차량내 결제 시스템 하드웨어 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

In-Vehicle Payment System Hardware Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871124

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

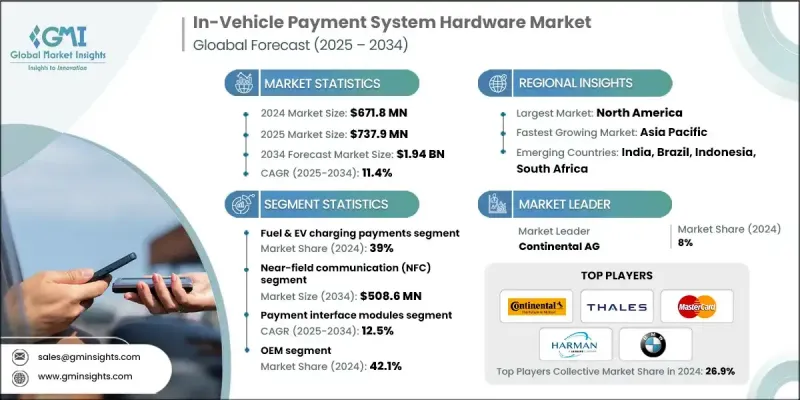

전 세계 차량내 결제 시스템 하드웨어 시장은 2024년에 6억 7,180만 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 11.4%를 나타낼 것으로 예측되며 19억 4,000만 달러에 달할 전망입니다.

전 세계적으로 커넥티드 차량 및 자율주행 차량의 확산은 통합 차량내 결제 기술의 도입을 가속화하고 있습니다. 보안 칩, 생체 인식 센서, NFC 모듈과 같은 첨단 하드웨어 구성 요소는 차량에서 직접 실시간으로 원활한 거래를 가능하게 합니다. 이러한 진화는 모빌리티 서비스 생태계 내에서 연료 충전, 주차, 통행료와 같은 서비스에 대한 자동 결제를 간소화함으로써 모빌리티 환경을 재편하고 있습니다. 특히 팬데믹 이후 소비자들의 디지털 및 비접촉 거래 선호도가 광범위하게 전환되면서 안전하고 마찰 없는 빠른 결제 경험에 대한 수요가 더욱 증가했습니다. 자동차 제조사들은 블루투스, NFC, RFID 같은 기술을 활용한 내장형 차량 결제 시스템에 대한 투자를 확대하며 대응하고 있습니다. 이러한 시스템은 인포테인먼트 플랫폼 및 디지털 지갑과 통합되어 외부 결제 네트워크와의 안전한 연동을 가능하게 합니다. 한편, 도시 및 교통 당국은 V2X 및 DSRC 기술을 활용해 통행료 징수, 주차, 충전 인프라를 현대화하고 있으며, 이는 상호 운용성과 국경 간 기능을 가능하게 하기 위해 차량내 결제 하드웨어에 의존합니다. 자동차 제조사, 핀테크 기업, 결제 제공업체 간의 파트너십은 차량내 상거래, 구독 서비스, 연결된 디지털 서비스를 통한 수익화 기회를 확대하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

6억 7,180만 달러

예측 금액

19억 4,000만 달러

CAGR

11.4%

결제 인터페이스 모듈 부문은 2025-2034년 연평균 12.5%의 성장률을 보일 것으로 예상됩니다. 인포테인먼트 시스템에 내장된 이 모듈들은 주차, 연료, 통행료 결제에 무현금 및 비접촉 거래를 가능하게 하여 토큰화된 결제 방식을 통해 편의성과 높은 보안성을 제공합니다. OEM 및 1차 공급업체들은 신뢰성, 확장성, 글로벌 안전 기준 준수를 위해 설계된 자동차 등급 인터페이스 모듈에 대규모 투자를 진행 중입니다. 이러한 통합 모듈은 다양한 차량 모델 간 결제 경험의 표준화를 돕고, 안전한 이동 중 거래에 대한 사용자 신뢰도를 높입니다.

