에너지 고밀도 재료 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Energy Dense Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801877

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 210 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

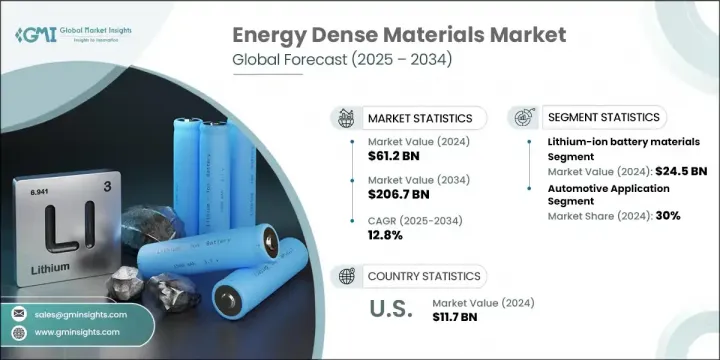

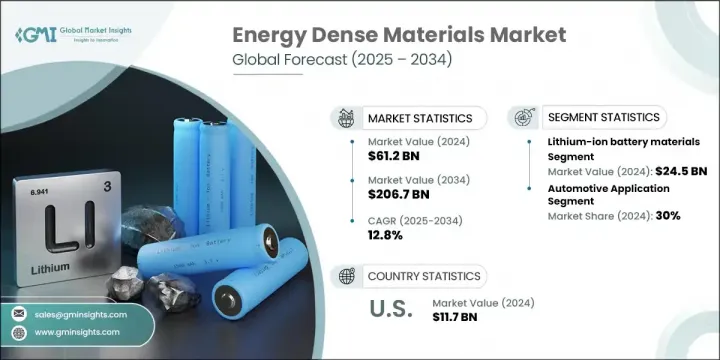

세계의 에너지 고밀도 재료 시장은 2024년에 612억 달러로 평가되었고, CAGR 12.8%로 성장하여 2034년에는 2,067억 달러에 이를 것으로 추정되고 있습니다.

이 시장은 탄소 감축에 대한 절박함과 보다 지속 가능하고 전기화된 에너지 시스템으로의 전환으로 인해 강력한 모멘텀을 보이고 있습니다. 재생에너지 발전이 계속 견인력을 발휘하는 가운데, 소형 고효율 에너지 저장 솔루션에 대한 수요가 점점 더 중요해지고 있습니다. 에너지 고밀도 재료는 전력망의 안정성을 보장하고, 피크 시간대 공급 균형을 조정하고, 간헐적인 전원으로부터의 전력 공급의 일관성을 개선함으로써 이러한 전환을 지원합니다. 효율적이고 가볍고 대용량의 에너지 저장에 대한 세계 수요가 증가함에 따라 다양한 분야에서 그 중요성이 커지고 있습니다.

전기 모빌리티의 부상은 시장 성장의 주요 요인 중 하나입니다. 전기자동차가 세계 시장에서 빠르게 확대됨에 따라 주행거리 연장, 급속 충전, 경량화를 실현하는 배터리의 필요성이 대두되고 있습니다. 에너지 고밀도 소재는 또한 전기 항공기와 드론을 위한 항공우주 추진 시스템에서도 중요한 역할을 하고 있으며, 단위 질량당 에너지를 극대화하여 비행 시간 연장 및 페이로드 용량을 향상시켜 궁극적으로 항공 운송 기술 전반의 혁신을 촉진합니다.

시장 범위

개시 연도

2024년

예측 연도

2025-2034년

개시 금액

612억 달러

예측 금액

2,067억 달러

CAGR

12.8%

2024년, 리튬 이온 배터리 재료 부문은 245억 달러의 수익을 창출했습니다. 리튬이온전지의 보급은 연료전지 소재, 슈퍼커패시터, 고체전지 등 다른 대안에 비해 에너지 밀도가 우수하기 때문입니다. 리튬 이온 배터리는 작고 가벼운 형태로 큰 에너지를 저장할 수 있어 휴대용 전자기기, 전기자동차, 대규모 에너지 저장 시스템에 최적의 솔루션이 되고 있습니다. 강력한 출력, 긴 수명, 안정적인 성능으로 인해 리튬 이온 배터리는 현대 에너지 저장의 기초 기술이 되었으며, 가전제품에서 유틸리티 규모의 그리드 스토리지에 이르기까지 광범위한 산업에서 급속한 보급을 지원하고 있습니다.

