항공기용 사출 좌석 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Aircraft Ejection Seat Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1844269

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 180 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

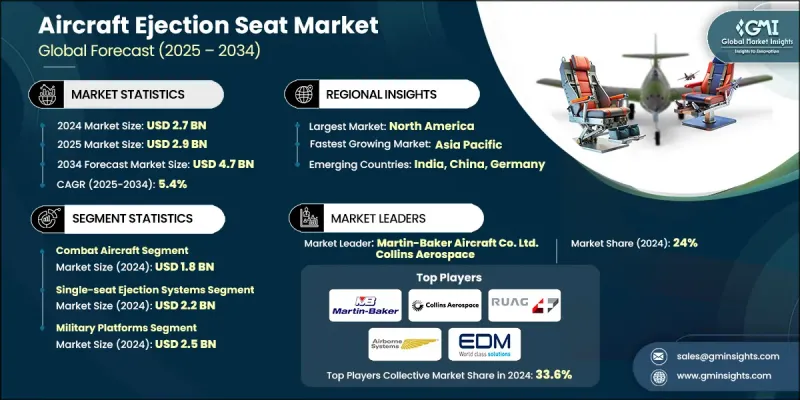

세계의 항공기용 사출 좌석 시장 규모는 2024년에 27억 달러로 평가되었고, CAGR 5.4%로 성장할 전망이며, 2034년에는 47억 달러에 이를 것으로 예측됩니다.

성장의 원동력은 전투기 조달 증가, 방위 항공기의 지속적인 업그레이드, 파일럿 생존 기술의 진보입니다. 세계의 방위 제조업체가 자급자족의 강화를 향하고 있는 가운데, 사출 좌석 시스템은 공전 안전 혁신의 초점이 되고 있습니다. 방위 기관이 파일럿의 안전성 향상과 고위험 시나리오에서의 미션 크리티컬한 생존성을 우선하는 가운데, 기술적으로 선진적이고 지능적인 사출 솔루션에 대한 수요가 증가하고 있습니다. 노후화된 기체의 급속한 근대화 구상 및 연명 프로그램은 후부에 대응한 차세대형 사출 좌석 수요를 한층 더 높이고 있습니다. 국방 관계자는 또한 빠른 탈출 타이밍을 최적화하고 부상 위험을 줄이기 위해 실시간 센서 입력을 갖춘 보다 스마트한 시스템을 통합하려고 합니다. 이러한 기술 혁신과 전략의 융합은 세계 사출 좌석 개발의 궤적을 형성하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

27억 달러

예측 금액

47억 달러

CAGR

5.4%

전투기 부문은 방위 예산 확대, 현대화 노력, 지정학적 불확실성 증가, 파일럿 보호 솔루션 업그레이드를 요구하는 세계적인 움직임에 힘입어 2024년 18억 달러를 창출했습니다. 스마트한 생체공학 및 구명 기술과 연동할 수 있는 보다 가볍고 모듈화된 신뢰성 있는 사출 좌석 시스템에 대한 관심이 높아지고 있습니다. 이러한 시스템은 신속한 배치 및 기체의 장수명화를 중시하는 군사 항공 프로그램에 필수적인 것이 되고 있습니다.

단좌기 부문은 2024년에 22억 달러를 창출했습니다. 단좌기 시스템 수요는 선진적인 최전선 제트기의 조달과 세계 전투기 플릿의 현대화를 향한 지속적인 노력과 밀접하게 연결되어 있습니다. 내구성이 강화되고 헬스 모니터링 기능이 통합된 보다 컴팩트하고 경량인 시스템 수요가 높아지고 있습니다. 이는 미래 전투기 플랫폼에 원활하게 통합될 수 있는 확장 가능한 사출 솔루션을 제공하며 임무의 즉각성과 생존성을 최적화하기 위한 광범위한 노력과 일치합니다.

미국의 항공기용 사출 좌석 시장 규모는 2024년 11억 달러에 이르렀으며, 견조한 국방 할당, 전략적 공군 업그레이드, 고급 사출 능력에 대한 투자 확대에 뒷받침되고 있습니다. 국내 제조업체는 항공기 호환성을 높이는 설계 혁신, 소재 경량화, AI 주도 의사 결정 시스템, 사출 후 지원 인프라 개선을 우선시하고 있습니다. 국내에서는 항공기의 근대화 구상이 확대되고 항공기 승무원의 보호가 중시되고 있는 것이 시장의 기세를 지속시키는 주요 요인이 되고 있습니다.