2024년 기준, 연료 및 전기차 충전 결제 부문이 39%의 점유율을 차지했습니다. 전기차 보급 확대와 효율적인 연료/충전 솔루션 수요 증가가 차량내 결제 시스템 활용을 촉진하고 있습니다. 이러한 시스템은 운전자가 인포테인먼트 시스템에서 직접 연료 또는 전기차 충전 결제를 완료할 수 있게 하여 실물 카드나 현금에 대한 의존도를 낮춥니다. 비접촉 결제 지원 및 다양한 결제 플랫폼과의 호환성 추가로 유연성이 높아지고 사용자 상호작용이 간소화되어 소비자 편의성이 향상됩니다.

미국의 차량내 결제 시스템 하드웨어 시장은 2024년에 86.4%의 점유율을 차지했습니다. 미국 운전자들이 차량 시스템에 직접 통합된 안전하고 비접촉식이며 즉각적인 결제를 선호하는 경향이 시장 성장을 지속적으로 주도하고 있습니다. OEM 업체들은 소비자 데이터 보호 및 결제 안전성 확보를 위해 생체 인증, 내장형 지갑, PCI 준수 토큰화 등 고급 보안 기능 구현을 최우선 과제로 삼고 있습니다. 개인정보 보호 기준 및 규정 준수 요구사항에 대한 집중과 함께 자동차 제조사와 금융 네트워크 간의 협력이 이 부문에서 미국의 선도적 위상을 강화하고 있습니다.

세계의 차량내 결제 시스템 하드웨어 시장에서 사업을 전개하는 주요 기업으로는 BMW, 콘티넨탈, 다임러, Thales Group, 마스터 카드, 허먼 인터내셔널, 현대 자동차, 혼다 모터 등이 있습니다. 차량내 결제 시스템 하드웨어 시장의 주요 업체들은 경쟁적 입지를 강화하고 기술 역량을 확장하기 위한 전략적 계획을 추진 중입니다. 기업들은 원활하고 안전한 거래를 보장하기 위해 고급 인증, 암호화 및 연결 기능을 갖춘 통합 결제 모듈 개발에 주력하고 있습니다. 자동차 제조사, 핀테크 제공업체 및 결제 기술 기업 간의 전략적 협력은 혁신을 촉진하고 생태계 호환성을 확대하고 있습니다. 연구개발(R&D)에 대한 막대한 투자는 글로벌 보안 및 데이터 보호 기준에 부합하는 표준화되고 상호운용 가능한 하드웨어 솔루션의 창출을 주도하고 있습니다.

