향후 신흥 기업의 경쟁 분석을 다룹니다.

보고서 구매 이유

이 보고서는 특수 유전용 화학제품 시장 전체와 하위 부문 수익의 가장 가까운 근사치에 대한 정보를 시장 리더/신규 참가자에게 제공합니다. 이 보고서는 이해 관계자가 경쟁 구도를 이해하고 비즈니스를 더 잘 파악할 수 있도록 고찰을 심화하고 적절한 시장 진출 전략을 계획하는 데 도움이 됩니다. 본 보고서는 이해관계자가 시장의 박동을 이해하고 주요 시장 성장 촉진요인 및 억제요인과 과제 및 기회에 관한 정보를 제공하는데 도움을 줍니다.

본 보고서에서는 세계의 특수 유전용 화학제품 시장에 대해 조사했으며, 유형별, 저류층 유형별, 용도별, 지역별 동향 및 시장 진출기업 프로파일 등을 정리했습니다.

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 중요 인사이트

제5장 시장 개요

소개

시장 역학

고객의 비즈니스에 영향을 미치는 동향과 혼란

생태계 분석

밸류체인 분석

관세 및 규제 상황

무역 분석

기술 분석

특허 분석

주된 회의와 이벤트(2025-2026년)

사례 연구 분석

투자 및 자금조달 시나리오

생성형 AI/AI가 특수 유전용 화학제품 시장에 미치는 영향

Porter's Five Forces 분석

주요 이해관계자와 구매 기준

거시경제 분석

미국 관세가 특수 유전용 화학제품 시장에 미치는 영향(2025년)

제6장 특수 유전용 화학제품 시장(유형별)

소개

탈유화제

억제제와 제거제

레올로지 개질제

마찰 감소제

특수 살균제

특수 계면활성제

유동점 저하제

기타

제7장 특수 유전용 화학제품 시장(저류층 유형별)

소개

해상

육상

제8장 특수 유전용 화학제품 시장(용도별)

소개

생산

유정 자극

드릴링 유체

석유 회수 강화

시멘트

개수와 완료

제9장 특수 유전용 화학제품 시장(지역별)

소개

북미

미국

캐나다

멕시코

유럽

노르웨이

영국

러시아

카자흐스탄

네덜란드

기타

중동 및 아프리카

GCC 국가

이란

이라크

나이지리아

기타

아시아태평양

중국

인도네시아

인도

말레이시아

태국

기타

남미

브라질

베네수엘라

기타

제10장 경쟁 구도

개요

주요 진입기업의 전략

시장 점유율 분석

수익 분석

기업평가와 재무지표

제품/브랜드 비교

기업평가 매트릭스 : 주요 진입기업(2024년)

기업평가 매트릭스 : 스타스업 및 중소기업(2024년)

경쟁 시나리오

제11장 기업 프로파일

주요 진출기업

SLB

BASF

DOW

CLARIANT

SYENSQO

HALLIBURTON

BAKER HUGHES COMPANY

ARKEMA

CARGILL, INCORPORATED

CHEVRON PHILLIPS CHEMICAL COMPANY LLC

기타 기업

ALBEMARLE CORPORATION

STEPAN COMPANY

INNOSPEC

LUBRIZOL

NOURYON

ASHLAND

THERMAX LIMITED

ELEMENTIS PLC

FLOTEK INDUSTRIES, INC.

GEO

SMC GLOBAL

OLEON NV

PURECHEM SERVICES

STERLING SPECIALTY CHEMICALS

ENROIL

제12장 인접 시장과 관련 시장

제13장 부록

HBR

영문 목차

영문목차

The specialty oilfield chemicals market is expected to reach USD 19.69 billion by 2030 from USD 16.75 billion in 2025, at a CAGR of 3.3% during the forecast period.

Scope of the Report

Years Considered for the Study

2021-2030

Base Year

2024

Forecast Period

2025-2030

Units Considered

Value (USD Million) and Volume (Kiloton)

Segments

Type, Reservoir Type, Application, and Region

Regions covered

North America, Asia Pacific, Europe, Middle East & Africa, and South America

The specialty oilfield chemicals market is experiencing consistent growth, due to the upstream oil and gas operations' demand for sustainable and efficient oilfield chemicals. In extreme circumstances such as deepwater and unconventional reservoirs, these chemicals enhance the extraction of oil from the reservoirs while maintaining the integrity of the wellbore and optimizing drilling operations.

