시멘트계 그라우트 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Cementitious Grouts Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801841

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 192 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

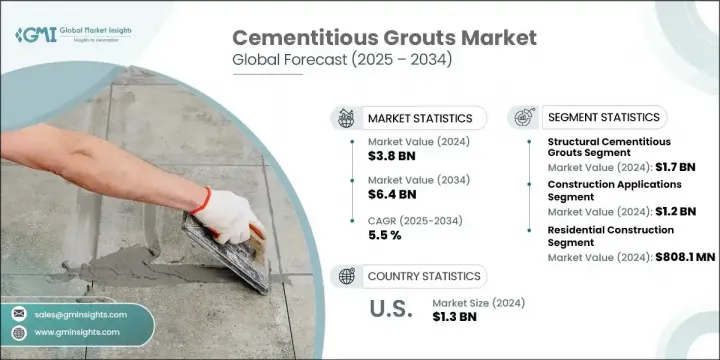

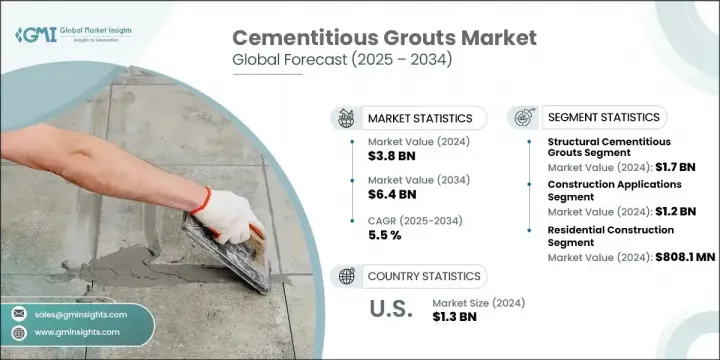

세계의 시멘트계 그라우트 시장 규모는 2024년에 38억 달러에 달하고, CAGR 5.5%로 성장할 전망이며 2034년까지는 64억 달러에 이를 것으로 추정되고 있습니다.

인프라 보강, 터널링 작업, 지반 안정화 및 고급 건설 용도 분야의 사용 증가로 시장이 견실한 성장을 보이고 있습니다. 동유럽, 아시아태평양, 중동 등 개발도상 지역의 투자가 공학용 시멘트 재료에 대한 수요를 강화하고 있습니다.

구조용 그라우트는 특히 대규모 인프라에서 압축 강도와 치수 안정성으로 인해 가장 많이 사용되고 있습니다. 그러나 성능 중심 건설이 전 세계적으로 우선순위가 되면서, 특히 내진 보강 및 터널 용도에서 내화학성 제품과 속경화 또는 수축 보정 시멘트계 그라우트의 수요가 증가하는 추세입니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

38억 달러

예측 금액

64억 달러

CAGR

5.5%

지질학적 복잡성도 기존 시멘트계 그라우트에서 미세 시멘트계 그라우트로의 전환을 촉진하고 있으며, 후자는 10%의 시장 점유율을 차지합니다. 이러한 고성능 제품은 특히 정밀한 침투와 기질 접착이 필요한 지반 공학 용도에서 토양 다짐 및 미세 균열 보수 수요가 증가하고 있습니다. 장기 내구성, 유동성, 극한 환경 조건에서의 저항성이 필수적인 분야에서 폴리머 개질 및 혼합 그라우트가 시장 관심을 더욱 사로잡으며, 고급적이고 적응력 있는 건설 자재로의 추세를 뒷받침하고 있습니다.

구조용 시멘트계 그라우트 부문은 2024년 17억 달러 규모로, 토목 및 인프라 건설에서의 강력한 수요로 인해 우위를 유지하고 있습니다. 이러한 재료는 특히 교량 베어링, 베이스 플레이트, 프리캐스트 조립체와 같은 하중이 중요한 용도에 사용됩니다. 높은 압축 강도, 중동적 하중에 대한 저항성, 치수 안정성으로 인해 공공 인프라 및 교통 프로젝트에서 선호되는 선택입니다. 중국과 인도 등 국가들의 상당한 기여로 아시아태평양 지역의 급속한 인프라 개발은 특히 지하철 시스템 및 고속도로 프로젝트에 대한 수요를 증가시키고 있습니다.