2024년 가장 큰 점유율을 차지한 분야는 자동차 분야로 30%의 점유율을 차지할 것으로 예측됩니다. 이러한 용도는 더 멀리 주행하고, 더 빨리 충전하며, 기존 엔진 성능에 필적하는 자동차에 대한 수요 증가에 힘입어 에너지 밀도가 높은 재료 기술 혁신의 중심이 되고 있습니다. 단위 면적당, 무게당 에너지 밀도를 높이는 배터리 기술은 소비자의 항속거리에 대한 우려를 해소하고 EV의 보급을 뒷받침합니다. 자동차 산업이 지속적으로 확대되는 가운데, 자동차 산업은 시장 성장의 중요한 원동력이 되고 있습니다.

미국의 에너지 고밀도 재료 시장은 2024년 117억 달러에 달할 것으로 예상되며, 2034년까지 연평균 13%의 성장률을 보일 것으로 전망됩니다. 꾸준한 경제 성장, 에너지 수요 증가, 산업 성장에 따라 미국에서는 효율적인 배터리, 자석, 연료전지 부품에 대한 수요가 증가하고 있습니다. 에너지 고밀도 재료는 산업계가 에너지 사용을 최적화하고 비용을 절감하며 전체 시스템 성능을 향상시키는 데 도움이 되고 있습니다. 에너지 저장 및 변환에 있어 에너지 저장과 변환의 역할은 부문을 불문하고 보다 견고하고 효율적인 에너지 인프라를 구축하는 데 필수적인 역할을 하고 있습니다.

에너지 고밀도 소재 세계 시장에서 사업을 전개하고 있는 주요 기업으로는 LG Energy Solution, Panasonic Corporation, Samsung SDI Co. 세계 에너지 고밀도 소재 시장에서 골격을 굳히기 위해 주요 기업들은 몇 가지 전략적 우선순위에 집중하고 있습니다. 여기에는 에너지 밀도, 안전성, 수명주기를 개선하는 첨단 화학물질 연구개발에 대한 적극적인 투자가 포함됩니다. 각 업체들은 특히 주요 성장 지역의 전기차 및 그리드 수요 증가에 대응하기 위해 생산 능력을 확장하고 있습니다. 자동차 제조업체 및 에너지 공급업체와의 전략적 제휴는 장기 계약을 확보하는 데 도움이 되고 있습니다. 또한, 기업들은 제품 포트폴리오를 다양화하여 솔리드 스테이트 기술 및 리튬 황 기술과 같은 차세대 재료를 포함하는 동시에 비용 효율성과 안정성을 위해 세계 공급망을 최적화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 인사이트

생태계 분석

공급업체 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 미치는 요인

파괴적 변화

산업에 대한 영향요인

성장 촉진요인

산업 잠재적 리스크와 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter의 Five Forces 분석

PESTEL 분석

가격 동향

지역별

향후 시장 동향

기술과 혁신 상황

현재 기술 동향

신기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속 가능한 실천

폐기물 감축 전략

생산 에너지 효율

친환경 이니셔티브

탄소발자국 고려

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

인수합병(M&A)

파트너십 및 협업

신제품 발매

확대 계획

제5장 시장 규모와 예측 : 재료별, 2021-2034년

주요 동향

리튬 이온 배터리 재료

정극 재료(LFP, NMC, NCA, LCO)

양극 재료(흑연, 실리콘, 리튬 금속)

전해질 재료

세퍼레이터 재료

고체 배터리 재료

고체 전해질(산화물, 황화물, 폴리머)

인터페이스 재료

첨단 전극 재료

슈퍼커패시터 재료

전극 재료(탄소계, 금속 산화물)

전해질용액

세퍼레이터 재료

첨단 숯 재료

그래핀과 그 유도체

탄소나노튜브

탄소섬유 복합재

에너지 재료

고에너지 밀도 화합물

추진제

폭발물

연료배터리 재료

촉매 재료

막재료

전극 재료

제6장 시장 규모와 예측 : 용도별, 2021-2034년

주요 동향

자동차 용도

전기자동차(BEV, PHEV, HEV)

자동차용 전자기기

start stop 시스템

가전제품

스마트폰 및 태블릿

노트북 및 웨어러블

파워 뱅크 및 휴대용 디바이스

에너지 저장 시스템

그리드 스케일 저장

주택 에너지 저장

상업과 산업용 저장

항공우주 및 방위

항공기와 우주선 용도

군 및 방위 시스템

무인 차량 및 드론

산업용도

자재관리 기기

백업 파워 써플라이 시스템

통신 인프라

의료 및 헬스케어

이식형 디바이스

휴대형 의료기기

응급 의료 시스템

제7장 시장 규모와 예측 : 기술별, 2021-2034년

주요 동향

배터리 기술

리튬 이온 배터리

전고체 배터리

나트륨 이온 배터리

금속 공기 배터리

커패시터 기술

슈퍼커패시터/울트라 커패시터

하이브리드 커패시터

세라믹 커패시터

연료전지 기술

양성자 교환막(PEM)

