발포 폴리스티렌(EPS) 포장재 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Expanded Polystyrene for Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1801803

리서치사:Global Market Insights Inc.

발행일:2025년 08월

페이지 정보:영문 180 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

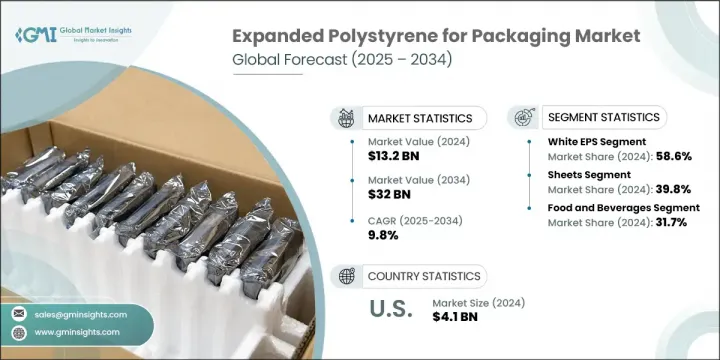

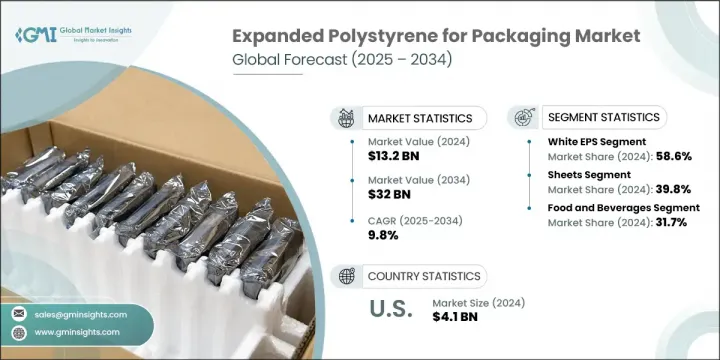

세계의 발포 폴리스티렌 포장재 시장은 2024년에는 132억 달러에 달하고, CAGR 9.8%로 성장할 전망이며 2034년에는 320억 달러에 이를 것으로 추정되고 있습니다.

이 시장 성장은 높은 단열 특성을 제공하면서도 가볍고 충격 흡수 기능이 있는 포장재에 대한 수요에 의해 촉진되고 있습니다. EPS는 구조적 무결성을 유지하고 신선도를 보존함으로써 장거리 운송 중 상품(특히 부패하기 쉬운 상품)을 보호하는 데 도움이 됩니다. 즉석식 및 편리한 식품 솔루션에 대한 선호도 증가 역시 효율적이고 신뢰할 수 있는 포장 형태에 대한 수요 증가를 촉진하고 있습니다.

급증하는 전자상거래 활동과 신속한 문 앞 배송 서비스는 EPS 포장 시장 확장에 지속적으로 영향을 미치고 있습니다. 식료품, 전자제품, 의약품 등 온라인 구매가 증가함에 따라 운송 중 제품을 보호할 수 있을 만큼 가볍고 내구성 있는 포장에 대한 요구가 더욱 강조되고 있습니다. 제조업체와 물류 업체들은 이러한 요건을 충족시키면서 비용 효율적인 배송을 지원하는 EPS를 점점 더 선호하고 있습니다. 이 소재의 신뢰성, 강도 대비 무게 비율, 단열 능력은 최근 유통 및 배송 요구에 대응하는 다양한 산업 분야에서 핵심 선택지로 자리매김하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

132억 달러

예측 금액

320억 달러

CAGR

9.8%

2024년에도 화이트 EPS는 77억 달러의 시장 가치를 기록하며 최고 실적을 보인 부문으로 자리매김했습니다. 이 변종은 경제성, 입증된 신뢰성, 다양한 포장 용도에 걸친 적합성으로 널리 선호됩니다. FMCG 및 농산물부터 전자제품 및 가전제품에 이르기까지 화이트 EPS는 계속해서 우위를 점하고 있습니다. 성형 및 표면 기술의 발전으로 고속 자동화 포장 시스템과의 호환성이 향상되었습니다. 단순해 보이지만 화이트 EPS는 속도와 기능성을 우선시하는 대량 생산, 비용 민감형 포장 환경에서 널리 활용됩니다.

EPS 시트 부문은 2024년 52억 달러의 매출을 기록했습니다. 이 시트는 우수한 내충격성과 경량성을 제공하며 매우 경제적인 것으로 알려져 있습니다. 포장된 전자제품, 기계류, 소비자 가전제품의 구조적 보호를 강화하기 위해 다이컷 처리되거나 폼 백킹과 라미네이팅되는 경우가 많습니다. 이러한 분야에서 맞춤형 보호 포장 수요가 증가함에 따라 EPS 시트는 향후 몇 년간 선호되는 소재로 자리매김할 것입니다.