시멘트계 그라우트 부문은 2024년 38%의 점유율을 기록했습니다. 보강 앵커링, 고층 구조물, 프리캐스트 시스템에서의 광범위한 사용은 높은 하중을 견디고 다양한 기후 조건에서 성능을 발휘할 수 있는 재료에 대한 수요에서 비롯되며, 이는 최근 건설 기술과 고성능 콘크리트 설계에서 구조용 그라우트의 핵심적 역할을 반영합니다.

미국의 시멘트계 그라우트 시장 점유율은 82%로 2024년에는 13억 달러를 창출했습니다. 이러한 우위적 지위는 지속적인 인프라 재건 사업, 연방 프로그램을 통한 공공 자금 확대, 지속가능한 건설 자재로의 전환 증가에 힘입었습니다. 미국 시장은 특히 교량, 터널링, 프리캐스트 연결, 토양 안정화에 사용되는 고성능 그라우트 수요에 의해 촉진되고 있습니다. 이러한 용도는 특히 까다로운 토목 환경에서 높은 강도, 최소한의 투수성, 강력한 내화학성을 제공하는 솔루션을 요구합니다.

세계의 시멘트계 그라우트 시장에서 선도적인 기업으로는 Holcim Group(LafargeHolcim), MAPEI SpA, Sika AG, Fosroc International Limited, BASF SE 등이 있습니다. 시멘트계 그라우트 부문에서의 입지가 확대되기를 위해 주요 업체들은 기계적 성능과 내구성을 개선한 고급 그라우팅 제형 개발을 위한 연구개발(R&D) 투자와 같은 전략을 활용하고 있습니다. 기업들은 진화하는 건설 기준에 부합하기 위해 저수축성, 속경화, 친환경 그라우트에 주력하고 있습니다. 고성장 지역에서의 생산 능력 확대와 지역 유통업체와의 전략적 제휴도 업체들이 현지 수요를 활용하는 데 도움이 되고 있습니다. 또한 기업들은 지속가능성 촉진 프로그램으로 자금 지원되는 인프라 프로젝트에 대응하기 위해 친환경 건축 규정 인증 및 준수를 우선시함으로써 공공 및 민간 건설 부문 전반에 걸친 광범위한 채택을 보장하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

인프라 개발과 현대화

건설 산업 수요 증가

터널링 및 광산 확장

지속가능성과 환경규제

업계의 잠재적 리스크 및 과제

높은 초기 투자 비용

기술적 전문지식 요건

원재료 가격 변동

시장 기회

신흥 시장 진출

친환경 건축 및 지속 가능한 건설

고급 소재 혁신

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속가능한 실천

폐기물 감축 전략

생산의 에너지 효율

환경 친화적인 노력

탄소발자국 고려 사항

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품 유형별(2021-2034년)

