전기자동차용 고체 배터리 시장 : 시장 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Solid-State Battery for Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1885808

리서치사:Global Market Insights Inc.

발행일:2025년 11월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

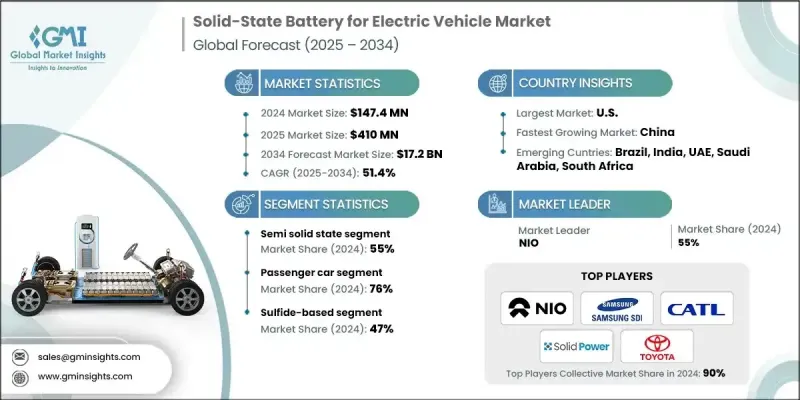

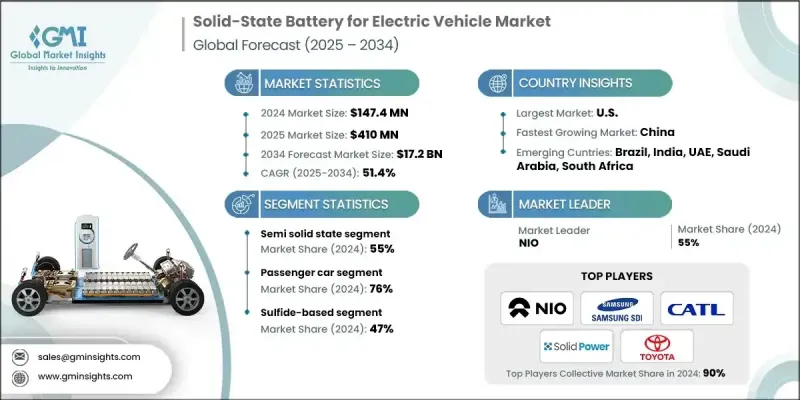

세계의 전기자동차용 고체 배터리 시장은 2024년 1억 4,740만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 51.4%로 성장할 전망이며, 172억 달러에 이를 것으로 예측됩니다.

기존의 액체 전해질 리튬 이온 배터리에서의 열폭주 및 화재 위험, 고유 한계에 대한 우려로 자동차 제조업체는 보다 안전하고 안정적인 배터리 화학 연구를 진행하고 있습니다. 고체 배터리는 가연성 전해질을 제거하고 우수한 열 안정성을 제공하며 극단적인 온도 하에서도 신뢰성 높은 성능을 발휘합니다. 정부에 의한 배터리 안전 규제의 강화와 제조업체의 리스크 경감에 대한 주력에 따라, 견고하고 충돌 내성이 있는 배터리 팩에 대한 수요가 급증하고 있습니다. 자동차 제조업체는 차량의 무게 증가 없이 항속 거리를 연장하기 위해 첨단 배터리 기술에 많은 투자를 하고 있습니다. 고체 배터리는 더 높은 에너지 밀도, 더 얇은 셀 구조, 더 빠른 충전 속도를 제공하여 파일럿 생산 라인과 전략적 공급 파트너십을 추진하고 있습니다. 가볍고 장거리 주행이 가능한 전기자동차(EV)로의 움직임이 상업화를 가속화하는 한편, 미국, 유럽, 중국, 일본, 한국의 각국 정부는 연구개발 및 생산에 수십억 달러를 투자해 스타트업 기업과 기존 제조업체의 리스크를 경감하는 인센티브를 제공합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 시 가치

1억 4,740만 달러

예측 금액

172억 달러

CAGR

51.4%

반고체 배터리 부문은 2024년에 55%의 점유율을 차지했으며, 2025-2034년 CAGR 50%로 성장할 것으로 예측됩니다. 반고체 배터리는 전통적인 액체 전해질 리튬 이온 배터리와 완전 고체 설계의 중간 위치에 있으며, 안전성 및 에너지 밀도를 향상시키면서 현재 제조 인프라와의 호환성을 유지합니다. 이 접근법을 통해 생산 비용을 줄이고 개발 기간을 단축할 수 있어 자동차 제조업체는 차세대 배터리 성능을 신속하게 도입할 수 있으므로 중급 및 고급 전기자동차(EV)에서의 채택이 가속화됩니다.

