가솔린 직분사 시스템 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Gasoline Direct Injection (GDI) System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1822654

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 178 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

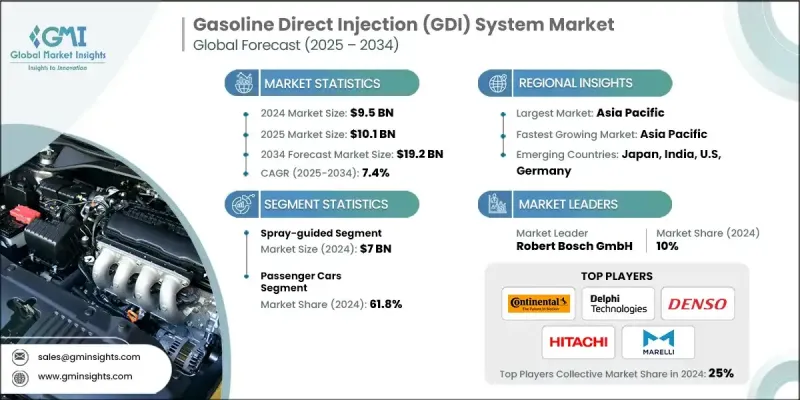

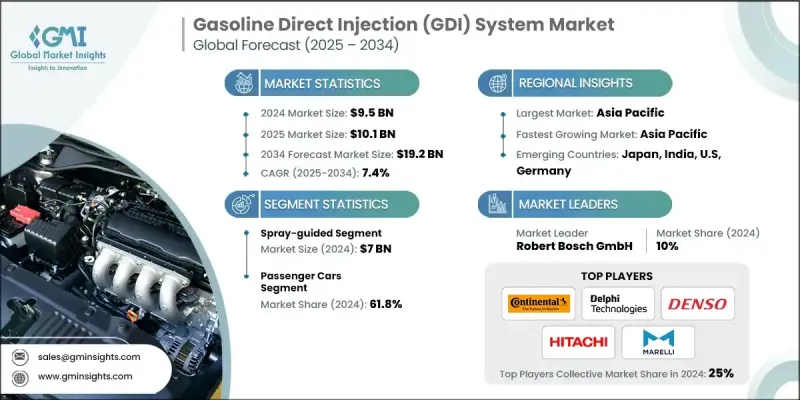

세계의 가솔린 직분사(GDI) 시스템 시장은 2024년에 95억 달러로 평가되었고, GDI 기술의 지속적인 혁신과 고성능 차량에 대한 소비자 선호도 증가로 CAGR은 7.4%를 나타낼 것으로 예측되며 2034년에 192억 달러로 성장할 전망입니다. 향상된 연료 인젝터 및 개선된 연소 제어를 포함한 GDI 시스템의 고급 발전은 엔진 효율성과 성능을 더욱 높이고 있습니다. 동시에 소비자들은 우수한 출력, 반응성 및 연비를 제공하는 차량을 점점 더 우선시하고 있습니다. 이러한 고성능 효율 차량에 대한 수요 증가는 GDI 시스템 채택을 촉진하고 있습니다. 2024년 1월, GB 리매뉴팩처링(GB Remanufacturing, Inc.)은 씰 키트, 멀티팩, 인젝터, 프리미엄 씰 교체 공구 키트 등을 포함한 17종의 신규 부품을 도입하며 가솔린 직접 분사(GDI) 프로그램을 강화했습니다. 이는 업계가 GDI 시스템 유지보수 및 업그레이드에 점점 더 중점을 두고 있음을 보여줍니다.

가솔린 직분사 시스템 산업 점유율은 컴포넌트, 용도, 지역별로 부문별로 세분화됩니다. 2032년까지 연료 인젝터 부문은 엔진 성능과 연비를 향상시키는 데 핵심적인 역할을 수행함에 따라 상당한 성장이 예상됩니다. 연료 인젝터는 연소실로 정밀한 연료 공급을 보장하여 연소 제어 개선과 배출가스 최소화를 이끌어냅니다. 자동차 제조사들이 엄격한 연비 및 배출 기준을 준수하기 위해 GDI 기술로 점점 더 전환함에 따라 고급 연료 인젝터에 대한 수요가 증가하고 있습니다. 상용차 부문은 중장비 용도에서 연비 효율이 높고 고성능 엔진에 대한 수요가 촉진됨에 따라 GDI 시스템 산업에 상당한 성장 기회를 제공할 전망입니다. 향상된 연비와 낮은 배출 가스로 유명한 GDI 시스템은 강력한 엔진이 필요하면서도 엄격한 환경 기준을 준수해야 하는 상용차에 완벽하게 부합합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

95억 달러

예측 금액

192억 달러

CAGR

7.4%

세계의 물류 및 운송 부문이 확대됨에 따라 상용차의 첨단 엔진 기술 도입이 가속화되며 GDI 시스템 채택이 확대되고 있습니다. 2032년까지 아시아태평양 가솔린 직분사 시스템 시장은 해당 지역의 번성하는 자동차 산업과 연비 효율 차량에 대한 수요 증가에 힘입어 상당한 점유율을 유지할 것으로 예상됩니다. 이 성장은 주요 자동차 제조업체의 입지와 최신기술 엔진 기술의 신속한 도입에 의해 촉진됩니다. 또한 연비 효율과 배출량 감소를 장려하는 정부 정책이 GDI 시스템 채택을 더욱 촉진합니다. 견고한 제조 기반과 빠른 기술적 발전을 바탕으로 아시아태평양 지역은 전 세계 가솔린 직분사(GDI) 시스템 시장에서 핵심적인 업체로 자리매김하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

