자동차 조명 반도체 시장 : 기회, 성장 요인, 업계 동향 분석 및 예측(2025-2034년)

Automotive Lighting Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1871106

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 190 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

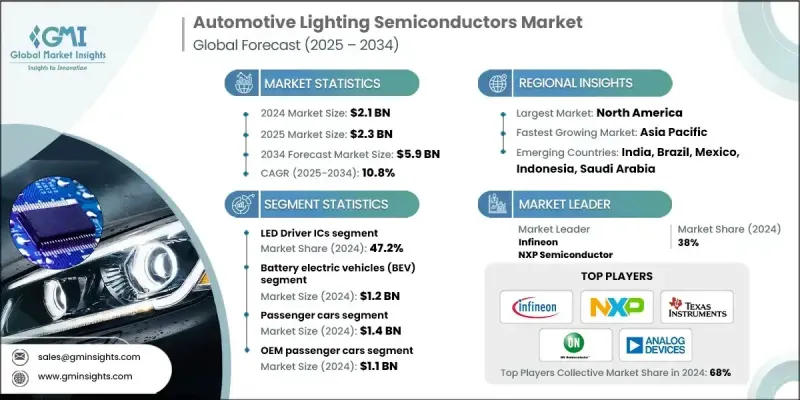

세계의 자동차 조명 반도체 시장은 2024년에 21억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR)은 10.8%를 나타낼 것으로 예측되며 59억 달러에 달할 전망입니다.

시장 성장은 기존의 할로겐 및 제논 램프에서 더 나은 밝기, 긴 수명, 낮은 에너지 소비를 제공하는 LED 및 OLED 조명 기술로의 전환에 의해 주도되고 있습니다. 자동차 제조사들은 효율성, 지속 가능성 및 차량 디자인을 향상시키기 위해 이러한 첨단 조명 시스템을 점점 더 많이 통합하고 있습니다. 주행 조건에 따라 빔 강도와 방향을 조정하는 적응형 및 스마트 조명 채택은 정밀한 실시간 제어가 가능한 반도체 수요를 가속화하고 있습니다. 이러한 혁신은 에너지 효율성, 안전성 및 전반적인 차량 성능에 중요하며, 자동차 조명 반도체를 현대 자동차 기술의 핵심 촉진제로 자리매김하고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

시작 금액

21억 달러

예측 금액

59억 달러

CAGR

10.8%

2024년 배터리 전기차(BEV) 부문은 에너지 효율적인 조명 시스템의 사용 증가로 12억 달러를 창출했습니다. BEV 생산 증가와 첨단 LED 및 적응형 조명에 대한 수요 증가는 차량 성능과 안전성 향상을 위한 반도체 채택을 촉진하고 있습니다. 제조사들은 조명 반도체의 성능, 신뢰성 및 통합 능력 향상에 주력하고 있습니다. LED 구동, 센싱, 통신 기능을 결합한 다기능 칩 개발은 자동차 제조업체에 부가가치를 창출하는 핵심 전략입니다.

2024년 승용차 부문은 14억 달러의 매출을 기록했습니다. 이 같은 주도권은 에너지 효율성, 향상된 밝기, 디자인 유연성을 제공하는 LED 및 OLED 조명의 광범위한 채택에 힘입은 것입니다. 첨단 운전자 보조 시스템(ADAS)과 적응형 헤드라이트, 자동 신호 시스템의 통합이 증가하면서 수요가 더욱 촉진되고 있습니다. 소비자들이 세련되고 안전하며 현대적인 조명 솔루션을 선호함에 따라 제조업체들은 고성능 조명 반도체에 투자하고 있습니다. 유럽, 북미, 아시아 전역에서 승용차 생산량이 증가하면서 시장 확대와 기술 발전이 지속되고 있습니다.

북미의 자동차 조명 반도체 시장은 2024년 7억 3,250만 달러에 달했습니다. 이러한 증가는 에너지 효율성, 가시성 및 디자인을 위해 승용차와 상용차 모두에서 LED 및 OLED 조명의 채택이 증가한 데 기인합니다. 적응형 헤드라이트, 자동 신호등, 지능형 조명 제어 등 ADAS 시스템의 통합은 반도체 수요를 더욱 강화합니다. 또한 증가하는 차량 생산량, 안전하고 세련된 조명에 대한 소비자 수요, 강화된 안전 규정이 북미 지역 자동차 조명 반도체 채택 확대에 기여하고 있습니다.

자동차 조명 반도체 시장 시장 진출기업은 인피니언, NXP 세미컨덕터스, 텍사스 기기, 온세미컨덕터, 아날로그 디바이스, ST 마이크로 일렉트로닉스, 모놀리식 파워시스템즈, 르네사스 일렉트로닉스, ams-오스람, 닛아화학산업, 루미레즈, 서울 반도체, 삼성 LED 등이 있습니다. 자동차 조명 반도체 시장 기업들이 채택한 주요 전략으로는 에너지 효율적이고 고성능이며 다기능 칩 개발을 위한 연구개발(R&D)에 대한 대규모 투자, 맞춤형 솔루션 공동 개발을 위한 자동차 제조사와의 전략적 파트너십 구축, 증가하는 수요 충족을 위한 제조 역량 확대 등이 있습니다. 또한 기업들은 신뢰성 및 통합 능력 향상, 적응형 및 스마트 조명 솔루션 개발, 공급망 회복탄력성 강화를 위한 현지 생산 확대에 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

