5G 텔레매틱스 제어 장치(TCU) 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

5G Telematics Control Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871137

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

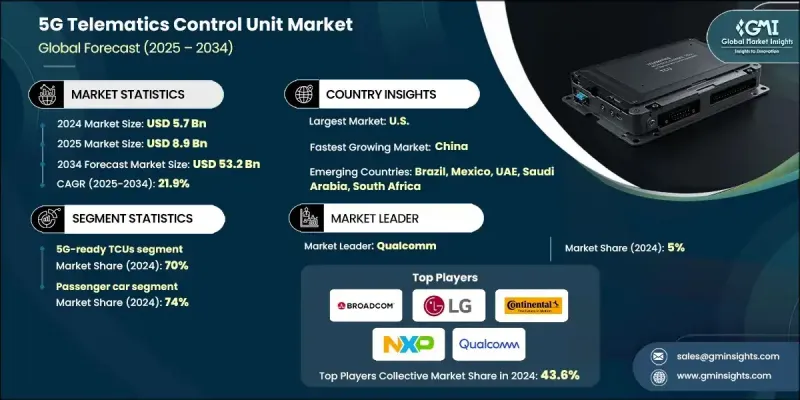

전 세계 5G 텔레매틱스 제어 장치 시장은 2024년 57억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 21.9%를 나타낼 것으로 예측되며 532억 달러에 달할 전망입니다.

자동차 제조업체들은 고속 연결성, 실시간 데이터 처리 및 원활한 시스템 통합에 대한 수요 증가를 충족하기 위해 생산 과정에서 5G TCU를 차량에 직접 통합하는 경우가 점점 더 많아지고 있습니다. 자동차 산업이 커넥티드 및 자율주행 모빌리티로 전환됨에 따라, 내장형 텔레매틱스 장치는 우수한 성능과 신뢰성으로 인해 개조 솔루션보다 선호되고 있습니다. 이러한 장치는 차량 내 인포테인먼트, 클라우드 통신, 스마트 내비게이션, 원격 진단, 예측 유지보수 등 현대적 기능을 구현하는 데 핵심적인 역할을 하며, 모두 최소한의 지연 시간으로 빠른 데이터 전송이 필요합니다. 전기차(EV) 보급이 가속화됨에 따라 5G TCU는 에너지 효율 향상과 전반적인 주행 경험 개선에 필수적입니다. 5G 연결성과 결합된 엣지 컴퓨팅은 실시간 데이터 분석을 가능하게 하여 안전이 중요한 차량 운영에 대한 신속한 의사 결정을 지원합니다. 인공지능(AI), 텔레매틱스, 다중 센서 데이터 처리의 시너지도 5G TCU 채택을 촉진하여 자동차 생태계 전반에 걸쳐 첨단 반도체 수요를 주도하고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 금액

57억 달러

예측 금액

532억 달러

CAGR

21.9%

승용차 부문은 74%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 22%의 성장률을 보일 것으로 예상됩니다. 커넥티드 카에 대한 선호도 증가로 자동차 제조사들은 외부 인프라, 클라우드 플랫폼 및 다른 차량과의 실시간 통신을 지원하는 TCU를 탑재하고 있습니다. 이 장치들은 내비게이션부터 엔터테인먼트까지 모든 것을 제어하며, 실시간 데이터 스트림을 관리하여 안전성과 기능성을 향상시킵니다. 지능형 모빌리티 경험에 대한 소비자 수요 증가로 OEM들은 원활한 연결성을 보장하기 위해 고성능 5G TCU를 차량에 통합해야 하는 압박을 지속적으로 받고 있습니다.

자동차 제조사들은 초저지연 및 고속 데이터 전송을 가능케 하여 고급 인포테인먼트 및 AI 기반 기능을 원활하게 구동하기 위해 신차 모델에 5G TCU를 탑재할 계획을 적극 추진 중입니다. 이러한 장치는 실시간 진단 및 예측 정비를 지원하여 더 스마트한 차량 생태계를 조성합니다. OEM들은 5G TCU를 조기에 도입함으로써 경쟁 우위를 확보하고, 미래 커넥티드 교통 부문에서 입지를 강화하고자 합니다. 자율주행 및 반자율주행 기술 발전 역시 5G 텔레매틱스 시스템에 대한 투자 확대를 촉진하고 있습니다. 이 장치들은 차량이 센서 입력을 신속히 처리하고, 다른 시스템(V2X)과 통신하며, 실시간 결정을 내릴 수 있게 하여 안전한 자동 주행을 위한 핵심 요소를 제공합니다.

