정맥혈전색전증 치료 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Venous Thromboembolism Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1833655

리서치사:Global Market Insights Inc.

발행일:2025년 09월

페이지 정보:영문 145 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

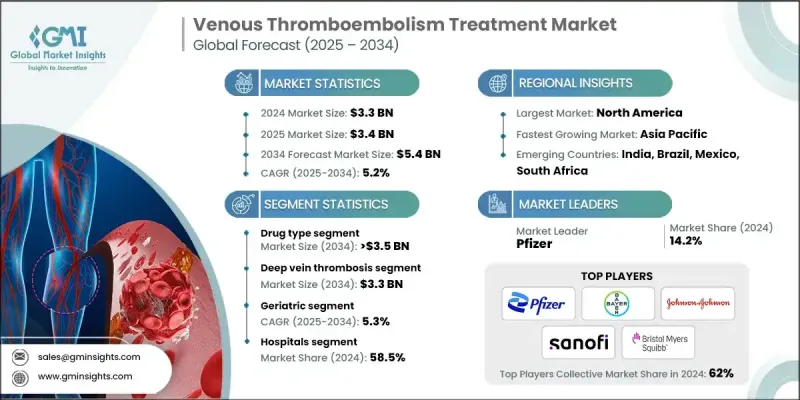

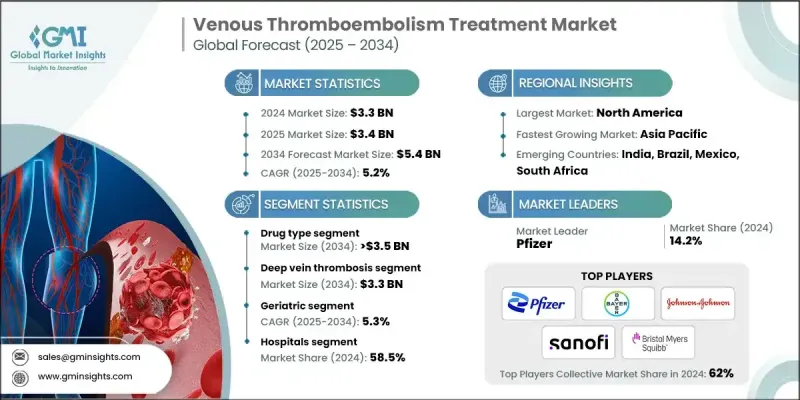

세계 정맥혈전색전증 치료 시장 규모는 2024년에 33억 달러로 평가되었으며, CAGR 5.2%로 성장하여 2034년에는 54억 달러에 달할 것으로 추정됩니다.

이러한 증가 추세는 전 세계적으로 VTE 발병률이 증가함에 따라 항응고제, 혈전용해 요법, 혈관 중재시술 장비에 대한 수요가 증가하고 있기 때문입니다. VTE 치료에는 정맥 내 혈전을 용해, 예방 및 관리하기 위해 특별히 고안된 약물 및 장치가 포함됩니다. 이러한 치료법은 연령, 면역 반응, 전신 건강 상태, 증상의 심각성 등 환자별 여러 요인에 따라 맞춤화됩니다. 치료받지 않은 VTE의 위험성에 대한 일반인과 전문가들의 인식 증가, 임상 현장에서의 예방 의료 프로토콜의 확대, 원격 항응고 모니터링을 위한 원격의료의 광범위한 사용은 시장 성장을 더욱 촉진하고 있습니다. 또한, 의약품 E-Commerce 플랫폼의 확산으로 경구용 치료제와 압박약에 대한 접근성이 향상되어 보다 신속하고 효과적인 개입이 가능해졌습니다. 교육, 진단, 디지털 케어 통합에 대한 지속적인 노력은 보다 적극적인 질병 관리를 지원하고, 환자의 예후를 개선하며, 병원과 재택 환경 모두에서 치료 솔루션의 채택을 확대할 수 있도록 돕습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034

시장 규모

33억 달러

예측 금액

54억 달러

CAGR

5.2%

최신 치료법은 의료 시스템의 VTE 관리 방식을 변화시키고 있으며, 환자의 안전성과 정확성, 편의성을 향상시키고 있습니다. 약물 제제와 혈전제거 도구의 기술적 발전은 치료의 정확도를 높이고 합병증을 억제하는 데 도움이 되고 있습니다. 더 오래 지속되는 경구용 항응고제, AI 유도 혈전제거 시스템, 덜 침습적인 혈관 기구의 개발로 환자의 치료 계획 준수율이 크게 향상되고 부작용이 최소화되고 있습니다. 이러한 기술 혁신은 표준 치료를 개선할 뿐만 아니라, 의사들이 보다 장기적인 결과를 가진 효율적인 치료를 제공할 수 있게 해줍니다.