영향요인

성장 촉진요인

자동차 조명 시스템에서 LED 및 OLED 기술 도입 확대

에너지 효율적이고 오래 지속되는 조명 솔루션에 대한 수요 증가

첨단 조명 시스템이 필요한 전기자동차 및 자율 주행 차량의 성장

고급스럽고 미적 감각을 갖춘 차량 디자인에 대한 소비자 선호도 상승

업계의 잠재적 억제요인 및 과제

높은 도입 및 통합 비용

시장의 세분화와 상호 운용성

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

신흥 비즈니스 모델

규정 준수 요건

소비자 심리 분석

특허 및 지적재산 분석

지정학적 및 무역 동향

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

시장 집중도 분석

주요 기업의 경쟁 벤치마킹

재무실적 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인의 폭

기술

혁신

지리적 존재 비교

세계 전개 분석

서비스 네트워크 커버리지

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

선도기업(Leaders)

도전 기업(Challengers)

추종 기업(Followers)

틈새 시장 기업(Niche players)

전략적 전망 매트릭스

주요 발전(2021-2024년)

합병 및 인수

제휴 및 협력 관계

기술 발전

확대 및 투자 전략

디지털 전환의 대처

신흥/스타트업 경쟁기업의 정세

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

주요 동향

LED 드라이버 IC

전원 관리 IC(PMIC)

마이크로컨트롤러(MCU)

광전자 부품

개별 부품

제6장 시장 추계 및 예측 : 차량 파워트레인별(2021-2034년)

주요 동향

내연 기관(ICE) 차량

하이브리드 전기자동차/플러그인 하이브리드 전기자동차(HEV/PHEV)

배터리 전기자동차(BEV)

제7장 시장 추계 및 예측 : 차종별(2021-2034년)

주요 동향

승용차

소형 상용차(LCV)

대형 상용차(HCV)

제8장 시장 추계 및 예측 : 최종 용도 고객별(2021-2034년)

주요 동향

OEM 승용차

OEM 상용차

1차 공급업체

애프터마켓

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

한국

호주

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

Infineon

NXP Semiconductors

Texas Instruments

ON Semiconductor

Analog Devices

STMicroelectronics

Monolithic Power Systems

Renesas Electronics

ams-OSRAM

Nichia

Lumileds

Seoul Semiconductor

Samsung LED

HBR

영문 목차

영문목차

The Global Automotive Lighting Semiconductors Market was valued at USD 2.1 Billion in 2024 and is estimated to grow at a CAGR of 10.8% to reach USD 5.9 Billion by 2034.

The market growth is driven by the shift from traditional halogen and xenon lamps to LED and OLED lighting technologies, which provide better brightness, longer life, and lower energy consumption. Automotive manufacturers are increasingly integrating these advanced lighting systems to enhance efficiency, sustainability, and vehicle design. The adoption of adaptive and smart lighting, which adjusts beam intensity and direction based on driving conditions, is accelerating demand for semiconductors capable of precise real-time control. These innovations are critical for energy efficiency, safety, and overall vehicle performance, positioning automotive lighting semiconductors as a key enabler of modern automotive technology.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.1 Billion

Forecast Value

$5.9 Billion

CAGR

10.8%

In 2024, the battery electric vehicles (BEV) sector generated USD 1.2 Billion owing to the rising use of energy-efficient lighting systems. The increasing production of BEVs, coupled with growing demand for advanced LED and adaptive lighting, is driving semiconductor adoption for improved vehicle performance and safety. Manufacturers are focusing on enhancing the performance, reliability, and integration capabilities of lighting semiconductors. Developing multifunctional chips that combine LED driving, sensing, and communication features is a key strategy to add value for automakers.

The passenger car segment generated USD 1.4 Billion in 2024. This leadership is fueled by widespread adoption of LED and OLED lighting, offering energy efficiency, improved brightness, and design flexibility. The increasing integration of advanced driver-assistance systems (ADAS) with adaptive headlights and automated signaling further boosts demand. Consumer preference for stylish, safe, and modern lighting solutions is driving manufacturers to invest in high-performance lighting semiconductors. Rising production of passenger vehicles across Europe, North America, and Asia supports sustained market expansion and technological advancement.

North America Automotive Lighting Semiconductors Market reached USD 732.5 million in 2024. This increase is attributed to greater adoption of LED and OLED lighting in both passenger and commercial vehicles for energy efficiency, visibility, and design. Integration of ADAS systems, including adaptive headlights, automated signaling, and intelligent lighting controls, further strengthens semiconductor demand. Additionally, rising vehicle production, consumer demand for safe and stylish lighting, and stricter safety regulations contribute to the growing deployment of automotive lighting semiconductors in North America.

Prominent Automotive Lighting Semiconductors Market participants include Infineon, NXP Semiconductors, Texas Instruments, ON Semiconductor, Analog Devices, STMicroelectronics, Monolithic Power Systems, Renesas Electronics, ams-OSRAM, Nichia, Lumileds, Seoul Semiconductor, and Samsung LED. Key strategies adopted by companies in the automotive lighting semiconductors market include investing heavily in research and development to create energy-efficient, high-performance, and multifunctional chips, forming strategic partnerships with automakers to co-develop tailored solutions, and expanding manufacturing capabilities to meet growing demand. Firms are also focusing on improving reliability and integration capabilities, developing adaptive and smart lighting solutions, and localizing production to strengthen supply chain resilience.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Product Type

2.2.2 Vehicle Powertrain

2.2.3 Vehicle Class

2.2.4 End Use Analysis

2.2.5 Regional trends

2.3 TAM Analysis, 2025-2034 (USD Million)

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Impact forces

3.2.1 Growth drivers

3.2.1.1 Rising adoption of LED and OLED technologies in vehicle lighting systems

3.2.1.2 Increasing demand for energy-efficient and long-lasting lighting solutions

3.2.1.3 Growth in electric and autonomous vehicles requiring advanced lighting systems

3.2.1.4 Rising consumer preference for premium and aesthetic vehicle designs