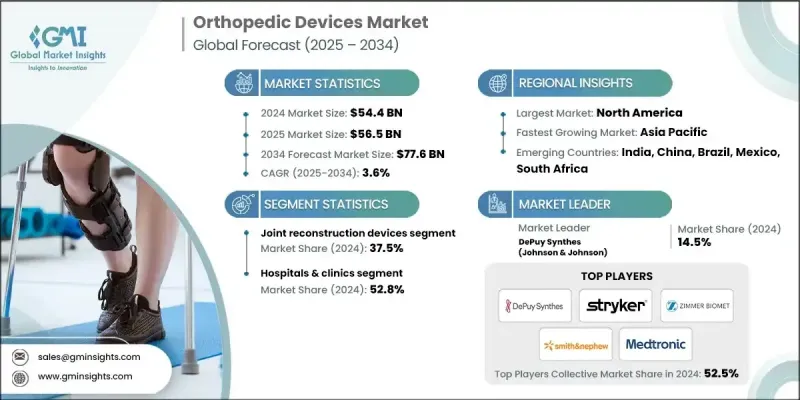

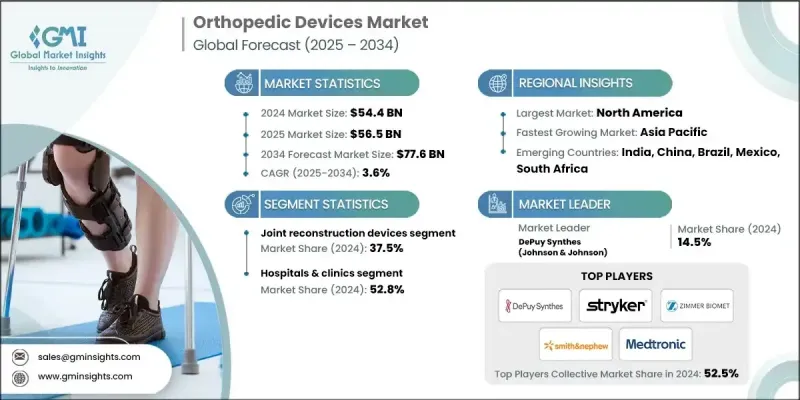

세계의 정형외과용 디바이스 시장은 2024년에 544억 달러로 평가되었고 CAGR 3.6%를 나타내 2034년에는 776억 달러에 이를 것으로 예측되고 있습니다.

성장의 원동력은 근골격계 질환의 세계 부담 증가, 노화, 정형외과 기술의 끊임없는 혁신입니다. 정형외과 장치는 운동 능력 향상, 통증 완화, 환자의 삶의 질 향상에 필수적입니다. 이 업계는 관절 임플란트, 척추 시스템, 외상 장치, 수술 정밀도 및 수술 후 관리를 향상시키는 디지털 도구와 같은 고급 솔루션을 제공하여 건강 관리 제공업체, 생명 과학 회사 및 디지털 건강 플랫폼을 지원합니다. 조기 개입에 대한 의식이 높아지고, 건강 관리에 대한 지출 증가, 낮은 침습 기술의 출현이 수요를 더욱 높이고 있습니다. 선진국 시장이든 신흥 시장이든, 이러한 의료기기는 조기 회복, 개인화 치료, 임상 효율 개선으로 정형외과 의료의 형태를 바꾸고 있습니다. 또한 사고율 상승, 스포츠 관련 부상, 다운타임을 단축하는 기술적으로 고도의 치료에 대한 환자의 기호도 수요를 지지하고 있습니다. 병원과 수술센터가 디지털 수술 시스템과 로봇 수술 시스템을 도입함에 따라 정형외과 장치의 역할은 다양한 의료 현장에서 계속 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 544억 달러 |

| 예측 금액 | 776억 달러 |

| CAGR | 3.6% |

관절 재건기구 부문은 2024년에 37.5%의 점유율을 차지했습니다. 퇴행성 관절 질환 진단 증가와, 특히 노인의 인공 고관절 치환술 및 인공 슬관절 치환술의 건수 증가가 이 분야를 밀어 올리는 주요 요인입니다. 이 장비는 관절의 기능을 회복시키고 만성 불쾌감을 완화하기 위해 수술 적 개입이 필요한 이동성을 손상시키는 상태를 관리하는 데 필수적입니다.

척추기구 분야는 2024년에 117억 달러를 창출했고 2034년까지 안정된 CAGR 2.8%를 나타낼 것으로 예측됩니다. 이 분야 시장 확대에는 고령화와 앉을 수 없는 생활 스타일에 기인하는 척추 질환의 환자수 증가가 크게 기여하고 있습니다. 침습성이 낮은 수술이 선호되고 첨단 척추 기술에 대한 수요가 높아지고 있습니다. 움직임을 유지하는 임플란트, 생체 흡수성 구성요소, 이미지 유도 시스템 등의 최근 기술 혁신으로 치료 성적이 향상되고 수술 후 합병증 감소에 도움이 되기 때문에 척추 수술은 더욱 친숙하고 효과적입니다.

