발효 유래 천연 향료 시장 : 시장 기회 및 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Fermentation-Derived Natural Flavors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1858849

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

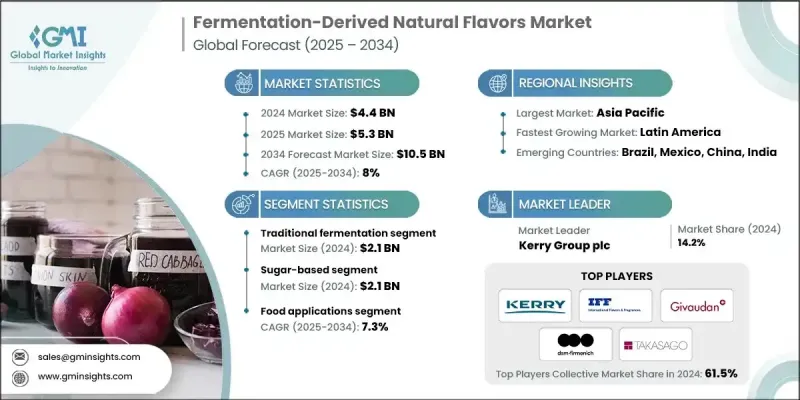

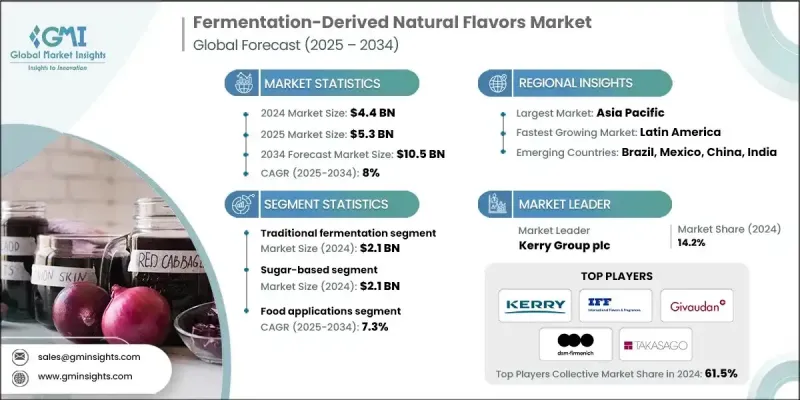

세계의 발효 유래 천연 향료 시장은 2024년에 44억 달러로 평가되었고, CAGR 8%로 성장할 전망이며, 2034년에는 105억 달러에 이를 것으로 추정됩니다.

시장의 성장은 깨끗한 라벨로 지속 가능한 원료에 대한 소비자 수요 증가 및 생명공학의 급속한 발전으로 빠르게 진화하고 있습니다. 친환경적인 생산 방법으로의 전환은 재생가능한 원료 및 순환형 경제에 대한 지향 증가와 함께 업계를 재구성하고 있습니다. 변동성이 큰 농산물 가격으로 인해 제조업체들은 비용을 안정시킬 뿐만 아니라 환경 발자국을 줄이는 대체 원자재를 채택하게 되었습니다. 한편, 정밀 발효는 획기적인 혁신으로 부상하고 있습니다. 인공 미생물과 합성 생물학을 통해 기업은 전통적으로 접근할 수 없었던 고도로 표적화된 풍미 분자를 생산할 수 있게 되었습니다. 순도, 일관성 및 확장성 향상은 미생물주공학과 바이오프로세스 최적화에 대한 엄청난 투자를 유도하고 있습니다. 이러한 진보는 천연 향료의 창조 및 식음료에 대한 용도에 변화를 가져오고 있습니다. 시장 개척은 특히 선진지역에서 유리한 규제 프레임워크 및 생명공학을 기반으로 하는 식품 소재에 대한 소비자의 관심 증가에 의해 더욱 지원되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

44억 달러

예측 금액

105억 달러

CAGR

8%

전통적인 발효 분야는 2024년에 21억 달러를 창조했습니다. 이 방법은 자본 요건이 낮고 소비자 신뢰가 두꺼우며, 규제가 완만해, 특히 GRAS 분류 식품 안전 미생물이 일반적으로 사용되기 때문에 여전히 인기가 있습니다. 이러한 기술은 전통 요리와 장인 식품 분야와 같은 화합물의 순도보다 맛의 복잡성이 중요한 시장에 특히 적합합니다. 이러한 용도에서는 전통적인 발효가 예산적 요구와 문화적 기대 모두에 부합합니다.