승용차 부문은 2024년에 76%의 점유율을 차지했으며, 2025-2034년 연평균 복합 성장률(CAGR) 51%로 성장할 것으로 예측됩니다. 고객은 EV에 빈번한 충전이 필요없는 장거리 주행 성능을 점점 기대하고 있습니다. 고체 배터리는 1회의 충전으로 700-1,000km를 넘는 항속 거리를 실현해, 항속 거리에 대한 불안을 경감합니다. 이를 통해 이러한 첨단 배터리 시스템을 탑재한 콤팩트, 중형, 프리미엄 EV의 소비자에 의한 채용을 촉진합니다.

미국의 전기자동차용 고체 배터리 시장은 2024년 4,970만 달러의 매출을 기록해 86%의 점유율을 차지했습니다. IRA(인플레이션 억제법)와 ARPA-E(선진 연구 프로젝트 청 에너지 부문) 등의 정부 시책이 전기자동차의 보급 및 배터리 기술 혁신에 대한 투자를 촉진하여 고체 배터리의 대규모 연구 개발 및 제조를 지원하고 있습니다. 이러한 프로그램을 통해 보다 안전하고 고성능 EV 배터리 기술로 신속하게 전환할 수 있습니다.

목차

제1장 조사 방법

시장 범위 및 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역별 및 국가별

기본 추정치 및 계산

기준 연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측 모델

조사의 전제조건 및 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

고에너지 밀도 고체 전해질에서의 획기적인 진전

보다 안전한 EV 배터리 기술에 대한 세계 수요 증가

파일럿 라인에 대한 OEM 및 정부에 의한 다액의 투자

초급속 충전 기능을 갖춘 장거리 EV로의 이행

전략적 제휴 및 소재의 혁신

업계의 잠재적 위험 및 과제

높은 제조 비용 및 복잡한 가공 공정

기가팩토리의 확장성 및 수율 문제

공급망의 성숙도가 한정적

급속 충전 시의 내구성에 관한 과제

시장 기회

세계의 전기자동차 보급률 확대

리튬 금속 및 실리콘 음극 설계의 진전

프리미엄 및 고성능 EV의 상업화

재활용 및 순환형 경제로의 길

시장의 과제

기술 검증 및 실지 시험의 요건

경쟁하는 차세대 기술

OEM의 위험 회피 자세 및 보수적인 도입 스케줄

표준화 및 상호 운용성의 과제

SSB 제조에 있어서 숙련 노동력의 부족

성장 가능성 분석

주요 시장 동향 및 변화 요인

장래 시장 동향

규제 상황

Porter's Five Forces 분석

PESTEL 분석

기술 및 혁신 동향

현행 기술

선진적인 양극 및 음극 재료

열 제어를 위한 열 관리 시스템

고에너지 밀도 전지

확장 가능한 제조 공정

신흥 기술

AI를 활용한 전지 설계 및 제조

자기 형성 양극 기술

듀얼 파워 및 멀티 케미스트리 아키텍처

디지털 트윈 및 스마트 제조

특허 분석

생산 통계

생산 거점

소비 거점

수출과 수입

가격 동향

지역별

추진력별

가격 분석 및 밸류체인 경제성

소재 부문별 SSB 가격 동향

비용 구조의 내역

지역별 가격 감응도

비용 내역 분석

재료비

제조 및 가공 비용

품질 관리 및 시험 비용

포장 및 운송 비용

지속가능성 및 환경면

지속가능한 실천

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

국제무역 및 수출입 분석

지역별 수입 의존도

무역 규제 및 관세의 영향

제품 수명주기 분석

예상되는 사이클 수명

캘린더 수명 및 열화 패턴

경시적인 성능 유지

수명 종료 시의 성능 임계치

업계의 중요한 과제 및 기업의 대응 전략

기술적 갭

제조 및 스케이러빌리티의 갭

공급망의 갭

표준화 및 상호 운용성의 갭

시장 도입에 있어서의 갭

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획 및 자금 조달

제5장 시장 추계 및 예측 : 재료별(2021-2034년)

주요 동향

폴리머베이스

황화물계

산화물계

기타

제6장 시장 추계 및 예측 : 추진력별(2021-2034년)

주요 동향

BEV(배터리식 전기자동차)

PHEV

HEV

제7장 시장 추계 및 예측 : 용도 단계별(2021-2034년)

주요 동향

시작 및 연구개발

파일럿 규모로의 도입

상업 생산

제8장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

반고체 상태

고체

제9장 시장 추계 및 예측 : 차량별(2021-2034년)

