District Heating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1822621

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 135 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

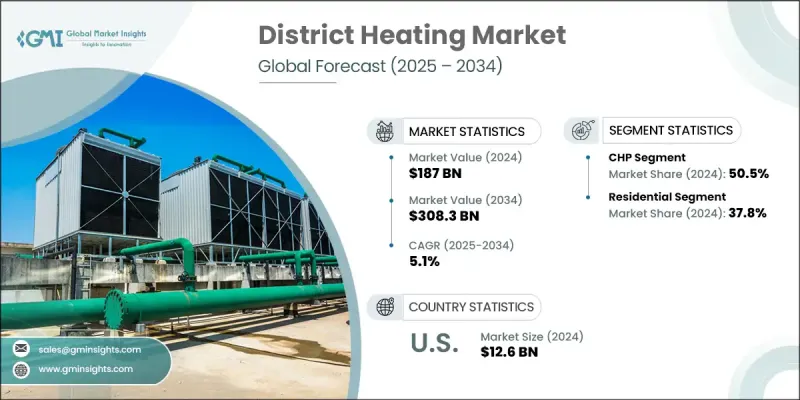

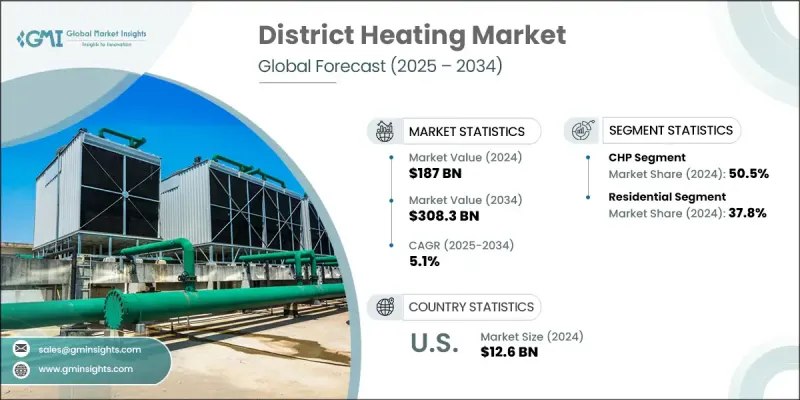

세계의 지역 난방 시장 규모는 2024년에 1,870억 달러로 평가되었고, CAGR은 5.1%를 나타낼 것으로 예측되며 2034년에 3,083억 달러에 이를 전망입니다. 변동성이 큰 화석 연료에 의존하는 개별 난방 시스템과 달리, 지역난방 네트워크는 가격 변동과 공급 차질에 덜 취약합니다. 열 생산 및 배급에 중앙 집중식 접근 방식을 활용함으로써, 이러한 시스템은 주거, 상업 및 산업 사용자에게 일관된 에너지 가용성을 보장합니다. 이러한 회복력은 화석 연료 의존도를 낮추고 탄소 배출을 감소시켜 경제적 안정성을 촉진하고 지속가능성 목표를 지원합니다. 이를 위해 2024년 6월, Hewlett Packard Enterprise와 Danfoss는 데이터 센터 에너지 사용량 감축을 위해 협력했습니다. 이들의 모듈식 설계는 열 포집 시스템을 통합하여 에지에서 AI 및 컴퓨팅 작업을 가속화하는 동시에, 잉여 열은 외부에서 재사용됩니다. 이는 에너지 관련 위험을 완화하고 미래를 위한 더 탄력적인 에너지 인프라를 구축하려는 글로벌 노력과 부합합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