주요 동향

구조용 시멘트계 그라우트

고성능 구조용 그라우트

표준 구조용 그라우트

속 경화 구조용 그라우트

비구조용 시멘트계 그라우트

범용 그라우트

공극 충전 그라우트

실링과 방수 그라우트

전문 분야 시멘트계 그라우트

초고성능 그라우트

해양 및 해양 그라우트

내고온 그라우트

내약품성 그라우트

초미세 시멘트계 그라우트

혼합 및 개질 그라우트

폴리머 개질 그라우트

섬유 강화 그라우트

광물 혼화제 강화 그라우트

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

건설 용도

기초 및 베이스 플레이트 그라우팅

앵커 볼트 설치

프리캐스트 요소 연결

구조 수리 및 리모델링

광산 및 터널링

지반의 강화와 안정화

침수 방지

암반 보강

갱도 및 터널 라이닝

인프라 프로젝트

교량 건설 및 보수

댐 및 저수지 용도

고속도로와 교통 인프라

유틸리티 및 파이프라인 프로젝트

해양 및 해상 용도

항만 건설

해상 풍력 터빈 설치

수중 구조 수리

산업 용도

설비 기초 그라우트

바닥 및 포장 용도

화학 플랜트 및 시설 건설

지질공학 용도

토양 안정화

지반 개량

경사면의 안정화

제7장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

주택 건설

단독 주택

집합 건물

리모델링 및 개조

상업건설

오피스 빌딩

소매점과 쇼핑센터

접객와 엔터테인먼트

산업 건설

제조 시설

창고와 배송 센터

발전 시설

인프라와 토목공학

교통 인프라

물 및 폐수 처리

에너지 인프라

광업 및 채굴 산업

석탄 채굴

금속 및 광물 추출

석유 및 가스 사업

해양 산업

조선과 수리

해외 에너지 프로젝트

항만 및 터미널 개발

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

Sika AG

MAPEI SpA

BASF SE(Master Builders Solutions)

Fosroc International Limited

Euclid Chemical Company

LafargeHolcim(Holcim Group)

CEMEX SAB de CV

CRH plc

HeidelbergCement AG

Arkema Group

UltraTech Cement Limited

Perma Construction Aids Pvt. Ltd.

Saint-Gobain Weber

Ambuja Cements Limited

HBR

영문 목차

영문목차

The Global Cementitious Grouts Market was valued at USD 3.8 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 6.4 billion by 2034. The market is experiencing solid growth due to increased use in infrastructure reinforcement, tunneling operations, geotechnical stabilization, and advanced construction applications. Investments across developing regions such as Eastern Europe, Asia-Pacific, and the Middle East are intensifying the demand for engineered cementitious materials.

Structural-grade grouts remain the most used due to their compressive strength and dimensional stability, particularly in large-scale infrastructure. However, the market is witnessing growing traction for chemical-resistant variants and rapid-set or shrinkage-compensated cementitious grouts, particularly in seismic retrofitting and tunnel applications, as performance-based construction becomes a priority globally.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$3.8 Billion

Forecast Value

$6.4 Billion

CAGR

5.5%

Geological complexities are also contributing to the shift from conventional cement grouts to microfine cement grouts, which hold a 10% share. These high-performance products are gaining demand in soil consolidation and fine crack remediation, especially in geotechnical applications that require precise penetration and substrate bonding. Polymer-modified and blended grouts are further capturing market interest where long-term durability, flowability, and resistance in extreme environmental conditions are essential, supporting the trend toward advanced and adaptable construction materials.

The structural cementitious grouts segment was worth USD 1.7 billion in 2024, maintaining dominance due to its strong uptake in civil and infrastructure construction. These materials are particularly used in load-critical applications like bridge bearings, base plates, and precast assemblies. Their high compressive strength, resistance to heavy dynamic loads, and dimensional stability make them the preferred choice in public infrastructure and transport projects. The fast-paced infrastructure development across Asia-Pacific, with countries like China and India contributing significantly, is driving up the demand, particularly for metro systems and expressway projects.

The cementitious grouts segment held 38% share in 2024. Their widespread use in reinforcement anchoring, high-rise structures, and precast systems is due to the demand for materials that can endure high loads and perform in varied climatic conditions, reflecting the critical role of structural grouts in modern construction techniques and high-performance concrete design.

US Cementitious Grouts Market held 82% share and generated USD 1.3 billion in 2024. This dominant position is supported by continual infrastructure renewal initiatives, expanded public funding through federal programs, and a growing shift toward sustainable construction materials. The market in the US is particularly driven by demand for high-performance grouts used in bridges, tunneling, precast bonding, and soil stabilization. These applications require solutions offering high strength, minimal permeability, and strong chemical resistance, particularly in demanding civil engineering environments.