주요 동향

승용차

해치백

세단

SUV

상용차

소형차

중형차

대형 차량

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

러시아

북유럽 국가

아시아태평양

중국

인도

일본

한국

ANZ

싱가포르

베트남

태국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계 기업

BYD Company Limited

CATL

Factorial Energy

Ganfeng Lithium

General Motors

Ilika plc

LG Energy

Panasonic Corporation

PolyPlus Battery Company

QuantumScape Corporation

SAFT

Samsung SDI

SK Innovation

Solid Power

Toyota Motor Corporation

Volkswagen Group

지역 기업

Blue Solutions

CALB

EVE Energy

Farasis Energy

Gotion High-Tech

Hyundai Motor Group

Narada Power Source

Nissan Motor

ProLogium Technology

Sakuu Corporation

Sunwoda Electronic

Svolt Energy Technology

WeLion New Energy Technology

신흥 기업

Factorial Energy

Ilika plc

InoBat

PolyPlus Battery Company

Sakuu Corporation

WeLion New Energy Technology

AJY

영문 목차

영문목차

The Global Solid-State Battery for Electric Vehicle Market was valued at USD 147.4 million in 2024 and is estimated to grow at a CAGR of 51.4% to reach USD 17.2 billion by 2034.

Concerns over thermal runaway, fire hazards, and the inherent limitations of conventional liquid-electrolyte lithium-ion batteries are pushing automakers to explore safer, more stable battery chemistries. Solid-state batteries eliminate flammable electrolytes, offer superior thermal stability, and perform reliably under extreme temperatures. With governments tightening battery safety regulations and manufacturers focusing on risk mitigation, the demand for robust, crash-resistant battery packs is surging. Automakers are investing heavily in advanced battery technologies to extend driving range without adding extra weight to vehicles. Solid-state batteries provide higher energy density, thinner cell structures, and faster charging, driving pilot production lines and strategic supply partnerships. The push toward lightweight, long-range EVs is accelerating commercialization, while governments in the US, Europe, China, Japan, and South Korea are investing billions in research, development, and production, providing incentives that reduce risks for startups and established manufacturers.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$147.4 Million

Forecast Value

$17.2 Billion

CAGR

51.4%

The semi-solid-state segment held a 55% share in 2024 and is projected to grow at a 50% CAGR from 2025 to 2034. Semi-solid-state batteries bridge conventional liquid-electrolyte lithium-ion cells with fully solid-state designs, enhancing safety and energy density while remaining compatible with current manufacturing infrastructure. This approach reduces production costs, shortens timelines, and allows automakers to introduce next-generation battery performance faster, accelerating adoption in mid-range and premium EVs.

The passenger cars segment held a 76% share in 2024 and is expected to grow at a CAGR of 51% from 2025 to 2034. Customers increasingly expect EVs to deliver extended ranges without frequent charging. Solid-state batteries enable ranges exceeding 700 to 1,000 km per charge, alleviating range anxiety and boosting consumer adoption of compact, mid-size, and premium EVs equipped with these advanced battery systems.

US Solid-State Battery for Electric Vehicle Market held an 86% share, generating USD 49.7 million in 2024. Government initiatives like the IRA and ARPA-E are driving investment in electric vehicle adoption and battery innovation, supporting large-scale research, development, and manufacturing of solid-state batteries. These programs are enabling a swift transition to safer, higher-performance EV battery technologies.

Key players in the Solid-State Battery for Electric Vehicle Market include NIO, LG Energy Solution, Solid Power, BYD, CATL, Toyota, Gotion High-Tech, Enovix, Samsung SDI, and Nissan. Companies in the Solid-State Battery for Electric Vehicle Market are strengthening their position by investing in advanced R&D to enhance energy density, durability, and safety. They are forming strategic collaborations with automakers and material suppliers, establishing pilot production lines, and scaling manufacturing capacity to meet growing demand. Geographic expansion, securing critical raw materials, and leveraging government incentives are also central strategies. Additionally, firms focus on improving battery performance through innovative designs, faster charging solutions, and compact architectures to solidify their competitive advantage in the rapidly evolving EV battery landscape.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Material

2.2.3 Propulsion

2.2.4 Vehicle

2.2.5 Application Stage

2.2.6 Technology

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook

2.6 Strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Breakthroughs in high-energy-density solid electrolytes

3.2.1.2 Rising global demand for safer EV battery technologies

3.2.1.3 Heavy OEM & government investments in pilot lines

3.2.1.4 Shift toward long-range EVs with ultra-fast charging

3.2.1.5 Strategic partnerships & material innovations

3.2.2 Industry pitfalls and challenges

3.2.2.1 High manufacturing costs & complex processing

3.2.2.2 Scalability & yield issues in gigafactories

3.2.2.3 Limited supply chain maturity

3.2.2.4 Durability issues during fast charging

3.2.3 Market opportunities

3.2.3.1 Growing global EV penetration

3.2.3.2 Advances in lithium-metal & silicon-anode design

3.2.3.3 Premium & performance EV commercialization

3.2.3.4 Recycling & circular economy pathways

3.2.4 Market Challenges

3.2.4.1 Technology validation & field testing requirements