2024년 북미의 정형외과용 디바이스 시장 점유율은 55.6%에 달했습니다. 이 지역의 강력한 건강 관리 인프라와 새로운 의료 기술에 대한 많은 투자가 정형외과 솔루션의 광범위한 채택을 지원합니다. 인구의 고령화와 관절염, 비만, 관절 관련 질환의 다발이 계속해서 높은 수요를 견인하고 있습니다. 이 지역에서는 조기 진단·조기 개입이 선호되고 스포츠 관련 외상 발생률도 증가하고 있기 때문에 정형외과용 임플란트나 기구의 임상 현장에서의 사용이 더욱 가속되고 있습니다.

세계의 정형외과용 디바이스 시장에 진입하는 주요 업계 기업은 Enovis, ATEC, MicroPort Scientific, DePuy Synthes(J& J), Stryker, Waldemar, Zimmer Biomet, Arthrex, TriMed, ConforMIS, Integra, CONMED, Globus Medical &Nephew, Medtronic, Medacta 등이 있습니다. 세계의 정형외과용 디바이스 시장에서 주요 기업들은 기술 혁신, 세계 전개, 전략적인수를 통해 존재감을 높이는 데 주력하고 있습니다. 지속적인 R&D 투자를 통해 차세대 임플란트, 로봇 지원 시스템 및 환자 전용 장치를 개발하고 있습니다. 파트너십과 현지 생산을 통해 신흥 시장에 진출함으로써 증가하는 수요와 규제 요구를 충족시킬 수 있습니다. 각 회사는 또한 임상 결과를 개선하기 위해 AI를 활용한 수술 계획 도구 및 원격 환자 모니터링과 같은 디지털 기술에 투자하고 있습니다.

The Global Orthopedic Devices Market was valued at USD 54.4 billion in 2024 and is estimated to grow at a CAGR of 3.6% to reach USD 77.6 billion by 2034.

The growth is powered by the increasing global burden of musculoskeletal conditions, an aging population, and continual innovations in orthopedic technology. Orthopedic devices are becoming essential in improving mobility, reducing pain, and enhancing patients' quality of life. The industry supports healthcare providers, life sciences firms, and digital health platforms by delivering advanced solutions such as joint implants, spinal systems, trauma devices, and digital tools that elevate surgical precision and post-operative care. Growing awareness around early interventions, increased spending on healthcare, and the emergence of minimally invasive techniques have further elevated demand. In both developed and emerging markets, these devices are reshaping orthopedic care by providing faster recovery, personalized treatment, and improved clinical efficiency. Demand is also being supported by rising accident rates, sports-related injuries, and patient preference for technologically advanced procedures that reduce downtime. As hospitals and surgical centers adopt digital and robotic surgical systems, the role of orthopedic devices continues to expand across diverse care settings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $54.4 Billion |

| Forecast Value | $77.6 Billion |

| CAGR | 3.6% |

The joint reconstruction devices segment held a 37.5% share in 2024. Increasing diagnoses of degenerative joint diseases and the growing volume of hip and knee replacement surgeries, especially among older adults, are primary factors boosting this segment. These devices are essential in managing conditions that impair mobility and require surgical intervention to restore joint functionality and relieve chronic discomfort.

The spinal devices segment generated USD 11.7 billion in 2024 and is forecasted to grow at a steady CAGR of 2.8% through 2034. Market expansion in this segment is largely attributed to the growing number of people affected by spinal conditions, often driven by aging demographics and sedentary lifestyles. The preference for less invasive surgical procedures has fueled demand for advanced spine technologies. Recent innovations in motion-preserving implants, bioresorbable components, and image-guided systems are improving outcomes and helping reduce post-operative complications, making spinal procedures more accessible and effective.

North America Orthopedic Devices Market held a 55.6% share in 2024. The region's strong healthcare infrastructure, along with significant investments in new medical technologies, has supported the wide adoption of orthopedic solutions. An aging population, coupled with high incidences of arthritis, obesity, and joint-related disorders, continues to drive high demand. The region's preference for early diagnosis and intervention, as well as the increasing rate of sports-related trauma, has further fueled the use of orthopedic implants and devices across clinical environments.

Major industry players involved in the Global Orthopedic Devices Market include Enovis, ATEC, MicroPort Scientific, DePuy Synthes (J&J), Stryker, Waldemar, Zimmer Biomet, Arthrex, TriMed, ConforMIS, Integra, CONMED, Globus Medical, aap Implantate, B. Braun, Smith & Nephew, Medtronic, and Medacta. Leading companies in the Global Orthopedic Devices Market are focused on strengthening their presence through innovation, global expansion, and strategic acquisitions. Continuous R&D investments allow them to develop next-generation implants, robotics-assisted systems, and patient-specific devices. Expanding into emerging markets through partnerships and localized manufacturing helps meet growing demand and regulatory needs. Companies are also investing in digital technologies like AI-driven surgical planning tools and remote patient monitoring to elevate clinical outcomes.