The business has been supported by regulatory bodies like the US Environmental Protection Agency (EPA) and the European Chemicals Agency (ECHA), which are enforcing tougher rules on chemical use, toxicity, and environmental impact. Manufacturers are responding by developing more sustainable, biodegradable, and low-VOC products. This regulatory initiative has accelerated advances in accurate chemistry and green product development. An increasingly common feature in these product approaches is real-time monitoring and smart chemical delivery systems to improve faster action and compliance. Specialty oilfield chemicals are crucial as exploration advances into challenging areas, ensuring that upstream energy operations are safe, efficient, and environmentally sustainable.

"Pour point depressants accounted for the largest share in the specialty oilfield chemicals market in 2024."

In 2024, pour point depressants accounted for the largest share of the specialty oilfield chemicals market, due to their vital role in promoting the flow of crude oil in low-temperature conditions. These chemicals lower the temperature at which wax crystals form, preventing pipeline blockages and promoting effective oil transportation, especially in cold climates and offshore operations. Their use is particularly critical in high-wax, high-viscosity crude regions such as Russia, Canada, and parts of the Middle East. The growing production from deepwater and arctic fields, along with rising demand for reliable flow assurance solutions, continues to support the dominance of pour point depressants in the specialty oilfield chemicals market.

"Production segment accounted for the largest share of the specialty oilfield chemicals market in 2024."

The increasing complexity of oilfield operations with the requirement for efficient extraction methods led to the production sector dominating the specialty oilfield chemicals market in 2024. The protection of infrastructure alongside enhanced oil and gas production and increased yield requires the essential use of demulsifiers in combination with scale inhibitors and corrosion inhibitors. Both traditional and modern reservoirs witness rising production activities because energy demand continues to increase, particularly from industrial and power sectors. The segment maintains its market leadership position through chemical formula advancements for challenging conditions alongside environmental regulation adherence, which delivers safe, economical oil production across worldwide markets.

"North America dominated the regional market for specialty oilfield chemicals in 2024."

In 2024, North America dominated the specialty oilfield chemicals market due to vigorous upstream activities in the Permian, Bakken, and Eagle Ford shale formations. The region utilizes advanced drilling techniques alongside widespread enhanced oil recovery (EOR) practices and robust rules that encourage environmentally acceptable chemical treatments. Increased demand for high-performance chemicals-such as corrosion inhibitors, scale inhibitors, and demulsifiers-has been fueled by growing production from unconventional reserves. Additionally, ongoing investments in deepwater and tight oil projects, combined with a focus on improving operational efficiency and environmental compliance, have solidified North America's leadership in the global specialty oilfield chemicals market.

By Company Type: Tier 1: 25%, Tier 2: 42%, and Tier 3: 33%

By Designation: C-level Executives: 20%, Directors: 30%, and Other Designations: 50%

By Region: North America: 20%, Europe: 10%, Asia Pacific: 40%, South America: 10%, and the Middle East & Africa: 20%

Companies Covered: BASF (Germany), Clariant (Switzerland), Dow (US), Syensqo (Belgium), SLB (US), Halliburton (US), Baker Hughes Company (US), Arkema (France), Cargill, Incorporated (US), and Chevron Phillips Chemical Company LLC (US) are covered in the report.

The study includes an in-depth competitive analysis of these key players in the specialty oilfield chemicals market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the specialty oilfield chemicals market based on type (demulsifiers, inhibitors & scavengers, rheology modifiers, friction reducers, specialty biocides, specialty surfactants, pour point depressants, and other types), reservoir type (onshore reservoirs and offshore reservoirs), application (production, well stimulation, drilling fluids, enhanced oil recovery, cementing, and workover & completion), and region (Asia Pacific, North America, Europe, South America, and Middle East & Africa). The report's scope covers detailed information regarding drivers, restraints, challenges, and opportunities influencing the growth of the specialty oilfield chemicals market. A detailed analysis of the key industry players has been done to provide insights into their business overview, products offered, and key strategies, such as partnerships, collaborations, mergers, acquisitions, product launches, and expansions, associated with the specialty oilfield chemicals market. This report covers a competitive analysis of upcoming startups in the specialty oilfield chemicals market ecosystem.

