가정용 냉장고 및 냉동고 시장 : 기회, 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Household Refrigerators and Freezers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1844333

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 166 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

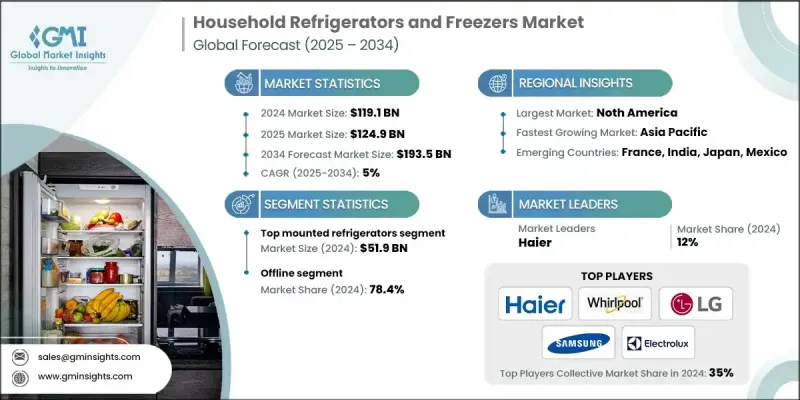

세계의 가정용 냉장고 및 냉동고 시장 규모는 2024년 1,191억 달러에 달했고, CAGR 5%로 성장하여 2034년까지 1,935억 달러에 이를 것으로 예측됩니다.

환경의 지속가능성에 대한 소비자의 의식 증가와 전기요금의 상승은 에너지 효율적인 가전제품에 대한 수요를 촉진하고 있습니다. 소비자는 현재 성능에 타협하지 않고 고급 에너지 절약 기능을 제공하는 가전제품을 선호합니다. 이러한 추세는 친환경 제품을 추진하는 정부의 이니셔티브와 규제 정책의 확대로 더욱 강화되고 있습니다. 동시에, 가정은 더 큰 통제와 편리함을 제공하는 스마트 기술을 채택하고 있습니다. 최근 냉장고에는 터치 스크린 패널, 가상 어시스턴트 대응, 무선 접속 등의 기능이 탑재되어, 사용자는 원격지에서 수납 관리, 재고 감시, 통합 서비스에 액세스할 수 있게 되었습니다. 스마트 홈과 커넥티드 가전의 융합은 쾌적성, 효율성, 실시간 응답성에 대한 기호의 변화를 반영하여 시장 상황의 재구축을 계속하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

1,191억 달러

예측 금액

1,935억 달러

CAGR

5%

상단형 냉장고 부문은 2024년 519억 달러로 시장에서 주도적 지위를 유지했습니다. 이 모델은 냉동실이 주요 냉장고 위에 있으며 저렴한 가격과 공간 절약형 디자인으로 인기를 얻고 있습니다. 저가격이기 때문에 선진국 및 신흥국을 불문하고 가치 중시 소비자에게 이상적인 선택지가 되고 있습니다. 컴팩트하고 사용하기 쉽고 안정적인 성능은 시장에서 강한 존재감을 지원합니다.

오프라인 유통 채널 부문은 2024년에 78.4%의 점유율을 차지합니다. 상점에서의 쇼핑은 구매자가 실제로 가전제품을 점검하고, 기능을 평가하고, 훈련받은 판매 직원의 지도하에 충분한 정보를 바탕으로 결정을 내릴 수 있도록 합니다. 소비자는 개인 지원, 제품의 즉각적인 시연, 배송, 설치, 유지보수 등의 서비스 편의성에 큰 가치를 두고 있습니다. 이러한 몰입감 있는 서비스 중심의 소매 경험은 가전제품 부문에서 오프라인 리더십을 유지하는 데 큰 역할을 하고 있습니다.

2024년 미국 가정용 냉장고 및 냉동고 시장의 점유율은 74.9%로, 소비자의 왕성한 구매력과 프리미엄으로 고성능의 가전제품에 대한 기호의 고조가 보급을 촉진했습니다. 지능형 홈 에코시스템의 통합으로 앱 제어, 에너지 모니터링, 디지털 인터페이스 등 스마트 기능을 갖춘 냉장고에 대한 수요가 가속화되고 있습니다. 또한 미국 소비자들은 지속가능성 목표에 따른 혁신에 높은 반응을 보이며 에너지 효율적인 모델의 성장을 지원하고 있습니다.

세계의 가정용 냉장고 및 냉동고 시장에서 활동하는 주요 기업으로는 Toshiba, Samsung, Whirlpool, Gree, Panasonic, LG, Midea, Haier, Arcelik, Liebherr, Hisense, BSH, Sharp, Hitachi, Electrolux 등이 있습니다. 가정용 냉장고 및 냉동고 시장의 각 회사는 경쟁력을 강화하기 위해 제품 혁신, 지속가능성 및 디지털 통합에 주력하고 있습니다. 많은 브랜드들은 IoT 기능, AI 기반 내용물 추적, 모바일 연결을 통합하여 스마트 가전 포트폴리오를 확대하고 있습니다. 규제 기준과 친환경 솔루션에 대한 소비자 수요를 충족하기 위해 제조업체는 인버터 기술과 친환경 냉매로 에너지 효율을 높입니다. 지리적 확대, 특히 신흥 시장 진출도 현지 생산과 소매 파트너십에 뒷받침된 핵심 전략 중 하나입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

