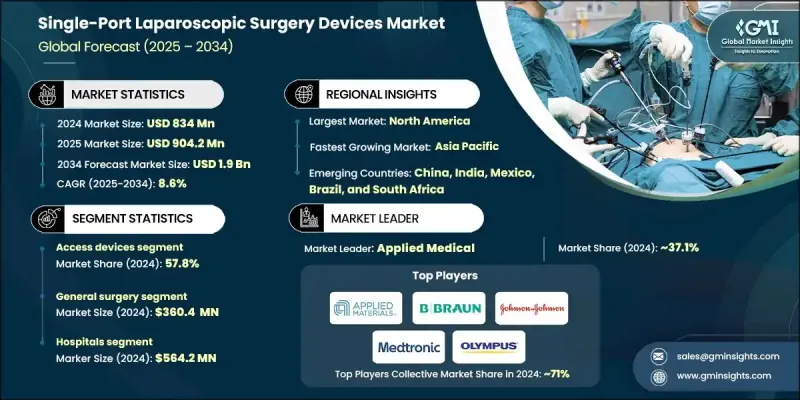

세계의 단일공 복강경 수술 기기 시장은 2024년에 8억 3,400만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 8.6%로 성장하여 19억 달러에 이를 것으로 예측됩니다.

시장 성장은 비만, 대장질환, 부인과질환의 발생률 상승에 더하여, 저침습 수술법에 대한 환자의 선호 증가, 외래 수술 건수 증가에 의해 견인되고 있습니다. 단일공 복강경 수술 기기는 낮은 침습 기술의 큰 진보이며, 외과의 사는 일반적으로 탯줄 근처의 작은 절개를 통해 복잡한 수술을 가능하게합니다. 이것은 흉터 형성, 조직 손상 및 회복 기간을 크게 줄일 수 있습니다. 이러한 장치는 통증 완화, 입원 기간 단축, 회복 가속화, 미용 결과 향상을 추구하는 의료 종사자와 환자들 사이에서 빠르게 확산되고 있습니다. 기존의 개복 수술에 비해 단일공 복강경 수술은 절개부가 작기 때문에 합병증이 적고 감염 위험도 감소합니다. 외과기술의 지속적인 진화와 단일공 플랫폼의 인체공학적 개선에 의해 정밀도, 조작성, 수술 효율이 계속 향상되고 있어, 세계의 병원이나 외래수술센터(ASC)에서 강한 수요를 낳고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 시작 금액 | 8억 3,400만 달러 |

| 예측 금액 | 19억 달러 |

| CAGR | 8.6% |

복강경 수술 기구 부문은 2024년에 42.2%의 점유율을 차지했습니다. 그 성장은 주로 단일 절개부를 통한 복잡한 움직임, 특히 해부학적으로 제한된 수술 영역을 지원하는 전문 정밀기구의 필요성에 의해 견인됩니다. 트로칼, 가위, 박리기, 겸자, 바늘 홀더 등의 기구는 수술 중 정밀한 제어와 용이성을 보장하는 데 중요한 역할을 합니다. 이 장비는 단일 포트 기술로 일반적인 장비 혼잡 및 삼각 측량 제한과 같은 일반적인 문제를 외과 의사가 극복하는 데 도움이 됩니다. 인체공학에 근거한 관절식 기구 설계의 진보는 수술의 성능을 더욱 향상시키고 이 부문의 확대를 추진하고 있습니다.

일반 수술 분야는 2024년 3억 6,040만 달러 시장 규모를 창출했습니다. 그 이점은 맹장 절제술, 탈장 수술, 담낭 절제술 등 단일 포트 접근에 적합한 수술 수가 많기 때문입니다. 입원시설과 외래시설 모두에서 단일포트법이 널리 받아들여지면서 이 분야는 계속 혜택을 받고 있습니다. 환자와 의료 제공업체는 회복 기간의 단축, 흉터의 경감, 전체적인 임상 결과의 개선 등의 이점으로부터 SPLS를 선택하는 경향이 강해지고 있습니다. 일반 수술 수술 증가와 수술 접근 시스템의 지속적인 발전이 함께 이 분야의 SPLS 장치에 대한 강한 수요를 더욱 강화하고 있습니다.

미국의 단일공 복강경 수술 기기 시장은 2024년 3억 5,790만 달러의 규모에 도달했습니다. 미국은 유리한 상환 정책, 첨단 기술을 갖춘 외과 의료 종사자의 존재, 의료 혁신에 대한 지속적인 투자에 힘입어 고급 싱글 포트 복강경 시스템의 도입에 세계를 선도하고 있습니다. 이 지역에서는 수술 훈련에 대한 강력한 지원, 디지털 수술 플랫폼 개발, 시뮬레이션 기반 학습 통합 등의 이점을 누리고 있으며, 이들 모두는 다양한 전문 분야에서 SPLS 기술의 광범위한 도입을 추진하고 있습니다.