Reasons to Buy the Report

The report will offer the market leaders/new entrants with information on the closest approximations of the revenue numbers for the overall specialty oilfield chemicals market and the subsegments. This report will help stakeholders understand the competitive landscape, gain more insights into positioning their businesses better, and plan suitable go-to-market strategies. The report will help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following points:

Analysis of key drivers (rising global crude oil production, expansion of enhanced oil recovery (EOR) techniques, and technological progress in oilfield operations), restraints (fluctuating crude oil prices and global supply chain disruptions), opportunities (rising oilfield explorations in emerging regions and growing aging oil reservoirs), and challenges (stringent environmental regulations and sustainability pressures and operational complexity in extreme environments limits chemical performance).

Product Development/Innovation: Detailed insights into upcoming technologies, research & development activities, and product & service launches in the specialty oilfield chemicals market.

Market Development: Comprehensive information about profitable markets - the report analyzes the specialty oilfield chemicals market across varied regions.

Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the specialty oilfield chemicals market.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players such as BASF (Germany), Clariant (Switzerland), Dow (US), Syensqo (Belgium), SLB (US), Halliburton (US), Baker Hughes Company (US), Arkema (France), Cargill, Incorporated (US), and Chevron Phillips Chemical Company LLC (US), among others.

TABLE OF CONTENTS

1 INTRODUCTION

1.1 STUDY OBJECTIVES

1.2 MARKET DEFINITION

1.3 STUDY SCOPE

1.3.1 MARKETS COVERED AND REGIONAL SCOPE

1.3.2 INCLUSIONS AND EXCLUSIONS

1.3.3 YEARS CONSIDERED

1.3.4 CURRENCY CONSIDERED

1.3.5 UNITS CONSIDERED

1.4 LIMITATIONS

1.5 STAKEHOLDERS

1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

2.1 RESEARCH DATA

2.1.1 SECONDARY DATA

2.1.1.1 Key data from secondary sources

2.1.2 PRIMARY DATA

2.1.2.1 Key data from primary sources

2.1.2.2 Key industry insights

2.2 MARKET SIZE ESTIMATION

2.3 BASE NUMBER CALCULATION

2.3.1 DEMAND-SIDE APPROACH

2.3.2 SUPPLY-SIDE APPROACH

2.4 MARKET FORECAST APPROACH

2.4.1 SUPPLY SIDE

2.4.2 DEMAND SIDE

2.5 DATA TRIANGULATION

2.6 FACTOR ANALYSIS

2.7 RESEARCH ASSUMPTIONS

2.8 RESEARCH LIMITATIONS AND RISK ASSESSMENT

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN SPECIALTY OILFIELD CHEMICALS MARKET

4.2 NORTH AMERICA: SPECIALTY OILFIELD CHEMICALS MARKET, BY APPLICATION AND COUNTRY

4.3 SPECIALTY OILFIELD CHEMICALS MARKET, BY TYPE

4.4 SPECIALTY OILFIELD CHEMICALS MARKET, BY APPLICATION

4.5 SPECIALTY OILFIELD CHEMICALS MARKET, BY COUNTRY

5 MARKET OVERVIEW

5.1 INTRODUCTION

5.2 MARKET DYNAMICS

5.2.1 DRIVERS

5.2.1.1 Rising global crude oil production

5.2.1.2 Expansion of Enhanced Oil Recovery (EOR) techniques

5.2.1.3 Increasing sophistication of exploration and production technologies

5.2.2 RESTRAINTS

5.2.2.1 Fluctuating crude oil prices

5.2.2.2 Global supply chain disruptions

5.2.3 OPPORTUNITIES

5.2.3.1 Rising oilfield exploration in emerging regions

5.2.3.2 Growing aging oil reservoirs

5.2.4 CHALLENGES

5.2.4.1 Stringent environmental regulations and sustainability pressures

5.2.4.2 Operational complexities in extreme environments limit chemical performance

5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.3.1 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

5.4 ECOSYSTEM ANALYSIS

5.5 VALUE CHAIN ANALYSIS

5.6 TARIFF AND REGULATORY LANDSCAPE

5.6.1 TARIFF ANALYSIS (HS CODE: 381190)

5.6.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

5.6.3 KEY REGULATIONS

5.6.3.1 ISO 10414-1 / API RP 13B-1

5.6.3.2 OSPAR Decision 2000/2 & HOCNF

5.6.3.3 API RP 55 - Recommended Practices for Oilfield H2S Safety