고체 산화물 연료전지(SOFC)

알칼리 연료전지

에너지수확기술 기술

열전 재료

압전 재료

태양광발전 재료

제8장 시장 규모와 예측 : 최종 이용 산업별, 2021-2034년

주요 동향

자동차 산업

전자기기 및 반도체

에너지 및 유틸리티

항공우주 및 방위

헬스케어 및 의료기기

산업 제조업

통신

해운·운송

제9장 시장 규모와 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카공화국

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제10장 기업 개요

Tesla

Panasonic Corporation

Samsung SDI

LG Energy Solution

Contemporary Amperex Technology

BYD Company Limited

QuantumScape Corporation

Solid Power

Sila Nanotechnologies

Group14 Technologies

Wildcat Discovery Technologies

Amprius Technologies

Enovix Corporation

Ion Storage Systems

Ampcera

Sion Power Corporation

Oxis Energy

LSH

영문 목차

영문목차

The Global Energy Dense Materials Market was valued at USD 61.2 billion in 2024 and is estimated to grow at a CAGR of 12.8% to reach USD 206.7 billion by 2034. This market is experiencing strong momentum due to the increasing urgency around carbon reduction and the shift toward more sustainable, electrified energy systems. As renewable energy continues to gain traction in power generation, the demand for compact and highly efficient energy storage solutions is becoming more critical. Energy dense materials support this transition by ensuring grid stability, balancing supply during peak demand, and improving the consistency of power delivery from intermittent sources. Their importance is rising across various sectors as the global appetite for efficient, lightweight, and high-capacity energy storage continues to grow.

The rise of electric mobility is one of the primary contributors to market growth. As electric vehicles scale quickly across global markets, the need for batteries that deliver longer range, faster charging, and reduced weight becomes vital. Energy dense materials also serve an important role in aerospace propulsion systems for electric aircraft and drones, where maximizing energy per unit of mass results in longer flight duration and greater payload capabilities, ultimately driving innovation across air transport technologies.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$61.2 Billion

Forecast Value

$206.7 Billion

CAGR

12.8%

In 2024, the lithium-ion battery materials segment generated USD 24.5 billion. Their widespread use is driven by their superior energy density relative to other options such as fuel cell materials, supercapacitors, and solid-state batteries. Lithium-ion batteries store significant energy in compact, lightweight formats, making them the go-to solution for portable electronics, electric vehicles, and large-scale energy storage systems. Their strong power output, extended cycle life, and stable performance have made them a foundational technology in modern energy storage and have supported fast adoption across industries ranging from consumer electronics to utility-scale grid storage.

The automotive applications segment held the largest share in 2024, accounting for 30% share. These applications are at the heart of energy dense material innovation, driven by the rising need for vehicles that can travel further, charge quicker, and match traditional engine performance. Battery technologies delivering greater energy density per unit of space and weight help address consumer range concerns and support widespread EV adoption. As the automotive industry continues to expand, it remains a key force behind the market's growth.

U.S. Energy Dense Materials Market reached USD 11.7 billion in 2024 and is forecasted to grow at a CAGR of 13% through 2034. With steady economic expansion, increased energy needs, and industrial growth, the U.S. has seen rising demand for efficient batteries, magnets, and fuel cell components. Energy dense materials are helping industries optimize energy use, reduce costs, and improve overall system performance. Their role in energy storage and conversion across sectors continues to make them essential for building a more resilient and efficient energy infrastructure.

Key companies operating in the Global Energy Dense Materials Market include LG Energy Solution, Panasonic Corporation, Samsung SDI Co., Ltd., Tesla, Inc., and Contemporary Amperex Technology Co. Limited (CATL). To strengthen their foothold in the global energy dense materials landscape, leading companies are focusing on several strategic priorities. These include aggressive investment in R&D for advanced chemistries that improve energy density, safety, and lifecycle. Companies are also scaling up production capacities to meet rising EV and grid demand, particularly in key growth regions. Strategic alliances with automakers and energy providers are helping secure long-term contracts. Additionally, firms are diversifying product portfolios to include next-gen materials like solid-state and lithium-sulfur technologies, while optimizing their global supply chains for cost efficiency and stability.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Material type

2.2.3 Application

2.2.4 End Use Industry

2.2.5 Technology

2.3 TAM analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.6.1 Technology and innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.8 Future market trends

3.9 Technology and innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Size and Forecast, By Material Type, 2021-2034 (USD Million) (Tons)