세계의 단일공 복강경 수술 기기 시장에서 활약하는 주요 기업으로는 존슨 엔드 존슨, 어플라이드 메디컬, B. 브라운, 올림푸스, 메드트로닉, 슈트르츠, 유니맥스, 칸지, 시텍, 룩메드, GYTR-VII, 호스피인스 등이 있습니다. 단일공 복강경 수술 기기 업계의 지위를 강화하기 위해 주요 기업은 제품 혁신, 파트너십 및 전략적 인수에 주력하여 세계 사업 확대를 도모하고 있습니다. 많은 기업들이 외과 의사의 편안함과 효율성을 높이는 고급 액세스 포트, 멀티 악기 플랫폼 및 유연한 복강경 도구를 설계하기 위해 연구 개발에 많은 투자를 하고 있습니다. 또한 유통 네트워크의 강화와 병원과의 제휴를 통해 임상 도입을 가속화하고 있습니다. 또한 제조 공정의 최적화와 현지 생산에 의한 비용 절감을 추진함과 동시에 외과의의 숙련도 향상과 지역을 넘어 지속적인 시장 성장을 확보하기 위해 교육 프로그램의 확충에도 주력하고 있습니다.

The Global Single-Port Laparoscopic Surgery Devices Market was valued at USD 834 million in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 1.9 Billion by 2034.

Market growth is driven by the rising incidence of obesity, colorectal disorders, and gynecological diseases, combined with the growing patient preference for minimally invasive surgical approaches and the increasing number of outpatient procedures. Single-port laparoscopic surgery (SPLS) devices mark a major step forward in minimally invasive techniques, allowing surgeons to perform complex operations through one small incision, typically near the umbilicus, which significantly reduces scarring, tissue trauma, and recovery time. These devices have gained rapid adoption among healthcare professionals and patients seeking procedures with reduced pain, shorter hospital stays, quicker recovery, and better cosmetic results. Compared with traditional open surgeries, single-port laparoscopy offers fewer complications and a lower infection risk due to smaller incisions. The ongoing evolution of surgical technology and ergonomic improvements in single-port platforms continue to enhance precision, control, and procedural efficiency, fueling strong demand in hospitals and ambulatory centers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $834 Million |

| Forecast Value | $1.9 Billion |

| CAGR | 8.6% |

The laparoscopic instruments segment held a 42.2% share in 2024. Its growth is primarily driven by the need for specialized precision tools that support intricate movements through a single incision, particularly in anatomically restricted surgical areas. Instruments such as trocars, scissors, dissectors, graspers, and needle holders play a critical role in ensuring precise control and dexterity during procedures. These devices help surgeons overcome common challenges associated with instrument crowding and limited triangulation, which are typical in single-port techniques. The advancement of ergonomic and articulating instrument designs is further improving surgical performance and driving the segment's expansion.

The general surgery segment generated USD 360.4 million in 2024. Its dominance stems from the high number of procedures suitable for single-port access, including appendectomy, hernia repair, and cholecystectomy. The segment continues to benefit from growing acceptance of single-port methods across both inpatient and outpatient facilities. Patients and providers are increasingly opting for SPLS due to its shorter recovery times, reduced scarring, and better overall clinical outcomes. The rising number of general surgical cases and continuous advancements in surgical access systems further reinforce the strong demand for SPLS devices in this segment.

U.S. Single-Port Laparoscopic Surgery Devices Market generated USD 357.9 million in 2024. The U.S. leads globally in adopting advanced single-port laparoscopic systems, driven by favorable reimbursement policies, the presence of a highly skilled surgical workforce, and consistent investments in healthcare innovation. The region benefits from strong support for surgical training, development of digital surgical platforms, and the integration of simulation-based learning, all of which are propelling the widespread implementation of SPLS technologies across different specialties.

Prominent companies active in the Global Single-Port Laparoscopic Surgery Devices Market include Johnson & Johnson, Applied Medical, B. Braun, Olympus, Medtronic, STORZ, UNIMAX, KANGJI, CITEC, LOOKMED, GYTR-VII, and Hospiinz. To reinforce their position in the single-port laparoscopic surgery devices industry, leading companies are focusing on product innovation, partnerships, and strategic acquisitions to expand their global reach. Many are investing heavily in research and development to design advanced access ports, multi-instrument platforms, and flexible laparoscopic tools that enhance surgeon comfort and efficiency. Firms are also strengthening distribution networks and entering collaborations with hospitals to accelerate clinical adoption. Additionally, they are emphasizing affordability through manufacturing optimization and local production, while expanding their training programs to increase surgeon proficiency and ensure consistent market growth across regions.