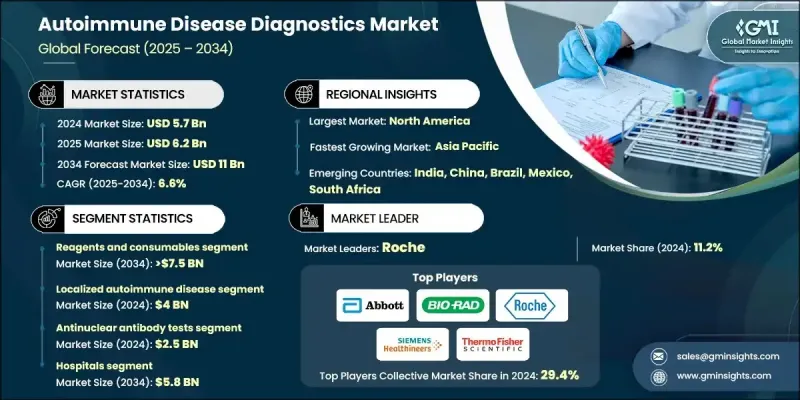

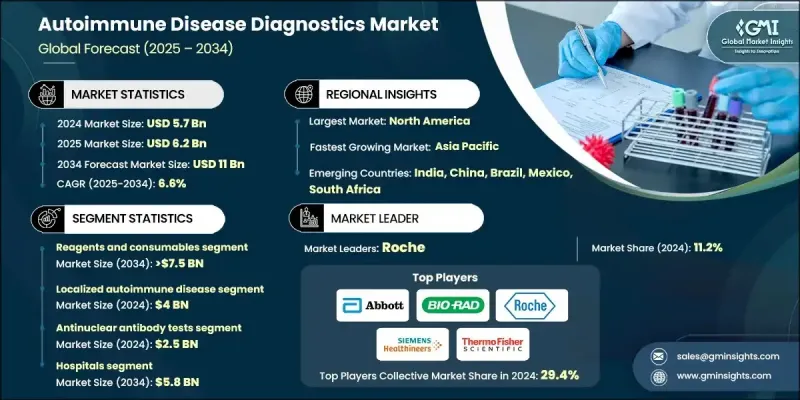

세계의 자가면역질환 진단 시장은 2024년 57억 달러로 평가되었으며 CAGR 6.6%로 성장해 2034년까지 110억 달러에 이를 것으로 추정됩니다.

자가면역질환의 이환율 상승, 조기진단에 대한 인식 증가, 지속적인 스크리닝 프로그램, 진단기술의 꾸준한 진보가 시장 확대에 박차를 가하고 있습니다. 건강 관리 지출 개선 및 조기 발견을 위한 혁신적인 도구의 도입은 정확하고 신속한 검사에 대한 수요를 강화하고 있습니다. 분자 분석에서 면역 분석, 바이오마커 기반 검출에 이르기까지 진단 능력은 임상 요구 증가에 따라 진화하고 있습니다. 정부 및 의료 기관이 주도하는 환자 교육 캠페인은 검사 건수를 크게 증가시키고 있습니다. 동시에 특정 바이오마커를 이용한 정밀진단의 채용이 확대되고 있어 질병의 조기 발견이나 환자별 모니터링을 통해 결과가 개선되고 있습니다. 자가면역질환을 위한 휴대용, 신속한 검사 솔루션도 인기를 끌고 있으며, 다양한 의료 현장에서 신속한 결과를 제공하여 시장 기세를 더욱 가속화하고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시장 규모 | 57억 달러 |

| 예측 금액 | 110억 달러 |

| CAGR | 6.6% |

2024년 시약 및 소모품 부문은 자가면역 검사에서 반복적으로 사용되기 때문에 67%의 점유율을 차지했습니다. 진단 응용 분야에서 분석 키트, 항체 및 완충액의 끊임없는 요구가 이 분야의 안정적인 성장에 기여하고 있습니다. 진단과 장기적인 질병 모니터링 모두에서 검사가 더 자주 수행됨에 따라 이러한 물질에 대한 수요가 증가하고 있습니다. 검사기관과 진료소는 정확하고 효율적인 진단을 위해 소모품에 크게 의존하고 있으며, 이 부문에서 안정적인 수익원을 창출하고 있습니다.

국소자가면역질환 분야는 2024년 40억 달러를 창출해 2034년까지 연평균 복합 성장률(CAGR) 6.4%를 보일 것으로 예측됩니다. 이 부문에는 갑상선 질환, 염증성 장 질환, 1형 당뇨병 등 특정 장기를 표적으로 하는 질병이 포함되어 세계에서 진단되고 있습니다. 이러한 장기 특이적 질환 증가는 국소적인 질병 검출에 특화된 고감도 및 고정밀 진단 약물에 대한 요구를 부추기는 것입니다. 이 분야의 지속적인 성장은 장기적인 합병증을 피하기 위해 조기 개입과 일관된 모니터링의 필요성에 의해 지원됩니다.