목차

제1장 조사 방법

시장 범위와 정의

조사 설계

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역별/국가별

기본 추정치와 계산

기준연도 계산

시장 추정에서의 주요 동향

1차 조사 및 검증

1차 정보

예측

조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

밸류체인 분석과 산업 구조

원재료 및 웨이퍼 제조

BMS IC 설계 및 개발

반도체 제조 및 시험

BMS 모듈 조립 및 통합

배터리 팩의 통합 및 검증

OEM 차량 통합 및 도입

애프터마켓 및 서비스 에코시스템

사용한 제품의 재활용과 지속가능성

공급자의 상황

원재료 공급자

부품 제조업체

시스템 통합자

OEM

최종 용도

업계에 미치는 영향요인

성장 촉진요인

커넥티드 및 스마트 차량의 급증

비접촉 결제에 대한 소비자 선호도 증가

전기자동차(EV)와 충전 인프라의 성장

OEM-핀테크 협력

스마트 시티와 지능형 교통 시스템 개발

업계의 잠재적 억제요인 및 과제

높은 하드웨어 및 통합 비용

사이버 보안 및 데이터 프라이버시에 대한 우려

시장 기회

MaaS(Mobility-as-a-Service)와의 통합

전기차 충전 및 친환경 모빌리티 확대

OEM과 디지털 지갑 제공업체간의 제휴

자동차에서의 생체 인증 기술의 대두

성장 가능성 분석

규제 상황

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현행 기술

신흥기술

특허 분석

가격 동향 분석

컴포넌트별

지역별

코스트 내역 분석

생산 통계

생산 거점

소비 거점

수출입

지속가능성과 환경면

지속가능한 실천

폐기물 감축 전략

생산에서의 에너지 효율

환경에 배려한 대처

탄소발자국에 관한 고려 사항

시장의 성숙도와 보급 상황의 분석

기술 성숙도 레벨 평가

지역별 도입 성숙도 비교

응용 부문의 성숙도 분석

제조 준비도와 규모 평가

상용 전개의 타임라인

장래의 동향

주요 시장 동향과 변화

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 뉴스와 대처

합병 및 인수

제휴 및 협업

신제품 발매

확대계획과 자금조달

제5장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

주요 동향

결제 인터페이스 모듈

생체 인증 장치

디스플레이 및 인포테인먼트 유닛

연결 컴포넌트

센서 및 컨트롤러

임베디드 보안 하드웨어

제6장 시장 추계 및 예측 : 결제 용도별(2021-2034년)

주요 동향

연료 및 전기차 충전 결제

통행료 징수

주차 요금

드라이브스루 결제 및 소매 결제

구독 서비스 및 자동차 서비스

제7장 시장 추계 및 예측 : 기술별(2021-2034년)

주요 동향

근거리 무선 통신(NFC)

무선 주파수 식별(RFID)

전용 단거리 통신(DSRC)

셀룰러(4G/5G)

Wi-Fi/Bluetooth Low Energy

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

OEM

자동차 사업자

모빌리티 서비스 제공업체

유료 도로 및 주차장 운영 사업자

연료 및 전기자동차 인프라 제공 사업자

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

북유럽 국가

네덜란드

러시아

아시아태평양

중국

인도

일본

호주

한국

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카(MEA)

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

세계 기업

BMW AG

Continental AG

Daimler AG(Mercedes-Benz Group)

Denso Corporation

Harman International

Honda Motor Co., Ltd.

Hyundai Motor Co., Ltd.

Mastercard Incorporated

NXP Semiconductors

Qualcomm Technologies Inc.

Robert Bosch GmbH

Thales Group

지역별 기업

Aisin Corporation

Aptiv PLC

Garmin Ltd.

Hyundai Mobis

LG Electronics

Magna International Inc.

Valeo SA

ZF Friedrichshafen AG

신흥 기업 및 혁신기업

Car IQ Inc.

Cerence Inc.

IDEMIA

Ingenico(Worldline)

PayByCar Inc.

Rambus Inc.

Secure-IC

Utimaco GmbH

Verifone Systems Inc.

Xevo Inc.(Lear Corporation)

HBR

영문 목차

영문목차

The Global In-Vehicle Payment System Hardware Market was valued at USD 671.8 million in 2024 and is estimated to grow at a CAGR of 11.4% to reach USD 1.94 Billion by 2034.

The expansion of connected and autonomous vehicles worldwide is accelerating the adoption of integrated in-vehicle payment technologies. Advanced hardware components such as secure chips, biometric sensors, and NFC modules enable real-time and seamless transactions directly from vehicles. This evolution is reshaping the mobility landscape by streamlining automated payments for services such as fueling, parking, and tolls within mobility-as-a-service ecosystems. The widespread shift in consumer preferences toward digital and contactless transactions, particularly following the pandemic, has further increased demand for secure, frictionless, and fast payment experiences. Automakers are responding by increasing their investment in embedded vehicle payment systems using technologies like Bluetooth, NFC, and RFID. These systems integrate with infotainment platforms and digital wallets, allowing secure synchronization with external payment networks. Meanwhile, cities and transport authorities are modernizing tolling, parking, and charging infrastructure using V2X and DSRC technologies that depend on in-vehicle payment hardware to enable interoperability and cross-border functionality. Partnerships between automakers, fintech firms, and payment providers are expanding opportunities for monetization through in-car commerce, subscriptions, and connected digital services.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$671.8 Million