미국의 발포 폴리스티렌 포장재 시장 규모는 2024년에 41억 달러로, 2034년까지의 CAGR 9%로 성장할 전망입니다. 미국의 견고한 식품 및 음료 산업은 특히 콜드체인 물류 및 단열 용도에서 EPS 사용을 지속적으로 촉진하고 있다. 온라인 쇼핑 트렌드는 EPS 기반 보호 포장 수요를 더욱 증폭시키고 있다. 시장 업체들은 증가하는 환경 문제에 대응하기 위해 생물 기반 대체재와 지속 가능한 재활용 옵션을 모색 중이다. 운송 배출량을 줄이고 비용을 절감하는 경량 포장재에 대한 강조는 혁신을 촉진하며 미국 내 성장의 새로운 길을 열어주고 있습니다.

세계의 발포 폴리스티렌 포장재 시장을 형성하는 주요 기업으로는 BASF SE, KANEKA CORPORATION, Alpek SAB de CV, TotalEnergies, Synthos, Dart Container Corporation, Wuxi Xingda Foam Plastic, Tamai Kasei Corporation, DuPont, Styrotech, Inc., Versalis Sp. Foam Products, Foamcraft USA, LLC, Styropek 등이 있습니다. EPS 포장 시장의 선도 기업들은 경쟁 엣지를 유지하기 위해 제품 혁신, 지역 확장, 지속 가능성 이니셔티브를 혼합하여 시행하고 있습니다. 많은 기업들이 전 세계 친환경 동향에 부응하기 위해 재활용 가능하고 바이오 기반 EPS 솔루션 개발에 투자하고 있습니다. 물류 기업 및 FMCG 기업과의 전략적 파트너십을 통해 변화하는 포장 수요에 대응하고 있습니다. 온라인 소매 및 콜드체인 공급망의 대량 수요를 충족시키기 위해 생산 자동화와 맞춤형 EPS 금형이 우선시되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

식품 및 음료 업계에서의 수요 증가

전자상거래와 택배 서비스의 급속한 확대

건설 업계 성장

비용효율과 다양한 용도

재활용성 및 기술 발전

업계의 잠재적 위험 및 과제

환경 문제와 규제 압력

지속 가능한 대체 포장재로 대체

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신 미래

현재의 기술 동향

신흥기술

가격 동향

과거 가격 분석(2021-2024년)

가격 동향 요인

지역별 가격 차이

가격 예측(2025-2034년)

가격 전략

새로운 비즈니스 모델

규제 준수 요건

지속가능성 대책

지속 가능한 재료의 평가

탄소발자국 분석

순환형 경제의 실현

지속가능성 인증 및 기준

지속가능성 ROI 분석

세계 소비자 감정 분석

특허 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

시장 집중 분석

주요 기업의 경쟁 벤치마킹

재무실적의 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업 폭

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전(2021-2024년)

합병과 인수

파트너십 및 협업

기술 발전

확대 및 투자 전략

지속가능성에 대한 노력

디지털 변혁의 대처

신흥기업/스타트업 기업 경쟁 구도

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

주요 동향

블랙

그레이

화이트

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

시트

트레이 및 클램쉘

폼 쿨러

컵 및 볼

포장용 폼

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

주요 동향

식품 및 음료

블랙

그레이

화이트

푸드서비스

블랙

그레이

화이트

헬스케어

블랙

그레이

화이트

전자 및 전기기기

블랙

그레이

화이트

건축 및 건설

블랙

그레이

화이트

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제9장 기업 프로파일

Alpek SAB de CV

BASF SE

Cellofoam

Dart Container Corporation

DuPont

Engineered Foam Products

Epsilyte LLC

Flint Hills Resources

Foam Holdings, Inc.

Foam Products Corporation

Foamcraft USA, LLC

Geofoam International LLC

Harbor Foam

KK Nag Pvt. Ltd.

KANEKA CORPORATION

Michigan Foam Products LLC

Poliestireno de San Luis SA de CV

Storopack

Styropek

Styrotech, Inc.

Synthos

Tamai Kasei Corporation

TotalEnergies

Versalis SpA

Wuxi Xingda Foam Plastic

HBR

영문 목차

영문목차

The Global Expanded Polystyrene for Packaging Market was valued at USD 13.2 billion in 2024 and is estimated to grow at a CAGR of 9.8% to reach USD 32 billion by 2034. This market growth is being driven by the need for lightweight, shock-absorbing packaging materials that offer high insulation properties. EPS helps protect goods-especially perishables-during long-distance transport by maintaining structural integrity and preserving freshness. The rising preference for ready-to-eat meals and convenient food solutions is also prompting increased demand for efficient and reliable packaging formats.