2024년에는 약물 기반 부문이 65.5%의 점유율을 차지했으며, 임상 및 외래 환경에서 항응고제 및 혈전용해제의 광범위한 사용이 주도할 것으로 보입니다. 이 부문은 항응고제와 혈전용해제의 두 가지 주요 카테고리로 나뉩니다. 항응고제의 카테고리는 다시 직접 경구용 항응고제, 헤파린 제제, 비타민 K 길항제로 나뉩니다. 이러한 장점은 최신 항응고제가 예측 가능한 치료 효과를 제공하고, 활성 지속 시간이 길며, 집중적인 모니터링이 덜 필요하기 때문입니다. 이러한 특징은 특히 다양한 환자 환경에서 VTE의 초기 및 지속적 관리에 이상적인 항응고제입니다.

심부정맥혈전증(DVT) 분야는 2024년 20억 달러를 창출하고 2034년에는 33억 달러에 달해 전체 VTE 치료 시장에 가장 큰 기여를 할 것으로 예상됩니다. DVT는 주로 하지의 심부정맥에 혈전이 형성되는 것이 특징이며, 조속히 발견하고 치료하지 않으면 심각한 건강상의 위험을 초래할 수 있습니다. DVT의 유병률은 좌식 생활습관, 흡연, 고체중, 만성질환 등 여러 위험요인의 영향을 받습니다. 이러한 부담의 증가로 의료진은 조기 발견, 항응고 요법의 지도적 사용, 필요한 경우 기계적 중재에 중점을 두어 회복률을 높이고 생명을 위협하는 합병증을 줄이기 위해 노력하고 있습니다.

북미 정맥혈전색전증 치료 시장 점유율은 40.1%였습니다. 이 지역의 우위는 고도의 진단 자원, 숙련된 의료진, 환자의 높은 의식 수준 등 의료 체계가 잘 구축되어 있기 때문입니다. 예방과 증상 조기 발견에 중점을 둔 공중보건 캠페인은 VTE의 적시 치료에 기여하고 있으며, 연구 투자를 통해 새로운 제품과 신기술이 지속적으로 시장에 출시되고 있습니다. 북미에 기반을 둔 제약 및 의료 기술 기업들은 우수한 효능과 안전성을 제공하는 혁신적인 솔루션을 지속적으로 개발하여 이 지역의 시장 성과를 뒷받침하고 있습니다.

정맥혈전색전증 치료 시장을 적극적으로 형성하고 있는 주요 기업으로는 Johnson & Johnson, Philips Healthcare, Boehringer Ingelheim, Daiichi Sankyo, Sanofi, Novartis, AngioDynamics, Bayer, Argon Medical Products, Boston Scientific, Daesung Maref, Pfizer, Cardinal Health, Cook Medical, GlaxoSmithKline, Bristol Myers Squibb, and Covidien (Medtronic) 등이 있습니다. 정맥혈전색전증 치료 시장의 주요 기업들은 시장에서의 입지를 확고히 하기 위해 혁신, 전략적 파트너십, 지리적 확장을 결합하는 데 주력하고 있습니다. 보다 안전하고 효과적인 치료법을 제공하는 차세대 치료법과 기기를 출시하기 위해 많은 기업들이 조사개발에 많은 투자를 하고 있습니다. 학술 및 임상 기관과의 전략적 제휴를 통해 임상시험 및 기술 개발을 가속화하는 데 도움을 주고 있습니다. 또한, 각 기업들은 신흥시장 진출과 유통망 강화를 통해 세계 입지를 넓히고 접근성을 높이고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급업체 상황