Forecast Value

$1.94 Billion

CAGR

11.4%

The payment interface module segment is expected to grow at a CAGR of 12.5% from 2025 to 2034. These modules, embedded into infotainment systems, enable cashless and contactless transactions for parking, fuel, and tolls, offering convenience and high security through tokenized payment methods. OEMs and top-tier suppliers are heavily investing in automotive-grade interface modules designed for reliability, scalability, and compliance with global safety standards. These integrated modules help standardize payment experiences across various vehicle models and enhance user confidence in secure, on-the-go transactions.

The fuel and EV charging payment segment held a 39% share in 2024. Growing adoption of electric vehicles and rising demand for efficient refueling and recharging solutions are fostering the use of in-vehicle payment systems. These systems enable drivers to complete transactions for fuel or EV charging directly from their infotainment systems, reducing reliance on physical cards or cash. The inclusion of contactless payment support and compatibility with diverse payment platforms adds flexibility and simplifies user interaction, enhancing convenience for consumers.

United States In-Vehicle Payment System Hardware Market held 86.4% share in 2024. The strong preference among U.S. drivers for secure, contactless, and instant payments integrated directly into vehicle systems continues to drive market growth. OEMs are prioritizing the implementation of advanced security features, including biometric verification, embedded wallets, and PCI-compliant tokenization to protect consumer data and ensure payment safety. The focus on privacy standards and compliance requirements, combined with collaboration between vehicle manufacturers and financial networks, is strengthening the country's leadership in this space.

Major companies operating in the Global In-Vehicle Payment System Hardware Market include BMW, Continental, Daimler, Thales Group, Mastercard Incorporated, Harman International, Hyundai Motor Company, and Honda Motor. Key players in the in-vehicle payment system hardware market are pursuing strategic initiatives to reinforce their competitive standing and expand their technological capabilities. Companies are focusing on developing integrated payment modules equipped with advanced authentication, encryption, and connectivity features to ensure seamless and secure transactions. Strategic collaborations between automakers, fintech providers, and payment technology companies are fostering innovation and expanding ecosystem compatibility. Heavy investment in R&D is driving the creation of standardized, interoperable hardware solutions that align with global security and data protection standards.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Component

2.2.2 Payment Application

2.2.3 Technology

2.2.4 End use

2.2.5 Regional

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Value Chain Analysis & Industry Structure

3.1.1.1 Raw Materials & Wafer Fabrication

3.1.1.2 BMS IC Design & Development

3.1.1.3 Semiconductor Manufacturing & Testing

3.1.1.4 BMS Module Assembly & Integration

3.1.1.5 Battery Pack Integration & Validation

3.1.1.6 OEM Vehicle Integration & Deployment

3.1.1.7 Aftermarket & Service Ecosystem

3.1.1.8 End-of-Life Recycling & Sustainability

3.2 Supplier landscape

3.2.1 Raw material suppliers

3.2.2 Component manufacturers

3.2.3 System integrators

3.2.4 OEM

3.2.5 End use

3.3 Industry impact forces

3.3.1 Growth drivers

3.3.1.1 Surge in Connected and Smart Vehicles

3.3.1.2 Rising Consumer Preference for Contactless Payments

3.3.1.3 Growth of EVs and Charging Infrastructure

3.3.1.4 OEM-Fintech Collaborations

3.3.1.5 Smart City and Intelligent Transportation Development

3.3.2 Industry pitfalls and challenges

3.3.2.1 High Hardware and Integration Costs

3.3.2.2 Cybersecurity and Data Privacy Concerns

3.3.3 Market opportunities

3.3.3.1 Integration with Mobility-as-a-Service (MaaS)

3.3.3.2 Expansion of EV Charging and Green Mobility

3.3.3.3 Partnerships Between OEMs and Digital Wallet Providers

3.3.3.4 Emergence of Biometric Authentication in Vehicles