중국의 5G 텔레매틱스 제어 장치 시장은 2024년에 40%의 점유율을 차지했으며 10억 달러 규모에 이르렀습니다. 실시간 내비게이션, 진단, 인포테인먼트 등 스마트 차량 시스템에 대한 소비자 수요가 주된 동력이 되어 연결 차량 보급이 급증하고 있습니다. 연결 기능을 탑재한 차량이 증가함에 따라 OEM 업체들은 데이터 집약적 애플리케이션을 효율적으로 관리하기 위해 고급 TCU 도입을 확대하고 있습니다. 안전 규정 및 지능형 교통 정책을 통한 정부의 지원이 성장을 가속화하고 있으며, 긴급 대응, 위치 추적, 규정 준수를 지원하는 프레임워크가 TCU 보급을 촉진하고 있습니다. 스마트 인프라 및 자동차 디지털화를 촉진하는 전략적 프로그램은 중국을 차량 연결성 혁신의 최전선에 위치시켰습니다.

5G 텔레매틱스 제어 장치 시장을 주도하는 주요 기업으로는 르네사스 일렉트로닉스, 인피니언 테크놀로지스, 엔엑스피, 에스티마이크로일렉트로닉스, 텍사스 인스트루먼트, 애널로그 디바이스, 도시바 일렉트로닉 디바이스 등이 있습니다. 업계 리더들은 5G 텔레매틱스 제어 장치 시장에서의 입지를 공고히 하기 위해 칩셋 통합 강화, 자동차 등급 반도체 포트폴리오 확장, OEM 및 1차 공급업체와의 협력적 파트너십 구축에 주력하고 있습니다. 기업들은 엄격한 자동차 규격을 충족하기 위해 저전력 설계, 빠른 데이터 처리량, 신뢰성을 최우선 과제로 삼고 있습니다. 연구개발(R&D)에 대한 전략적 투자는 엣지 컴퓨팅, AI 가속화, 안전한 무선 업데이트(OTA) 부문의 혁신을 촉진하고 있습니다. 진화하는 V2X(차량-사물 간 통신) 표준과 자율주행 수요에 부응함으로써, 이들 기업은 소프트웨어 정의 및 커넥티드 차량으로의 전환을 활용하는 동시에 자사 솔루션의 미래 대비를 강화하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝의 출처

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측 모델

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

커넥티드 차량 안전 시스템에 대한 정부 의무화

5G 네트워크 인프라의 전개 가속

자율주행차 개발 및 테스트 요구사항

차량 관리 효율성 및 비용 최적화 수요

첨단 인포테인먼트 및 연결성에 대한 소비자 수요

업계의 잠재적 억제요인 및 과제

높은 구현 비용 및 투자 수익률(RoI) 불확실성

주파수 할당 및 간섭 문제

사이버 보안 취약점과 프라이버시에 대한 우려

지역별 표준화 분열

레거시 시스템 통합 복잡성

시장 기회

초저지연 애플리케이션을 위한 엣지 컴퓨팅 통합

국경 간 V2X 통신 표준화

기존 차량용 애프터마켓 개조 솔루션

스마트 시티 인프라를 위한 공공-민간 파트너십

개발도상국에서의 신흥 시장 진출

성장 가능성 분석

주요 시장 동향과 파괴적 변화

장래 시장 동향

규제 상황

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 동향

현재의 기술 동향

5G NR 기술규격과 사양

C-V2X 통신 프로토콜

엣지 컴퓨팅 통합

AI 및 머신러닝의 응용

신흥기술

6G 연구개발 이니셔티브

양자 통신 기술

첨단 안테나 기술

차량 시스템용 디지털 트윈 통합

특허 분석

가격 분석

OEM 가격 전략

애프터마켓 가격 모델

구독형 서비스의 가격 설정

수량 기준 가격대

코스트 내역 분석

하드웨어 부품 비용

소프트웨어 및 라이선싱 비용

통합 및 설치 비용

보수 및 지원 비용

지속가능성과 환경면

지속가능한 대처

폐기물 감축 전략

생산에 있어서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

투자환경분석

반도체 R&D 투자

자동차 오디오 기술에 대한 자금 조달

오디오 부문의 벤처 캐피탈 투자

기업 투자 패턴

정부조사자금

오디오 반도체 부문의 M&A 동향

고객 행동과 시장 보급 분석

고객 세분화 및 프로파일링

채용 패턴과 의사 결정 요인

구매 행동 분석

기술 선호의 동향

지역별 고객 행동의 차이

고객 만족도와 충성도 분석

도입 장벽과 시장 저항

고객교육과 인지도 수준

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

제휴 및 협업

신제품 발매

사업 확대 계획과 자금 조달

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

주요 동향

5G TCU

네이티브 5G TCU

제6장 시장 추계 및 예측 : 추진력별(2021-2034년)

주요 동향

가솔린

디젤

완전 전기

HEV

PHEV

연료전지자동차(FCEV)

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

서브 6GHz 5G TCU

Wave 5G TCU

제8장 시장 추계 및 예측 : 설비별(2021-2034년)

주요 동향

OEM

애프터마켓

제9장 시장 추계 및 예측 : 차량별(2021-2034년)