설탕 기반 원료 부문은 2024년에 21억 달러를 창출했으며, 2034년까지의 예측 점유율은 48%로 성장할 전망입니다. 성장률은 7%로 완만하며, 이 분야는 수년간 확립된 공급망과 최적화된 발효 기술로부터 이익을 얻고 있습니다. 일반적인 당류 유래의 원료는 미생물 풍미 화합물의 생산에 필수적인 쉽게 발효 가능한 탄소원을 제공합니다. 이 부문의 성장률은 안정적이지만 신뢰성과 운영 효율성이 높기 때문에 많은 대규모 발효 사업의 핵심 역할을 계속하고 있습니다.

북미 발효 유래 천연 향료 시장은 2024년에 36%의 점유율을 차지하였고, 2034년까지 7%의 연평균 복합 성장률(CAGR)로 성장할 것으로 예측되고 있습니다. 이 지역 성장의 원동력이 되고 있는 것은 첨단 생명공학 및 에코시스템, 천연 성분이나 클린 라벨 성분에 대한 왕성한 소비자 수요, 생명공학 유래 식품 성분의 상업화를 촉진하는 규제 프레임워크입니다. 이 지역에서 연구개발 및 생산 시설을 운영하고 있는 대기업은 진화하는 소비자의 기대에 부응하기 위해 풍미개발의 혁신을 가속화하고 있습니다.

세계의 발효 유래 천연 향료 시장 경쟁 구도를 형성하고 있는 기업으로는 Robertet SA, Symrise AG, DSM-Firmenich, Givaudan SA, Sensient Technologies Corporation, Kerry Group plc, International Flavors & Fragrances Inc., Chr. Hansen Holding A/S, Takasago International Corporation, Ginkgo Bioworks Holdings Inc. 등이 있습니다. 발효 유래 천연 향료 시장의 주요 기업은 미생물 균주의 성능을 개선하고 풍미의 수율을 극대화하기 위해 적극적으로 연구 개발에 투자하고 있습니다. 많은 기업들이 정밀 발효 기술을 채택하여 우수한 순도 및 확장성을 제공하는 고가치 틈새 풍미 화합물을 생산하고 있습니다. 또한 기업은 원료 조달의 다양화에 주력하고 있으며 환경에 미치는 영향과 생산 리스크를 줄이기 위해 지속 가능하고 비용 효율적인 원료를 채용하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

천연 소재에 대한 소비자 수요 증가

바이오테크놀러지 용도에 대한 규제 지원

정밀 발효에서 기술의 진보

업계의 잠재적 위험 및 과제

높은 초기 투자 요건

복잡한 규제 승인 프로세스

공급망 최적화 및 원료 조달

시장 기회

식물 유래 및 기능성 식품 부문에 대한 진출

지역의 원료를 사용한 지역별 향료 프로파일 개발

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

원료 유형별

향후 시장 동향

기술 및 혁신의 전망

현재의 기술 동향

신흥 기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 대해서만 제공됨)

주요 수입국

주요 수출국

지속가능성 및 환경 측면

지속가능한 실천

폐기물 감축 전략

생산에서 에너지 효율

환경 친화적인 노력

탄소발자국

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병 및 인수

파트너십

신제품 발표

확장 계획

제5장 시장 추계 및 예측 : 생산 기술별(2021-2034년)

주요 동향

정밀 발효

전통 발효

하이브리드 생물 변환

제6장 시장 추계 및 예측 : 원료 유형별(2021-2034년)

주요 동향

설탕 기반 원료

사탕수수

설탕 비트

포도당

과당

전분계 원료

옥수수

카사바

감자

밀 전분

셀룰로오스계 및 폐기물계 원료

농업 잔류물

식품 폐기물

특수 기재

단백질 가수분해물

해양 바이오매스

신규 기재

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

식품 용도

가공 식품

구운 과자

과자류

음료 용도

청량 음료

알코올 음료

기능성 음료

유제품 및 식물성 대체품

전통적인 유제품

식물성 우유

치즈 대체품

화장품 및 퍼스널케어

화장품 원료

향수 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Cargill Inc

Archer Daniels Midland Company

Bunge Limited

COFCO Corporation

Louis Dreyfus Company

Verdesian Life Sciences

Avani Seeds Ltd

Lidea

Buhler

Nestle

Agrovita Foods

AJY

영문 목차

영문목차

The Global Fermentation-Derived Natural Flavors Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 8% to reach USD 10.5 billion by 2034.

