그라우트 및 앵커 시장 : 기회, 촉진요인, 업계 동향 분석 및 예측(2025-2034년)

Grouts and Anchors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801864

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 192 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

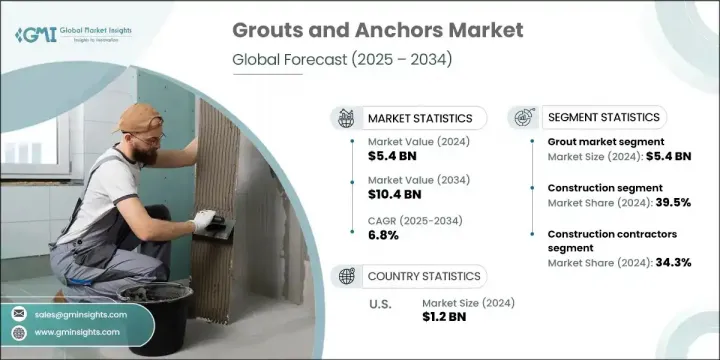

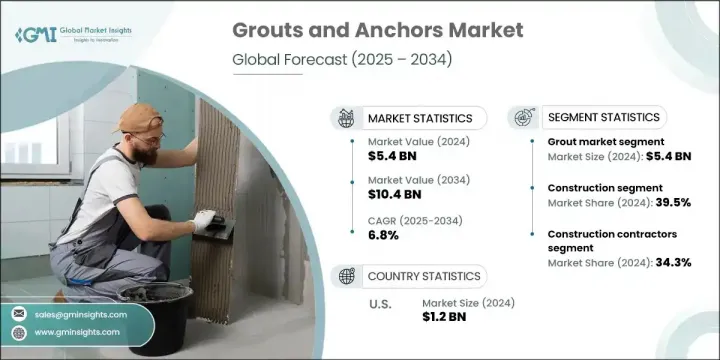

세계의 그라우트 및 앵커 시장 규모는 2024년에는 54억 달러에 달하고, CAGR 6.8%로 성장할 전망이며 2034년에는 104억 달러에 이를 것으로 추정됩니다.

시장 확대는 도시화 증가, 건설 활동 급증, 인프라 복원력 강화에 대한 관심 증대와 밀접하게 연관되어 있습니다. 그라우트 및 앵커는 최근 건축 및 리모델링 프로젝트 전반에서 기초를 안정화하고, 고정물을 고정하며, 틈새를 메움으로써 구조적 무결성을 보장하는 필수 재료입니다. 이러한 구성 요소는 상업용 건물, 교량, 터널 등을 포함한 토목 인프라의 안전성과 수명에 기초를 제공합니다.

주거용, 상업용 및 공공 인프라에 대한 전 세계 투자가 가속화됨에 따라 고성능 및 내구성 건설 자재에 대한 수요도 함께 증가하고 있습니다. 기술적으로 발전되고 적용이 용이한 앵커링 및 그라우팅 솔루션에 대한 선호도 증가 역시 산업을 형성하고 있습니다. 또한 진화하는 건축 규정 및 안전 규범 준수에 대한 요구는 선진국과 신흥 경제국 모두에서 시장 성장세를 지속적으로 촉진하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

54억 달러

예측 금액

104억 달러

CAGR

6.8%

그라우트 부문은 2024년 54.3%의 시장 점유율로 우위를 점했으며, 이러한 재료는 구조물 안정화, 공동 채움, 하중 분산 개선에 널리 사용됩니다. 강도와 적응성으로 유명한 그라우트는 구조물 보수, 기초 보강, 내구성과 정밀도가 요구되는 까다로운 건설 작업에 필수적입니다. 장기적인 신뢰성 덕분에 소규모 보수부터 대규모 인프라 프로젝트까지 선호되는 솔루션입니다.

건설 부문은 2024년 39.5%의 점유율을 기록했으며, 이는 주거용, 산업용, 상업용 개발에 대한 지속적인 전 세계 수요에 기인합니다. 건설사들이 더 오래 지속되고 규정을 준수하는 건물을 지향함에 따라, 성능과 안전 기대치를 충족시키기 위해 고품질 그라우팅 및 앵커링 제품으로 눈을 돌리고 있습니다. 지속 가능한 건설 자재로의 전환도 최근 건축 관행에서 고급 그라우트 및 앵커 사용을 강화하는 데 기여하고 있습니다.