주요 동향

승용차

해치백

세단

SUV

상용차

소형차

중형차

대형 차량

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

러시아

북유럽 국가

아시아태평양

중국

인도

일본

한국

ANZ

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제11장 기업 프로파일

세계적 기업

Samsung Electronics

Harman International(Samsung)

LG Electronics

Qualcomm Technologies

Continental AG

Robert Bosch GmbH

Valeo

Visteon Corporation

Marelli Holdings

Huawei Technologies

지역 기업

NXP Semiconductors

Denso Corporation

Infineon Technologies

Quectel Wireless Solutions

Sierra Wireless

Ficosa International

Cavli Wireless

Rolling Wireless

Anritsu Corporation

Panasonic Industrial

신흥 기업

aicas GmbH

CalAmp Corp

Zonar Systems

Xirgo Technologies

Telit Communications

Peiker Acustic GmbH

Novero GmbH(Laird)

Rohde & Schwarz

Jimi IoT Co., Ltd

Xiamen Yaxon Network

HBR

영문 목차

영문목차

The Global 5G Telematics Control Unit Market was valued at USD 5.7 Billion in 2024 and is estimated to grow at a CAGR of 21.9% to reach USD 53.2 Billion by 2034.

Automakers are increasingly integrating 5G TCUs directly into vehicles during production to meet rising demands for high-speed connectivity, real-time data processing, and seamless system integration. As the auto industry transitions toward connected and autonomous mobility, built-in telematics units are becoming more favorable than retrofit solutions due to their superior performance and reliability. These units play a pivotal role in enabling modern features such as in-car infotainment, cloud communication, smart navigation, remote diagnostics, and predictive maintenance, all requiring fast data transmission with minimal latency. With EV adoption accelerating, 5G-enabled TCUs are essential for enhancing energy efficiency and elevating the overall driving experience. Edge computing combined with 5G connectivity allows real-time data analysis, empowering faster decision-making for safety-critical vehicle operations. The synergy of AI, telematics, and multi-sensor data processing has also fueled the adoption of 5G TCUs, driving the need for advanced semiconductors across the automotive ecosystem.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$5.7 Billion

Forecast Value

$53.2 Billion

CAGR

21.9%

The passenger vehicles segment held a 74% share and is expected to grow at a CAGR of 22% between 2025 and 2034. The growing preference for connected cars is motivating vehicle manufacturers to embed TCUs that support real-time communication with external infrastructure, cloud platforms, and other vehicles. These units control everything from navigation to entertainment, and they enhance safety and functionality by managing live data streams. Rising consumer demand for intelligent mobility experiences continues to pressure OEMs to integrate high-performance 5G TCUs into their vehicles to ensure seamless connectivity.

The automakers are actively planning to install 5G-compatible TCUs into new car models to enable ultra-low latency and fast data transmission, which helps run advanced infotainment and AI-based functions smoothly. These units support real-time diagnostics and predictive maintenance, creating a smarter vehicle ecosystem. OEMs aim to gain a competitive edge by embracing 5G TCUs early, strengthening their position in the future of connected transportation. The development of autonomous and semi-autonomous driving capabilities also drives higher investments in 5G-based telematics systems. These units allow vehicles to rapidly process sensor input, communicate with other systems (V2X), and make real-time decisions, key elements for safe automated driving.

China 5G Telematics Control Unit Market held a 40% share and generated USD 1 Billion in 2024. The country is witnessing a rapid surge in connected car deployment, largely driven by consumer demand for smart in-vehicle systems like live navigation, diagnostics, and infotainment. As more vehicles integrate connected features, OEMs are stepping up the adoption of advanced TCUs to manage data-intensive applications efficiently. Government backing through safety mandates and intelligent transport policies is accelerating growth, with frameworks supporting emergency response, geolocation, and compliance pushing TCU deployment forward. Strategic programs promoting smart infrastructure and automotive digitization have further positioned China at the forefront of vehicle connectivity innovation.

Key players shaping the 5G Telematics Control Unit Market include Renesas Electronics, Infineon Technologies, NXP, STMicroelectronics, Texas Instruments, Analog Devices, and Toshiba Electronic Devices. To solidify their foothold in the 5G Telematics Control Unit Market, industry leaders are focusing on enhancing chipset integration, expanding automotive-grade semiconductor portfolios, and building collaborative partnerships with OEMs and Tier 1 suppliers. Companies are prioritizing low-power design, faster data throughput, and reliability to meet strict automotive standards. Strategic investments in R&D are fueling innovation in edge computing, AI acceleration, and secure over-the-air updates. By aligning with evolving V2X standards and autonomous driving demands, these firms are future-proofing their solutions while capitalizing on the shift toward software-defined and connected vehicles.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Vehicle

2.2.4 Propulsion

2.2.5 Technology

2.2.6 Installation

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook

2.6 Strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Government mandates for connected vehicle safety systems