2024년 북미 자가면역질환 진단 점유율은 36.6%이었습니다. 이 지역에서는 다발성 경화증, 낭창, 류마티스 관절염, 1형 당뇨병과 같은 자가면역질환의 이환율이 세계적으로 가장 높습니다. 이러한 환자 수 증가는 고급 진단 검사에 대한 큰 수요를 이끌고 있습니다. 강력한 건강 관리 인프라와 광범위한 스크리닝 이니셔티브를 통해 이 지역은 루틴과 고급 자가면역 검사를 계속 지원합니다. 조기 진단과 맞춤형 의료가 중시되어 시장 성장을 더욱 뒷받침하고 있습니다.

세계 자가면역질환 진단 시장에서 활약하고 있는 주요 기업은 Euroimmun, Thermo Fisher Scientific, Roche, Quest Diagnostics, Inova Diagnostics(Werfen), DIAsource, Trinity Biotech, Revvvity, Labcorp, Siemens Healthineers, GRIFOLS, Hemagen Diagnostics, BIO-RAD, BIOMERIEUX, Abbott 등입니다. 자가면역질환 진단 시장의 기업은 전략적 제휴, 인수, 첨단기술에 대한 투자를 통해 포트폴리오를 확대하고 있습니다. 많은 기업들은 감도와 속도를 향상시키기 위해 바이오마커를 기반으로 하는 진단제 및 차세대 분자 도구 개발에 주력하고 있습니다. 연구개발에 대한 투자 확대로 기업은 포인트 오브 케어 검사 키트 등 보다 정밀하고 사용하기 쉬운 진단 플랫폼을 도입할 수 있게 되었습니다. 기업은 또한 실험실 워크플로우를 간소화하고 처리량을 향상시키기 위해 자동화를 선호합니다.

The Global Autoimmune Disease Diagnostics Market was valued at USD 5.7 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 11 billion by 2034.

Rising incidence rates of autoimmune conditions, higher awareness about early diagnosis, ongoing screening programs, and steady advancements in diagnostic technologies are fueling market expansion. Improved healthcare spending and the introduction of innovative tools for early detection have also strengthened the demand for accurate and rapid testing. From molecular assays to immunoassays and biomarker-based detection, diagnostic capabilities are evolving to meet growing clinical needs. Patient education campaigns, led by both governments and healthcare organizations, are significantly raising testing volumes. At the same time, precision diagnostics utilizing specific biomarkers are seeing greater adoption, improving outcomes through early disease detection and patient-specific monitoring. Portable and rapid testing solutions for autoimmune disorders are also gaining popularity, offering quicker results in various care settings and further driving market momentum.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.7 Billion |

| Forecast Value | $11 Billion |

| CAGR | 6.6% |

In 2024, the reagents and consumables segment held 67% share owing to their recurring use in autoimmune testing procedures. The constant need for assay kits, antibodies, and buffers across diagnostic applications is contributing to the segment's consistent growth. As testing becomes more frequent for both diagnosis and long-term disease monitoring, the demand for these materials continues to rise. Laboratories and clinics rely heavily on consumables to perform accurate and efficient diagnostics, creating a steady revenue stream within the segment.

The localized autoimmune disease segment generated USD 4 billion in 2024 and is expected to grow at a CAGR of 6.4% through 2034. This segment includes conditions such as thyroid disorders, inflammatory bowel diseases, and Type 1 diabetes diseases targeting specific organs and increasingly being diagnosed worldwide. The rise in these organ-specific conditions fuels the need for highly sensitive and precise diagnostics tailored to localized disease detection. Continued growth in this area is supported by the need for early intervention and consistent monitoring to avoid long-term complications.

North America Autoimmune Disease Diagnostics Market held 36.6% share in 2024. The region reports one of the highest rates of autoimmune disorders globally, including multiple sclerosis, lupus, rheumatoid arthritis, and Type 1 diabetes. This growing patient population drives significant demand for advanced diagnostic testing. With a strong healthcare infrastructure and widespread screening initiatives, the region continues to support both routine and advanced autoimmune testing. The emphasis on early diagnosis and personalized care further sustains market growth.

Major players active in the Global Autoimmune Disease Diagnostics Market include Euroimmun, Thermo Fisher Scientific, Roche, Quest Diagnostics, Inova Diagnostics (Werfen), DIAsource, Trinity Biotech, Revvity, Labcorp, Siemens Healthineers, GRIFOLS, Hemagen Diagnostics, BIO-RAD, BIOMERIEUX, and Abbott. Companies in the autoimmune disease diagnostics market are expanding their portfolios through strategic collaborations, acquisitions, and investments in advanced technologies. Many are focusing on developing biomarker-based diagnostics and next-generation molecular tools to improve sensitivity and speed. Increased investment in R&D is enabling firms to introduce more precise and user-friendly diagnostic platforms, including point-of-care testing kits. Companies are also prioritizing automation to streamline lab workflows and enhance throughput.