각 단계에서의 부가가치

밸류체인에 영향을 미치는 요인

업계에 대한 영향요인

성장 촉진요인

정맥혈전색전증 유병률 증가

고령화와 이동 어려움

항응고 요법의 진보

혈전 후 증후군에 대한 의식 상승

업계의 잠재적 리스크와 과제

출혈성 합병증 리스크

개발도상 지역에서의 인식의 한계

시장 기회

이중 작용 요법 개발

원격의료 플랫폼 확대

성장 가능성 분석

규제 상황

북미

미국

캐나다

유럽

아시아태평양

향후 시장 동향

기술적 상황

현재 기술

신기술

특허 상황

파이프라인 분석

가격 분석

질병 역학

Porters 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

세계

북미

유럽

기업 매트릭스 분석

주요 시장 기업 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병

파트너십과 협업

신제품 발매

확장 계획

제5장 시장 추정과 예측 : 치료 종류별, 2021-2034

주요 동향

디바이스

압축 시스템

혈전제거 시스템

IVC 필터

스타킹

기타 디바이스

약제 종류

항응고제

직접 경구 항응고제

헤파린

비타민 K 길항제

혈전용해제

제6장 시장 추정과 예측 : 용도별, 2021-2034

주요 동향

심부정맥혈전증

폐색전증

제7장 시장 추정과 예측 : 연령별, 2021-2034

주요 동향

성인

노인

제8장 시장 추정과 예측 : 최종 용도별, 2021-2034

주요 동향

병원

카테터 검사실

외래 수술 센터(ASC)

기타 용도

제9장 시장 추정과 예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제10장 기업 개요

AngioDynamics

Argon Medical Products

Bayer

Boehringer Ingelheim

Boston Scientific

Bristol Myers Squibb

Cardinal Health

Cook Medical

Covidien(Medtronic)

Daesung Maref

Daiichi Sankyo

GlaxoSmithKline

Johnson &Johnson

Novartis

Pfizer

Philips Healthcare

Sanofi

목차

제11장 조사 방법과 범위

제12장 주요 요약

제13장 업계 인사이트

생태계 분석

공급업체 상황

각 단계에서의 부가가치

밸류체인에 영향을 미치는 요인

업계에 대한 영향요인

성장 촉진요인

정맥혈전색전증 유병률 증가

고령화와 이동 어려움

항응고 요법의 진보

혈전 후 증후군에 대한 의식 상승

업계의 잠재적 리스크와 과제

출혈성 합병증 리스크

개발도상 지역에서의 인식의 한계

시장 기회

이중 작용 요법 개발

원격의료 플랫폼 확대

성장 가능성 분석

규제 상황

북미

미국

캐나다

유럽

아시아태평양

향후 시장 동향

기술적 상황

현재 기술

신기술

특허 상황

파이프라인 분석

가격 분석

질병 역학

Porters 분석

PESTEL 분석

제14장 경쟁 구도

소개

기업의 시장 점유율 분석

세계

북미

유럽

기업 매트릭스 분석

주요 시장 기업 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

인수합병

파트너십과 협업

신제품 발매

확장 계획

제15장 시장 추정과 예측 : 치료 종류별, 2021-2034

주요 동향

디바이스

압축 시스템

혈전제거 시스템

IVC 필터

스타킹

기타 디바이스

약제 종류

항응고제

직접 경구 항응고제

헤파린

비타민 K 길항제

혈전용해제

제16장 시장 추정과 예측 : 용도별, 2021-2034

주요 동향

심부정맥혈전증

폐색전증

제17장 시장 추정과 예측 : 연령별, 2021-2034

주요 동향

성인

노인

제18장 시장 추정과 예측 : 최종 용도별, 2021-2034

주요 동향

병원

카테터 검사실

외래 수술 센터(ASC)

기타 용도

제19장 시장 추정과 예측 : 지역별, 2021-2034

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트

제20장 기업 개요

AngioDynamics

Argon Medical Products

Bayer

Boehringer Ingelheim

Boston Scientific

Bristol Myers Squibb

Cardinal Health

Cook Medical

Covidien(Medtronic)

Daesung Maref

Daiichi Sankyo

GlaxoSmithKline

Johnson &Johnson

Novartis

Pfizer

Philips Healthcare

Sanofi

KSM

영문 목차

영문목차

The Global Venous Thromboembolism Treatment Market was valued at USD 3.3 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 5.4 billion by 2034.