1,870억 달러

예측 금액

3,083억 달러

CAGR

5.1%

주거 부문은 도시화 증가와 인구 밀집 지역의 효율적이고 지속 가능한 난방 솔루션 수요로 인해 2032년까지 지역 난방 시장에서 상당한 점유율을 차지할 것입니다. 주택 소유자들은 에너지 비용과 탄소 발자국을 줄이기 위한 친환경 옵션을 모색하고 있습니다. 지역난방 시스템은 개별 보일러와 유지보수의 필요성을 없애고 안정적이고 편리한 난방원을 제공합니다. 또한 에너지 효율적인 건물을 장려하는 정부 인센티브와 규제는 신규 주거 단지에서 지역난방 채택을 촉진하고 있습니다. 유럽 지역난방 시장은 탄소 배출 감축과 기후 목표 달성에 대한 의지로 인해 예측 기간 동안 주목할 만한 CAGR을 보일 것입니다. 유럽 국가들은 재생 에너지원과 첨단 난방 인프라에 막대한 투자를 진행 중입니다. 도시화와 노후 난방 시스템의 현대화는 보다 효율적인 중앙 집중식 솔루션에 대한 수요를 급증시키고 있습니다. 더불어 유럽연합(EU) 정책과 자금 지원은 지속 가능한 지역난방 네트워크 개발을 뒷받침하며, 공공 및 민간 부문이 에너지 효율성 향상과 환경 영향 감소를 위해 이러한 시스템을 채택하도록 장려하고 있습니다. 이러한 요소들은 지역 산업 성장을 견인할 것입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

주요 공급자 및 기술 공급자

물류, 유통, 서비스

규제 상황

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 위험 및 과제

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

지역 난방의 비용 구조 분석

가격 동향 분석

지역별

출처별

장래 시장 전망과 새로운 기회

미래 지역 난방 및 냉각 솔루션 개발

INDIGO

FLEXYNETS

E2District

InDeal

사례 연구 분석 - 스톡홀름 통합 DHC 시스템

프로젝트 개요

주요 사실 및 수치

고객 세분화

DHC 지원 정책 및 인센티브

지역 난방 시스템의 기술적 및 운영상의 파라미터

고객과 최종 용도의 분석

주거, 산업, 상업 부문에서의 채택

도시와 농촌의 침투

수요 동향과 소비 패턴

제4장 경쟁 구도

소개

기업의 시장 점유율 분석 : 지역별(2024년)

북미

유럽

아시아태평양

전략적 대시보드

전략적 노력

주요 M&A 활동

주요 파트너십 및 협업

제품의 혁신과 발매

시장 확대 전략

경쟁 벤치마킹

혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 출처별(2021-2034년)

주요 동향

CHP

지열

태양열

난방 전용 보일러

기타

제6장 시장 규모와 예측 : 용도별(2021-2034년)

주요 동향

주거용

상업용

대학

사무실

정부/군

기타

산업

화학

정유

제지

기타

제7장 시장 규모와 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

폴란드

러시아

스웨덴

핀란드

이탈리아

덴마크

영국

슬로바키아

오스트리아

체코 공화국

프랑스

아시아태평양

중국

일본

한국

제8장 기업 프로파일

A2A SpA

Alfa Laval

Antin Infrastructure Partners

BEW Berlin Energy and Heat

CenTrio

Cordia

Danfoss

E.ON

EDF

EnBW Energie Baden-Wurttemberg

ENGIE

Fortum

Goteborg Energi

Hafslund

Iren SpA

Kelag Energie & Warme

Keppel

Korea District Heating

LOGSTOR Denmark Holding

Nevel

Ørsted

Ramboll

RWE

Shinryo Corporation

Statkraft

STEAG

Vattenfall

Veolia

HBR

영문 목차

영문목차

The Global District Heating Market was valued at USD 187 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 308.3 billion by 2034, ushered by enhancing energy security by providing a stable energy supply. Unlike individual heating systems reliant on volatile fossil fuels, district heating networks are less susceptible to price fluctuations and supply disruptions. By utilizing a centralized approach to heat production and distribution, these systems ensure consistent energy availability for residential, commercial, and industrial users. This resilience promotes economic stability and supports sustainability goals by reducing reliance on fossil fuels and lowering carbon emissions. To that end, in June 2024, Hewlett Packard Enterprise and Danfoss joined forces to reduce data center energy usage. Their modular design integrates heat capture systems to accelerate AI and compute tasks at the edge, while excess heat is reused externally. It aligns with global efforts to mitigate energy-related risks and build more resilient energy infrastructures for the future.