업계에 미치는 영향요인

성장 촉진요인

에너지 효율적이고 고성능 차량의 점진적 채택

엄격한 배출규제

기술적 진보

업계의 잠재적 위험 및 과제

탄소 축적 우려

배출가스 우려

기회

고급 제어 시스템 통합

대체 연료와의 호환성

성장 가능성 분석

장래 시장 동향

기술과 혁신 상황

현재 기술 동향

신흥 기술

가격 동향

지역별

유형별

규제 상황

표준 및 규제 준수 요건

지역 규제 프레임워크

인증 기준

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

주요 동향

벽 유도

스프레이 유도

제6장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

주요 동향

연료 펌프

연료 인젝터

전자 제어 장치

연료 레일

기타

제7장 시장 추계 및 예측 : 차종별(2021-2034년)

주요 동향

기존 가솔린 자동차

하이브리드 자동차

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

승용차

소형 상용차

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제10장 기업 프로파일

Aisin Seiki Co Ltd

BorgWarner Inc

Continental AG

Delphi Technologies

Denso

Hitachi

Infineon Technologies AG

Keihin Corporation

Marelli

Park Ohio Holdings Corp

PHINIA

Robert Bosch GmbH

Stanadyne LLC

Standard Ignition

TI Fluid Systems

HBR

영문 목차

영문목차

The Global Gasoline Direct Injection (GDI) System Market was valued at USD 9.5 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 19.2 billion by 2034 driven by continuous innovations in GDI technology and rising consumer preference for high-performance vehicles. Advancements in GDI systems, such as enhanced fuel injectors and improved combustion control, are driving greater engine efficiency and performance. Concurrently, consumers are increasingly prioritizing vehicles that deliver superior power, responsiveness, and fuel economy. This heightened demand for high-performance, efficient vehicles is propelling the adoption of GDI systems. In January 2024, GB Remanufacturing, Inc. bolstered its Gasoline Direct Injection program by introducing 17 new parts, including seal kits, multi-packs, injectors, and a premium seal replacement tool kit. This move underscores the industry's growing emphasis on maintaining and upgrading GDI systems.

The gasoline direct injection system industry share is segmented by component, application, and region. By 2032, the fuel injectors segment is poised for significant growth, thanks to their pivotal role in enhancing engine performance and fuel efficiency. Fuel injectors ensure precise fuel delivery into the combustion chamber, leading to better combustion control and minimized emissions. With automakers increasingly turning to GDI technology to adhere to stringent fuel efficiency and emission standards, the demand for advanced fuel injectors is on the rise. The commercial vehicle segment is set to offer substantial gains to the GDI system industry, driven by the escalating demand for fuel-efficient, high-performance engines in heavy-duty applications. GDI systems, known for their enhanced fuel economy and lower emissions, are perfectly suited for commercial vehicles that need robust engines while adhering to strict environmental standards.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$9.5 Billion

Forecast Value

$19.2 Billion

CAGR

7.4%

As global logistics and transportation sectors expand, the push for advanced engine technologies in commercial vehicles amplifies the adoption of GDI systems. Through 2032, the Asia Pacific gasoline direct injection system market is expected to maintain a significant share, fueled by the region's thriving automotive sector and a growing appetite for fuel-efficient vehicles. The growth is driven by the presence of major automotive manufacturers and the swift adoption of cutting-edge engine technologies. Additionally, government initiatives championing fuel efficiency and emissions reduction further catalyze the uptake of GDI systems. With its robust manufacturing foundation and rapid technological advancements, Asia Pacific stands as a pivotal player in the global gasoline direct injection (GDI) system arena.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Type

2.2.3 Component

2.2.4 Vehicle type

2.2.5 Application

2.3 CXO perspectives: Strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing adoption of energy-efficient and high-performance vehicles

3.2.1.2 Stringent emission regulations

3.2.1.3 Technological advancements

3.2.2 Industry pitfalls & challenges

3.2.2.1 Carbon buildup concerns

3.2.2.2 Emission concerns

3.2.3 Opportunities

3.2.3.1 Integration of advanced control systems

3.2.3.2 Compatibility with alternative fuels

3.3 Growth potential analysis

3.4 Future market trends

3.5 Technology and innovation landscape

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.6 Price trends

3.6.1 By region

3.6.2 By type

3.7 Regulatory landscape

3.7.1 Standards and compliance requirements

3.7.2 Regional regulatory frameworks

3.7.3 Certification standards

3.8 Porter's analysis

3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East and Africa

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Units)

5.1 Key trends

5.2 Wall-guided

5.3 Spray-guided

Chapter 6 Market Estimates and Forecast, By Component, 2021 - 2034 (USD Billion) (Units)

6.1 Key trends

6.2 Fuel pump

6.3 Fuel injector

6.4 Electronic control unit

6.5 Fuel rail

6.6 Others

Chapter 7 Market Estimates and Forecast, By Vehicle Type, 2021 - 2034 (USD Billion) (Units)

7.1 Key trends

7.2 Conventional gasoline-powered vehicles

7.3 Hybrid vehicles

Chapter 8 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Units)

8.1 Key trends

8.2 Passenger cars

8.3 Light commercial vehicles

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Units)