The upward trend is driven by the growing incidence of VTE conditions globally, which has heightened demand for anticoagulant medications, thrombolytic therapies, and vascular intervention devices. VTE treatment includes a targeted group of drugs and devices that are specifically designed to dissolve, prevent, or manage blood clots within the venous system. These therapies are customized based on multiple patient-specific factors, including age, immune response, overall health, and the severity of the condition. The market growth is further fueled by increased public and professional awareness about the dangers of untreated VTE, the expansion of preventive care protocols in clinical settings, and the broader use of telemedicine for remote anticoagulant monitoring. Additionally, the widespread availability of pharmaceutical e-commerce platforms has improved access to both oral treatments and compression products, promoting earlier and more effective intervention. The continued focus on education, diagnostics, and digital care integration is supporting more proactive management of the condition, leading to improved patient outcomes and increased adoption of therapeutic solutions across both hospital and home settings.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$3.3 Billion

Forecast Value

$5.4 Billion

CAGR

5.2%

Modern treatment options are transforming how healthcare systems manage VTE, offering greater safety, accuracy, and convenience for patients. Technological progress in drug formulation and clot-removal tools is helping enhance therapeutic precision and limit complications. The development of longer-acting oral anticoagulants, AI-guided clot retrieval systems, and less invasive vascular devices is significantly improving patient adherence to treatment plans and minimizing adverse reactions. These innovations are not only improving the standard of care but also enabling physicians to deliver efficient treatment with better long-term outcomes.

In 2024, the drug-based segment held a 65.5% share, driven by the wide-scale use of anticoagulants and thrombolytic drugs across both clinical and outpatient environments. This segment is divided into two main categories: anticoagulants and thrombolytics. The anticoagulant category is further segmented into direct oral anticoagulants, heparin products, and vitamin K antagonists. This dominance is the result of modern anticoagulants offering predictable therapeutic effects, longer activity durations, and requiring less intensive monitoring. These features make them ideal for both initial and ongoing management of VTE, especially in varied patient settings.

The deep vein thrombosis (DVT) segment generated USD 2 billion in 2024 and will reach USD 3.3 billion by 2034, making it the largest contributor to the overall VTE treatment market. DVT is characterized by clot formation in deep veins, primarily in the lower limbs, and poses serious health risks if not identified and treated promptly. The prevalence of DVT is influenced by multiple risk factors such as sedentary lifestyles, smoking, high body weight, and chronic illnesses. This increasing burden has prompted medical professionals to emphasize early detection, guided use of anticoagulant therapy, and, where necessary, mechanical interventions to improve recovery rates and reduce life-threatening complications.

North America Venous Thromboembolism Treatment Market held a 40.1% share. The dominance of this region stems from its well-established healthcare framework, including advanced diagnostic resources, skilled healthcare personnel, and high patient awareness levels. Public health campaigns focused on prevention and early symptom recognition have contributed to the timely treatment of VTE, while research investments continue to bring new products and technologies to the market. Pharmaceutical and medical technology companies based in North America are consistently developing innovative solutions that offer superior efficacy and safety, which support the region's strong market performance.

Prominent companies actively shaping the venous thromboembolism treatment market include Johnson & Johnson, Philips Healthcare, Boehringer Ingelheim, Daiichi Sankyo, Sanofi, Novartis, AngioDynamics, Bayer, Argon Medical Products, Boston Scientific, Daesung Maref, Pfizer, Cardinal Health, Cook Medical, GlaxoSmithKline, Bristol Myers Squibb, and Covidien (Medtronic). Leading players in the venous thromboembolism treatment market are focusing on a blend of innovation, strategic partnerships, and geographic expansion to solidify their market standing. Many are investing heavily in R&D to launch next-generation therapies and devices that provide safer, more effective treatment options. Strategic collaborations with academic and clinical institutions are helping accelerate clinical trials and technology development. Companies are also expanding their global footprint by entering emerging markets and strengthening distribution networks to improve access.