The market growth is rapidly evolving, driven by rising consumer demand for clean-label, sustainable ingredients and rapid advances in biotechnology. The shift toward environmentally responsible production methods is reshaping the industry, with a growing preference for renewable feedstocks and circular economy practices. Volatile agricultural commodity prices have pushed manufacturers to adopt alternative raw materials, which not only stabilize costs but also reduce environmental footprints. Meanwhile, precision fermentation is emerging as a game-changing innovation. Through engineered microbes and synthetic biology, companies are now capable of producing highly targeted flavor molecules that were previously inaccessible via conventional methods. Enhanced purity, consistency, and scalability are attracting massive investments in microbial strain engineering and bioprocess optimization. These advancements are transforming the creation and integration of natural flavors into food and beverage applications. Market growth is further supported by a favorable regulatory framework and growing consumer interest in biotechnology-based food ingredients, especially in developed regions.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$4.4 Billion

Forecast Value

$10.5 Billion

CAGR

8%

The traditional fermentation segment generated USD 2.1 billion in 2024. This method remains popular due to its lower capital requirements, consumer trust, and regulatory ease, especially since it typically uses food-safe microorganisms with GRAS classification. These techniques are particularly well-suited for markets where flavor complexity is more critical than compound purity, including heritage cuisines and artisanal food segments. In such applications, traditional fermentation aligns with both budgetary needs and cultural expectations.

The sugar-based feedstocks segment generated USD 2.1 billion in 2024, holding a 48% share projected through 2034. Growing at a moderate 7% rate, this segment benefits from long-established supply chains and well-optimized fermentation technologies. Feedstocks derived from common sugars offer readily fermentable carbon sources that are essential for microbial flavor compound production. While its growth rate is steady, the segment continues to serve as the backbone of many large-scale fermentation operations due to its reliability and operational efficiency.

North America Fermentation-Derived Natural Flavors Market held a 36% share in 2024 and is expected to grow at a 7% CAGR through 2034. The region's growth is powered by an advanced biotech ecosystem, robust consumer demand for natural and clean-label ingredients, and regulatory frameworks that facilitate the commercialization of biotech-derived food components. Major players operating R&D and production facilities in the region are accelerating innovation in flavor development to meet evolving consumer expectations.

Companies shaping the competitive landscape of the Global Fermentation-Derived Natural Flavors Market include Robertet SA, Symrise AG, DSM-Firmenich, Givaudan SA, Sensient Technologies Corporation, Kerry Group plc, International Flavors & Fragrances Inc., and Chr. Hansen Holding A/S, Takasago International Corporation, and Ginkgo Bioworks Holdings Inc., leading firms in the Fermentation-Derived Natural Flavors Market, are aggressively investing in R&D to refine microbial strain performance and maximize flavor yield. Many are adopting precision fermentation technologies to produce high-value, niche flavor compounds that offer superior purity and scalability. Companies are also focusing on diversifying raw material sourcing, embracing sustainable and cost-effective feedstocks to reduce environmental impact and production risks.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Admixtures

2.2.3 Application Methods

2.2.4 Application

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing Consumer Demand for Natural Ingredients

3.2.1.2 Regulatory Support for Biotechnology Applications

3.2.1.3 Technological Advancements in Precision Fermentation

3.2.2 Industry pitfalls and challenges

3.2.2.1 High Initial Capital Investment Requirements

3.2.2.2 Complex Regulatory Approval Processes

3.2.2.3 Supply Chain Optimization & Raw Material Sourcing

3.2.3 Market opportunities

3.2.3.1 Expansion into Plant-Based and Functional Food Segments

3.2.3.2 Development of Region-Specific Flavor Profiles Using Local Feedstocks

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation Landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By feedstock type

3.8 Future market trends

3.9 Technology and Innovation Landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Production Technology, 2021 - 2034 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Precision fermentation

5.3 Traditional fermentation

5.4 Hybrid biotransformation

Chapter 6 Market Estimates and Forecast, By Feedstock Type, 2021 - 2034 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Sugar-Based Feedstocks

6.2.1 Sugarcane

6.2.2 Sugar Beet

6.2.3 Glucose

6.2.4 Fructose

6.3 Starch-Based Feedstocks

6.3.1 Corn

6.3.2 cassava

6.3.3 potato

6.3.4 wheat starch

6.4 Cellulosic & Waste Feedstocks

6.4.1 Agricultural residues

6.4.2 Food Waste

6.5 Specialized Substrates

6.5.1 Protein hydrolysates

6.5.2 Marine biomass

6.5.3 Novel substrates

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Food Applications

7.2.1 Processed foods

7.2.2 Baked goods

7.2.3 Confectionery

7.3 Beverage Applications

7.3.1 Soft drinks

7.3.2 Alcoholic beverages,

7.3.3 Functional drinks

7.4 Dairy & Plant-Based Alternatives

7.4.1 Traditional dairy

7.4.2 Plant-based milk

7.4.3 Cheese alternatives

7.5 Cosmetics & Personal Care

7.5.1 Cosmetic ingredients

7.5.2 Fragrance applications

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)