미국의 그라우트 및 앵커 시장은 88.7%의 점유율을 차지했으며, 2024년에는 12억 달러를 창출했습니다. 이러한 선도적 지위는 전국적인 인프라 업그레이드 및 신규 건설에 대한 대규모 투자에서 비롯됩니다. 지속적인 연방 인프라 계획은 강도, 내구성 및 향상된 복원력을 제공하는 신뢰할 수 있는 그라우팅 및 앵커링 재료에 대한 수요를 유지하고 있습니다. 인프라 노후화와 기후 회복력이 중요해짐에 따라 건설사들은 진화하는 구조적 요구사항에 부합하는 고성능 제품을 지속적으로 찾고 있습니다.

세계의그라우트 및 앵커 시장을 형성하는 주요 기업은 Hilti AG, MAPEI SpA, Sika AG, BASF SE, Fosroc Internationa 등입니다. 그라우트 및 앵커 분야의 선도 기업들은 시장 지위를 강화하기 위해 여러 전략적 이니셔티브에 주력하고 있습니다. 여기에는 경화 시간이 더 빠르고 내구성이 높으며 지속가능성 기능을 갖춘 혁신적인 소재 개발을 위한 연구개발(R&D) 확대가 포함됩니다. 많은 기업들이 특정 건설 용도의 요구를 충족시키기 위해 제품 맞춤화와 고급 화학 제형에 투자하고 있습니다. 전략적 합병, 지역적 파트너십 및 인수도 지리적 영향력을 확대하기 위한 일반적인 접근 방식입니다. 또한 기업들은 제품 채택을 촉진하고 적절한 적용을 보장하기 위해 계약업체 대상 교육 프로그램을 강조하는 한편, 정확한 제형 권장 및 프로젝트 계획을 위한 디지털 도구를 통합하고 있습니다.

목차

제1장 조사 방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사의 전제와 한계

제2장 주요 요약

제3장 산업 고찰

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

산업에 미치는 영향요인

성장 촉진요인

지속 가능한 건설로의 전환

하이브리드 기술과 스마트 기술 채택

주입형 접착 앵커의 성장 주도

산업의 잠재적 리스크 및 과제

원자재 공급 불안정성

규제 준수의 압력

시장 기회

모듈형과 조립식 건설 증가

맞춤화 및 특수 제품

건설 기술 기업과의 협력

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

가격 동향

지역별

제품 유형별

코스트 내역 분석

특허 분석

지속가능성과 환경 측면

지속 가능한 사례

폐기물 감축 전략

생산의 에너지 효율

친환경 활동

탄소발자국 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

합병과 인수

파트너십 및 협업

신제품 발매

확대계획과 자금조달

제5장 시장 추정 및 예측 : 제품 유형별(2021-2034년)

주요 동향

그라우트 시장

시멘트 기반 그라우트

에폭시 그라우트

화학 그라우트

기타 그라우트 유형

폴리우레탄 그라우트

아크릴 그라우트

앵커 시장

기계식 앵커

화학식 앵커

접착 앵커

제6장 시장 추정 및 예측 : 용도별(2021-2034년)

주요 동향

건설

주거용

상업용

산업용

인프라

운송

교량 및 고속도로

터널 및 지하

철도 인프라

공항 건설

유틸리티

물 및 폐수

발전

통신

에너지 인프라

해양

항만 건설

해양 플랫폼

연안 보호

선박 수리 및 유지 보수

광업 및 지하 용도

광산 지원 시스템

지하 드릴링

터널 안정화

지반 개량

제7장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

주요 동향

건설 계약자

종합 건설업자

전문 건설업자

인프라 개발자

산업 최종 용도

판매자와 소매업체

제8장 시장 추정 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Arkema Group(via Bostik)

BASF SE(Master Builders Solutions)

Fosroc International Limited

HB Fuller Company

Henkel AG & Co. KGaA(Loctite brand)

Hilti AG

Laticrete International

MAPEI SpA

Saint-Gobain Weber

Sika AG

Stanley Black & Decker

Wurth Group

HBR

영문 목차

영문목차

The Global Grouts and Anchors Market was valued at USD 5.4 billion in 2024 and is estimated to grow at a CAGR of 6.8% to reach USD 10.4 billion by 2034. Market expansion is strongly tied to increased urbanization, a surge in construction activity, and the growing emphasis on infrastructure resilience. Grouts and anchors are essential materials that ensure structural integrity by stabilizing foundations, securing fixtures, and filling gaps across both modern construction and retrofitting projects. These components are foundational to the safety and longevity of civil infrastructure, including commercial buildings, bridges, tunnels, and more.