업계에 미치는 영향요인

성장 촉진요인

에너지 절약 가전 수요 증가

기술의 진보와 스마트한 기능

도시화와 가처분소득 증가

업계의 잠재적 위험 및 과제

교환 사이클 연장

소비자의 가격 민감도

기회

신흥 시장 진출

스마트 홈 에코시스템의 성장

성장 가능성 분석

미래 시장 동향

기술과 혁신의 상황

현재 기술 동향

신흥 기술

가격 동향

지역별

제품별

규제 상황

표준 및 컴플라이언스 요건

지역 규제 틀

인증기준

무역 통계(HS코드 8418)

주요 수입국

주요 수출국

Porter's Five Forces 분석

PESTEL 분석

소비자 구매 행동 분석

구입 패턴

선호 분석

소비자 행동의 지역차

전자상거래가 구매결정에 미치는 영향

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

주요 동향

상단형 냉장고

하단형 냉장고

양문형 냉장고

프렌치 도어 냉장고

제6장 시장 추계 및 예측 : 용량별, 2021-2034년

주요 동향

15 입방피트 미만

16-30 입방 피트

30 입방피트 이상

제7장 시장 추계 및 예측 : 구조별, 2021-2034년

주요 동향

내장

자립형

카운터 뎁스

컴팩트 및 미니

양문형

기타(프렌치 도어, 탑 냉동고, 하단 냉장고 등)

제8장 시장 추계 및 예측 : 냉각 기술별, 2021-2034년

주요 동향

직냉

성에 제거

인버터 컴프레서

듀얼 증발기

열전

제9장 시장 추계 및 예측 : 스마트 기능별, 2021-2034년

주요 동향

Wi-Fi 대응

앱 제어

음성 어시스턴트 통합

기타(터치 스크린 디스플레이, 내장 카메라 등)

제10장 시장 추계 및 예측 : 마감별, 2021-2034년

스테인레스 스틸

매트 블랙

유리문

기타(레트로, 커스텀 등)

제11장 시장 추계 및 예측 : 가격대별, 2021-2034년

주요 동향

저

중

고

제12장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

주요 동향

주택용

상업용

제13장 시장 추계 및 예측 : 유통 채널별, 2021-2034년

주요 동향

온라인

전자상거래

기업 웹사이트

오프라인

백화점

하이퍼마켓 및 슈퍼마켓

전문 소매점

기타

제14장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제15장 기업 프로파일

Arcelik

BSH

Electrolux

Gree

Haier

Hisense

Hitachi

LG

Liebherr

Midea

Panasonic

Samsung

Sharp

Toshiba

Whirlpool

JHS

영문 목차

영문목차

The Global Household Refrigerators and Freezers Market was valued at USD 119.1 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 193.5 billion by 2034.

Increasing consumer awareness about environmental sustainability and rising electricity costs are fueling the demand for energy-efficient home appliances. Consumers are now prioritizing appliances that offer advanced energy-saving capabilities without compromising on performance. This trend is further strengthened by growing government initiatives and regulatory policies promoting eco-friendly products. Simultaneously, households are adopting smart technologies that provide greater control and convenience. Modern refrigerators now come equipped with features like touchscreen panels, virtual assistant compatibility, and wireless connectivity, which allow users to manage storage, monitor inventory, and access integrated services remotely. The merging of smart homes with connected appliances continues to reshape the market landscape, reflecting shifting preferences for comfort, efficiency, and real-time responsiveness.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$119.1 Billion

Forecast Value

$193.5 Billion

CAGR

5%

The top-mounted refrigerators segment generated USD 51.9 billion in 2024, maintaining its leading position in the market. These models, which place the freezer compartment above the main refrigerator section, remain popular for their affordability and space-saving design. Their lower price point makes them an ideal option for value-driven consumers across developed and emerging regions. Compactness, ease of use, and consistent performance continue to support their strong market presence.

The offline distribution channel segment held 78.4% share in 2024. In-store shopping allows buyers to physically inspect appliances, assess features, and make informed decisions with the guidance of trained sales staff. Consumers place significant value on personal assistance, immediate product demonstrations, and the added convenience of services such as delivery, installation, and maintenance, all of which are better facilitated through brick-and-mortar stores. This immersive, service-driven retail experience plays a major role in maintaining offline leadership in the appliance segment.

U.S. Household Refrigerators and Freezers Market held 74.9% share in 2024. Strong consumer purchasing power and a rising preference for premium, high-performance home appliances are driving adoption. The integration of intelligent home ecosystems is accelerating demand for refrigerators with smart features such as app control, energy monitoring, and digital interfaces. U.S. consumers are also highly responsive to innovations that align with sustainability goals, supporting the growth of energy-efficient models.

Major companies active in the Global Household Refrigerators and Freezers Market include Toshiba, Samsung, Whirlpool, Gree, Panasonic, LG, Midea, Haier, Arcelik, Liebherr, Hisense, BSH, Sharp, Hitachi, and Electrolux. Companies in the household refrigerators and freezers market are focusing on product innovation, sustainability, and digital integration to solidify their competitive position. Many brands are expanding their smart appliance portfolios by embedding IoT capabilities, AI-based inventory tracking, and mobile connectivity. To meet regulatory standards and consumer demand for eco-friendly solutions, manufacturers are enhancing energy efficiency through inverter technology and environmentally friendly refrigerants. Geographic expansion, particularly into emerging markets, is another core strategy, supported by localized production and retail partnerships.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Capacity

2.2.4 Structure

2.2.5 Cooling technology

2.2.6 Smart features

2.2.7 Finish

2.2.8 Price range

2.2.9 End use

2.2.10 Distribution channel

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising demand for energy-efficient appliances

3.2.1.2 Technological advancements and smart features

3.2.1.3 Increasing urbanization and disposable income