항공기용 사출 좌석 시장과 관련된 주요 기업은 Hindustan Aeronautics Limited, Collins Aerospace, AmSafe Bridport Ltd., Lockheed Martin, Northrop Grumman, Martin-Baker Aircraft Co. Ltd., Airborne Systems Inc., QinetiQ Group Plc, Parachute Laborator Inc., Quickstep Technologies, Tencate Advanced Armor, RUAG Group, Safran SA, EDM Limited, BAE Systems, Butler Parachute Systems Inc., Survival Equipment Services Ltd., Vector Aerospace, Cobham Plc, NPP Zvezda 등이 있습니다. 존재감을 높이기 위해, 각사는 사출 좌석의 경량화, 모듈러 설계, 센서 기반의 타이밍 시스템의 개량, 통합형 스마트 안전 기술에 주력하고 있습니다. 많은 기업들은 차세대 방위 기준을 준수하면서 노후화된 항공기 플랫폼을 지원하기 위해 개조 제품의 제공을 확대하고 있습니다. 공군과 OEM과의 전략적 제휴, 지속적인 연구개발 투자, 강력한 애프터마켓 서비스 능력을 통해 이들 기업은 경쟁력을 획득하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

전투기 조달 증가

배출 시스템의 기술적 개선

파일럿의 생존율 향상에 고도의 사출 시스템 필요

신흥 전투기 업그레이드 및 수명 연장 프로그램

방위에 있어서 자립 진행

제조업의 함정 및 과제

개발과 유지에 필요한 높은 비용

다양한 항공기와의 복잡한 통합

3.2.3. 시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥 기술

가격 동향

지역별

제품별

가격 전략

새로운 비즈니스 모델

컴플라이언스 요건

국방 예산 분석

세계 방위비의 동향

지역 방위 예산 배분

북미

유럽

아시아태평양

중동 및 아프리카

라틴아메리카

주요 방위 근대화 프로그램

예산 예측(2025-2034년)

업계의 성장에 미치는 영향

국가별 방위 예산

공급망의 탄력

지정학적 분석

인재 분석

디지털 변혁

합병, 인수 및 전략적 파트너십의 상황

위험 평가 및 관리

주요 계약 체결(2021-2024년)

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

시장 집중 분석

주요 기업의 경쟁 벤치마킹

재무 실적 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업의 넓이

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더들

과제자들

팔로워

틈새 기업

전략적 전망 매트릭스

주요 발전(2021-2024년)

합병 및 인수

파트너십 및 협업

기술적 진보

확대 및 투자 전략

지속가능성에 대한 노력

디지털 변혁의 대처

신흥기업 및 스타트업 기업 경쟁 구도

제5장 시장 추계 및 예측 : 기종별(2021-2034년)

주요 동향

전투기

연습기

기타

제6장 시장 추계 및 예측 : 좌석 유형별(2021-2034년)

주요 동향

단좌식 사출 시스템

트윈 시트 사출 시스템

제7장 시장 추계 및 예측 : 핏(2021-2034년)

주요 동향

LINE-FIT

개조

제8장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

로켓 모터 및 투석기 시스템

낙하산

캐노피 투기 시스템

기타

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

군사 플랫폼

연구기관

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제11장 기업 프로파일

세계 주요 기업

Martin-Baker Aircraft Co. Ltd.

Collins Aerospace

BAE Systems

Lockheed Martin

Northrop Grumman

지역별 주요 기업

북미

EDM Limited

AmSafe Bridport Ltd.

Quickstep Technologies

아시아태평양

Hindustan Aeronautics Limited

NPP Zvezda

Airborne Systems Inc.

유럽

RUAG Group

Safran SA

Cobham Plc

QinetiQ Group Plc

Tencate Advanced Armor

Vector Aerospace

Survival Equipment Services Ltd.

틈새 기업 및 유통업체

Butler Parachute Systems Inc.

Parachute Laboratories Inc.

AJY

영문 목차

영문목차

The Global Aircraft Ejection Seat Market was valued at USD 2.7 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 4.7 billion by 2034.

The growth is driven by rising fighter jet procurement, ongoing upgrades of defense aircraft fleets, and advancements in pilot survival technologies. As global defense manufacturers move toward greater self-sufficiency, ejection seat systems have become a focal point in air combat safety innovation. With defense agencies prioritizing enhanced safety for pilots and mission-critical survivability in high-risk scenarios, the demand for technologically advanced and intelligent ejection solutions is gaining momentum. Rapid modernization initiatives and life-extension programs for aging airframes are further amplifying demand for retrofit-compatible, next-generation ejection seats. Defense players are also incorporating smarter systems with real-time sensor inputs to optimize timing and reduce injury risk during high-speed ejections. This convergence of innovation and strategy continues to shape the trajectory of ejection seat development worldwide.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.7 Billion

Forecast Value

$4.7 Billion

CAGR

5.4%

The combat aircraft segment generated USD 1.8 billion in 2024, fueled by expanded defense budgets, modernization efforts, rising geopolitical uncertainty, and the global push for upgraded pilot protection solutions. There's rising interest in integrating lighter, modular, and more reliable ejection seat systems capable of interfacing with smart avionics and life-saving technologies. These systems are becoming integral to military aviation programs focused on rapid deployability and fleet longevity.