Surging e-commerce activities and rapid doorstep delivery services continue to influence the expansion of the EPS packaging market. As more consumers shift toward purchasing items like groceries, electronics, and pharmaceuticals online, there is a stronger emphasis on packaging that is lightweight yet resilient enough to protect goods in transit. Manufacturers and logistics providers increasingly favor EPS as it checks these boxes and supports cost-effective shipping. The material's reliability, strength-to-weight ratio, and insulation capabilities make it a key choice across sectors responding to modern distribution and delivery needs.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$13.2 Billion

Forecast Value

$32 Billion

CAGR

9.8%

White EPS remained the top-performing segment in 2024 with a market valuation of USD 7.7 billion. This variant is widely preferred for its affordability, proven reliability, and suitability across diverse packaging applications. From FMCG and agricultural produce to electronics and household appliances, white EPS continues to dominate. Advances in molding and surface technology have improved its compatibility with high-speed automated packaging systems. Although it appears simple, white EPS is widely utilized in high-volume, cost-sensitive packaging environments that prioritize speed and functionality.

The EPS sheets segment generated USD 5.2 billion in 2024. These sheets offer excellent impact resistance, are lightweight, and are known for being highly economical. They are often die-cut or laminated with foam backings to enhance structural protection in packaged electronics, machinery, and consumer appliances. The rising demand for tailored and protective packaging in these sectors ensures that EPS sheets will remain a preferred material in the years to come.

United States Expanded Polystyrene for Packaging Market generated USD 4.1 billion in 2024, registering a CAGR of 9% through 2034. The country's robust food and beverage industry continues to drive EPS usage, especially in cold chain logistics and insulation applications. Online shopping trends further amplify demand for EPS-based protective packaging. Market players are now exploring bio-based alternatives and sustainable recycling options to respond to increasing environmental concerns. Emphasis on lighter packaging that reduces shipping emissions and lowers costs is prompting innovations, creating new avenues for growth in the US.

Key players shaping the Global Expanded Polystyrene for Packaging Market include BASF SE, KANEKA CORPORATION, Alpek S.A.B. de C.V., TotalEnergies, Synthos, Dart Container Corporation, Wuxi Xingda Foam Plastic, Tamai Kasei Corporation, DuPont, Styrotech, Inc., Versalis S.p.A., Michigan Foam Products LLC, Engineered Foam Products, Foamcraft USA, LLC, and Styropek. Leading companies in the EPS packaging market are implementing a mix of product innovation, regional expansion, and sustainability initiatives to maintain a competitive edge. Many are investing in the development of recyclable and bio-based EPS solutions to align with global eco-conscious trends. Strategic partnerships with logistics firms and FMCG companies allow them to address evolving packaging needs. Automation in production and customized EPS molds are being prioritized to meet high-volume demand from online retail and cold-chain supply chains.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry snapshot

2.2 Key market trends

2.2.1 Packaging type trends

2.2.2 Material trends

2.2.3 Application trends

2.2.4 Regional

2.3 TAM Analysis, 2025-2034 (USD Billion)

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing demand in food and beverage industry

3.2.1.2 Rapid expansion of e-commerce and home delivery services

3.2.1.3 Construction industry growth

3.2.1.4 Cost-effectiveness and versatile applications

3.2.1.5 Recyclability and technological advancements

3.2.2 Industry pitfalls and challenges

3.2.2.1 Environmental concerns and regulatory pressure

3.2.2.2 Substitution by sustainable packaging alternatives

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter’s analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 Historical price analysis (2021-2024)

3.8.2 Price trend drivers

3.8.3 Regional price variations

3.8.4 Price forecast (2025-2034)

3.9 Pricing strategies

3.10 Emerging business models

3.11 Compliance requirements

3.12 Sustainability measures

3.12.1 Sustainable materials assessment

3.12.2 Carbon footprint analysis

3.12.3 Circular economy implementation

3.12.4 Sustainability certifications and standards

3.12.5 Sustainability roi analysis

3.13 Global consumer sentiment analysis

3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.2.2 Market Concentration Analysis

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Sustainability initiatives

4.4.6 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Million & Kilo Tons)

5.1 Key trends

5.2 Black

5.3 Grey

5.4 White

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Kilo Tons)

6.1 Key trends

6.2 Sheets

6.3 Trays & clamshells

6.4 Foam coolers

6.5 Cups & bowls

6.6 Packaging peanuts

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Kilo Tons)

7.1 Key trends

7.2 Food and beverages

7.2.1 Black

7.2.2 Grey

7.2.3 White

7.3 Foodservice

7.3.1 Black

7.3.2 Grey

7.3.3 White

7.4 Healthcare

7.4.1 Black

7.4.2 Grey

7.4.3 White

7.5 Electronics and electrical appliances

7.5.1 Black

7.5.2 Grey

7.5.3 White

7.6 Building and constructions

7.6.1 Black

7.6.2 Grey

7.6.3 White

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million & Kilo Tons)