As global investments in residential, commercial, and public infrastructure accelerate, so does the demand for high-performance and durable construction materials. The growing preference for technologically advanced and easy-to-apply anchoring and grouting solutions is also shaping the industry. Additionally, the push for compliance with evolving building codes and safety regulations continues to drive market momentum across both developed and emerging economies.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$5.4 Billion

Forecast Value

$10.4 Billion

CAGR

6.8%

The grouts segment dominated with a 54.3% market share in 2024, as these materials are widely used to stabilize structures, fill cavities, and improve load distribution. Known for their strength and adaptability, grouts are essential for structural rehabilitation, foundation reinforcements, and demanding construction tasks requiring durability and precision. Their long-term reliability makes them the go-to solution in both small-scale repairs and large-scale infrastructure projects.

The construction segment held a 39.5% share in 2024, owing to constant global demand for residential, industrial, and commercial developments. As builders aim for longer-lasting, code-compliant buildings, they are turning to high-quality grouting and anchoring products to meet performance and safety expectations. The shift toward sustainable construction materials is also playing a role in reinforcing the use of advanced grouts and anchors in modern building practices.

U.S. Grouts and Anchors Market held an 88.7% share and generated USD 1.2 billion in 2024. This leadership position stems from large-scale investments in infrastructure upgrades and new construction across the country. Ongoing federal infrastructure initiatives are sustaining the demand for reliable grouting and anchoring materials that offer strength, longevity, and improved resilience. As infrastructure ages and climate resilience becomes critical, builders continue to seek high-performance products that align with evolving structural demands.

Key players shaping the Global Grouts and Anchors Market include Hilti AG, MAPEI S.p.A., Sika AG, BASF SE, and Fosroc International. To strengthen their market position, leading companies in the grouts and anchors space are focusing on several strategic initiatives. These include expanding R&D to develop innovative materials with faster curing times, higher durability, and sustainability features. Many are investing in product customization and advanced chemical formulations to meet the needs of specific construction applications. Strategic mergers, regional partnerships, and acquisitions are also common approaches to widen their geographical footprint. Furthermore, companies are emphasizing on training programs for contractors to boost product adoption and ensure proper application, while integrating digital tools for precise formulation recommendations and project planning.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Product Type

2.2.3 Application

2.2.4 End Use

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Shift toward sustainable construction

3.2.1.2 Adoption of hybrid and smart technologies

3.2.1.3 Injectable adhesive anchors leading growth

3.2.2 Industry pitfalls and challenges

3.2.2.1 Raw material supply instability

3.2.2.2 Regulatory compliance pressure

3.2.3 Market opportunities

3.2.3.1 Rise in modular and prefabricated construction

3.2.3.2 Customization and specialty products

3.2.3.3 Collaboration with construction technology firms

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 By region

3.8.2 By product type

3.9 Cost breakdown analysis

3.10 Patent analysis

3.11 Sustainability and environmental aspects

3.11.1 Sustainable practices

3.11.2 Waste reduction strategies

3.11.3 Energy efficiency in production

3.11.4 Eco-friendly Initiatives

3.12 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 North America

4.2.2 Europe

4.2.3 Asia Pacific

4.2.4 LATAM

4.2.5 MEA

4.3 Competitive analysis of major market players

4.4 Competitive positioning matrix

4.5 Strategic outlook matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product Type, 2021 - 2034 (USD Billion, Kilo Tons)

5.1 Key trends

5.2 Grouts market

5.2.1 Cementitious grouts

5.2.2 Epoxy grouts

5.2.3 Chemical grouts

5.2.4 Other grout types

5.2.4.1 Polyurethane grouts

5.2.4.2 Acrylic grouts

5.3 Anchors market

5.3.1 Mechanical anchors

5.3.2 Chemical anchors

5.3.3 Adhesive anchors

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

6.1 Key trends

6.2 Construction

6.2.1 Residential

6.2.2 Commercial

6.2.3 Industrial

6.3 Infrastructure

6.3.1 Transportation

6.3.1.1 Bridges and highways

6.3.1.2 Tunnels and underground

6.3.1.3 Railway infrastructure

6.3.1.4 Airport construction

6.3.2 Utilities

6.3.2.1 Water and wastewater

6.3.2.2 Power generation

6.3.2.3 Telecommunications

6.3.2.4 Energy infrastructure

6.4 Marine and offshore

6.4.1 Port and harbor construction

6.4.2 Offshore platforms

6.4.3 Coastal protection

6.4.4 Marine repair and maintenance

6.5 Mining and underground applications

6.5.1 Mine support systems

6.5.2 Underground excavation

6.5.3 Tunnel stabilization

6.5.4 Ground improvement

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion, Kilo Tons)

7.1 Key trends

7.2 Construction Contractors

7.2.1 General Contractors

7.2.2 Specialty Contractors

7.3 Infrastructure Developers

7.4 Industrial End Use

7.5 Distributors and Retailers

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Billion, Kilo Tons)