The single-seat segment generated USD 2.2 billion in 2024. Demand for single-seat systems is closely tied to the procurement of advanced frontline jets and sustained efforts to modernize global fighter fleets. The push for more compact, lightweight systems with enhanced durability and integrated health monitoring features is growing. This aligns with broader efforts to deliver scalable ejection solutions that can be seamlessly embedded into future fighter platforms, optimizing mission readiness and survivability.

U.S. Aircraft Ejection Seat Market reached USD 1.1 billion in 2024, supported by robust defense allocations, strategic air force upgrades, and growing investments in advanced ejection capabilities. Domestic manufacturers are prioritizing design innovations that enhance aircraft compatibility, material lightness, AI-driven decision systems, and improved post-ejection support infrastructure. The country's expanding fleet modernization initiatives and emphasis on aircrew protection remain key contributors to sustained market momentum.

Leading companies involved in Aircraft Ejection Seat Market include Hindustan Aeronautics Limited, Collins Aerospace, AmSafe Bridport Ltd., Lockheed Martin, Northrop Grumman, Martin-Baker Aircraft Co. Ltd., Airborne Systems Inc., QinetiQ Group Plc, Parachute Laboratories Inc., Quickstep Technologies, Tencate Advanced Armor, RUAG Group, Safran SA, EDM Limited, BAE Systems, Butler Parachute Systems Inc., Survival Equipment Services Ltd., Vector Aerospace, Cobham Plc, and NPP Zvezda. To strengthen their presence, companies are focusing on lighter, modular ejection seat designs, improved sensor-based timing systems, and integrated smart safety technologies. Many players are expanding their retrofit offerings to support aging aircraft platforms while ensuring compliance with next-generation defense standards. Strategic collaborations with air forces and OEMs, continuous R&D investments, and strong aftermarket service capabilities are enabling these firms to gain a competitive edge.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry snapshot

2.2 Key market trends

2.2.1 Aircraft type trends

2.2.2 Seat type trends

2.2.3 Fit trends

2.2.4 Component trends

2.2.5 End use trends

2.2.6 Regional

2.3 TAM Analysis, 2025-2034 (USD Billion)

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Increasing Fighter Aircraft Acquisition

3.2.1.2 Technological Improvements in Ejection Systems

3.2.1.3 Enhanced pilot survivability demands advanced ejection systems

3.2.1.4 Emerging Fighters Upgrade and Life Extension Programs

3.2.1.5 Increasingly Self-Reliant in Their Defense

3.2.2 Manufacturing Industry pitfalls and challenges

3.2.2.1 High cost to develop and maintain

3.2.2.2 Complex integration with various aircraft

3.2.3. Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product

3.9 Pricing strategies

3.10 Emerging business models

3.11 Compliance requirements

3.12 Defense budget analysis

3.13 Global defense spending trends

3.14 Regional defense budget allocation

3.14.1 North America

3.14.2 Europe

3.14.3 Asia Pacific

3.14.4 Middle East and Africa

3.14.5 Latin America

3.15 Key defense modernization programs

3.16 Budget forecast (2025-2034)

3.16.1 Impact on Industry Growth

3.16.2 Defense Budgets by Country

3.17 Supply chain resilience

3.18 Geopolitical analysis

3.19 Workforce analysis

3.20 Digital transformation

3.21 Mergers, acquisitions, and strategic partnerships landscape

3.22 Risk assessment and management

3.23 Major contract awards (2021-2024)

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.2.2 Market Concentration Analysis

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Sustainability initiatives

4.4.6 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Aircraft Type, 2021 - 2034 (USD Million & Units)

5.1 Key trends

5.2 Combat Aircraft

5.3 Training Aircraft

5.4 Others

Chapter 6 Market Estimates and Forecast, By Seat Type, 2021 - 2034 (USD Million & Units)

6.1 Key trends

6.2 Single-seat ejection systems

6.3 Twin-seat ejection systems

Chapter 7 Market Estimates and Forecast, By Fit, 2021 - 2034 (USD Million & Units)

7.1 Key trends

7.2 Line-fit

7.3 Retrofit

Chapter 8 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Million & Units)

8.1 Rocket motors / catapult systems

8.2 Parachutes

8.3 Canopy jettison systems

8.4 Others

Chapter 9 Market Estimates and Forecast, By End Use Application, 2021 - 2034 (USD Million & Units)

9.1 Military platforms

9.2 Research institutes

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Units)