The overall district heating market is categorized based on application, source, and region. The geothermal segment will record a promising CAGR through 2032, due to its increasing recognition as a sustainable and reliable heat source. Geothermal energy provides a consistent and renewable supply of heat, reducing dependency on fossil fuels and minimizing GHG emissions. Additionally, technological advancements have made geothermal extraction more efficient and cost-effective, encouraging its integration into district heating systems. Governments and environmental policies also support geothermal adoption for district heating applications, adding to segment growth.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$187 Billion

Forecast Value

$308.3 Billion

CAGR

5.1%

The residential segment will acquire a remarkable district heating market share by 2032, owing to growing urbanization and the need for efficient, sustainable heating solutions in densely populated areas. Homeowners are seeking eco-friendly options to reduce energy costs and carbon footprints. District heating systems provide a reliable and convenient heating source, eliminating the need for individual boilers and maintenance. Additionally, government incentives and regulations promoting energy-efficient buildings are ushering in the adoption of district heating in new residential developments. Europe district heating market will infer a notable CAGR during the forecast period, because of the commitment to reducing carbon emissions and achieving climate goals. European countries are investing heavily in renewable energy sources and advanced heating infrastructure. Urbanization and the modernization of aging heating systems catapult the need for more efficient, centralized solutions. Additionally, European Union policies and funding support the development of sustainable district heating networks, encouraging public and private sectors to adopt these systems for improved energy efficiency and environmental impact reduction. These factors will bolster the regional industry growth.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.1.3 Base estimates and calculations

1.1.4 Base year calculation

1.1.5 Key trends for market estimates

1.2 Forecast model

1.3 Primary research and validation

1.4 Some of the primary sources (but not limited to)

1.5 Data mining sources

1.5.1 Secondary

1.5.1.1 Paid sources

1.5.1.2 Public sources

1.5.1.3 Sources, by region

1.6 Market definitions

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Business trends

2.3 Source trends

2.4 Application trends

2.5 Regional trends

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Key suppliers and technology providers

3.1.2 Logistics, distribution, and services

3.2 Regulatory landscape

3.3 Industry impact forces

3.3.1 Growth drivers

3.3.2 Industry pitfalls & challenges

3.4 Growth potential analysis

3.5 Porter's analysis

3.5.1 Bargaining power of suppliers

3.5.2 Bargaining power of buyers

3.5.3 Threat of new entrants

3.5.4 Threat of substitutes

3.6 PESTEL analysis

3.6.1 Political factors

3.6.2 Economic factors

3.6.3 Social factors

3.6.4 Technological factors

3.6.5 Legal factors

3.6.6 Environmental factors

3.7 Cost structure analysis of district heating

3.8 Price trend analysis

3.8.1 By region

3.8.2 By source

3.9 Future market outlook & emerging opportunities

3.10 Development of future district heating & cooling solutions

3.10.1 INDIGO

3.10.2 FLEXYNETS

3.10.3 E2District

3.10.4 InDeal

3.11 Case study analysis - Integrated DHC system in Stockholm

3.11.1 Project overview

3.11.2 Key facts & figures

3.11.3 Customer segmentation

3.11.4 Policies & incentives supporting the DHC

3.12 Technical and operational parameters of district heating systems

3.13 Customer & End Use analysis

3.13.1 Adoption by residential, industrial, and commercial sectors

3.13.2 Urban vs rural penetration

3.13.3 Demand trends and consumption patterns

Chapter 4 Competitive Landscape, 2025

4.1 Introduction

4.2 Company market share analysis, by region 2024

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.3 Strategic dashboard

4.4 Strategic initiatives

4.4.1 Major M&A activities

4.4.2 Key partnerships and collaborations

4.4.3 Product innovations and launches

4.4.4 Market expansion strategies

4.5 Competitive benchmarking

4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Source, 2021 - 2034 (USD Billion & PJ)

5.1 Key trends

5.2 CHP

5.3 Geothermal

5.4 Solar

5.5 Heat only boiler

5.6 Others

Chapter 6 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion & PJ)

6.1 Key trends

6.2 Residential

6.3 Commercial

6.3.1 College/university

6.3.2 Office

6.3.3 Government/military

6.3.4 Others

6.4 Industrial

6.4.1 Chemical

6.4.2 Refinery

6.4.3 Paper

6.4.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion & PJ)