The leading players in the Global Cementitious Grouts Market include Holcim Group (LafargeHolcim), MAPEI S.p.A, Sika AG, Fosroc International Limited, and BASF SE. To expand their presence in the cementitious grouts sector, key players are leveraging strategies such as investing in R&D to develop advanced grouting formulations that deliver improved mechanical performance and durability. Companies are focusing on low-shrinkage, rapid-setting, and eco-friendly grouts to align with evolving construction standards. Expanding manufacturing capacity in high-growth regions and forming strategic partnerships with regional distributors are also helping players tap into localized demand. Additionally, businesses are prioritizing certifications and compliance with green building codes to cater to infrastructure projects funded through sustainability-driven programs, ensuring broader adoption across public and private construction sectors.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product type

2.2.3 Raw Material

2.2.4 Application

2.2.5 End use industry

2.2.6 Production process

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Infrastructure development and modernization

3.2.1.2 Growing construction industry demand

3.2.1.3 Tunneling and mining expansion

3.2.1.4 Sustainability and environmental regulations

3.2.2 Industry pitfalls and challenges

3.2.2.1 High initial investment costs

3.2.2.2 Technical expertise requirements

3.2.2.3 Raw material price volatility

3.2.3 Market opportunities

3.2.3.1 Emerging market penetration

3.2.3.2 Green building and sustainable construction

3.2.3.3 Advanced material innovations

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation Landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and Innovation Landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and Environmental Aspects

3.12.1 Sustainable Practices

3.12.2 Waste Reduction Strategies

3.12.3 Energy Efficiency in Production

3.12.4 Eco-friendly Initiatives

3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 Structural Cementitious Grouts

5.2.1 High-Performance Structural Grouts

5.2.2 Standard Structural Grouts

5.2.3 Rapid-Setting Structural Grouts

5.3 Non-Structural Cementitious Grouts

5.3.1 General Purpose Grouts

5.3.2 Void Filling Grouts

5.3.3 Sealing and Waterproofing Grouts

5.4 Specialty Cementitious Grouts

5.4.1 Ultra-High Performance Grouts

5.4.2 Marine and Offshore Grouts

5.4.3 High-Temperature Resistant Grouts

5.4.4 Chemical Resistant Grouts

5.5 Microfine Cement Grouts

5.6 Blended and Modified Grouts

5.6.1 Polymer-Modified Grouts

5.6.2 Fiber-Reinforced Grouts

5.6.3 Mineral Admixture Enhanced Grouts

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Construction applications

6.2.1 Foundation and base plate grouting

6.2.2 Anchor bolt installation

6.2.3 Precast element connections

6.2.4 Structural repairs and rehabilitation

6.3 Mining and tunneling

6.3.1 Ground consolidation and stabilization

6.3.2 Water ingress control

6.3.3 Rock mass reinforcement

6.3.4 Shaft and tunnel lining

6.4 Infrastructure projects

6.4.1 Bridge construction and repair

6.4.2 Dam and reservoir applications

6.4.3 Highway and transportation infrastructure

6.4.4 Utility and pipeline projects

6.5 Marine and offshore applications

6.5.1 Port and harbor construction

6.5.2 Offshore wind turbine installations

6.5.3 Underwater structural repairs

6.6 Industrial applications

6.6.1 Equipment foundation grouting

6.6.2 Floor and pavement applications

6.6.3 Chemical plant and facility construction

6.7 Geotechnical applications

6.7.1 Soil stabilization

6.7.2 Ground improvement

6.7.3 Slope stabilization

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Residential construction

7.2.1 Single-family housing

7.2.2 Multi-family housing

7.2.3 Renovation and remodeling

7.3 Commercial construction

7.3.1 Office buildings

7.3.2 Retail and shopping centers

7.3.3 Hospitality and entertainment

7.4 Industrial construction

7.4.1 Manufacturing facilities

7.4.2 Warehouses and distribution centers

7.4.3 Power generation facilities

7.5 Infrastructure and civil engineering

7.5.1 Transportation infrastructure

7.5.2 Water and wastewater treatment

7.5.3 Energy infrastructure

7.6 Mining and extractive industries

7.6.1 Coal mining

7.6.2 Metal and mineral extraction

7.6.3 Oil and gas operations

7.7 Marine and offshore industries

7.7.1 Shipbuilding and repair

7.7.2 Offshore energy projects

7.7.3 Port and terminal development

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)