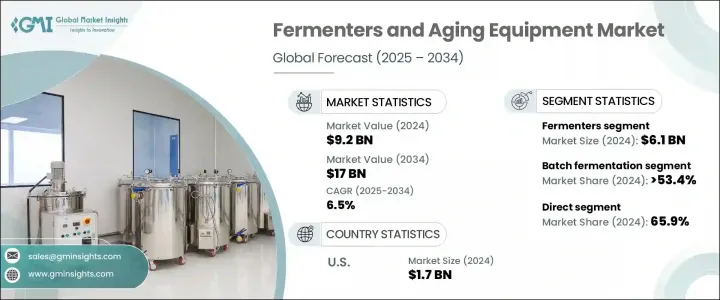

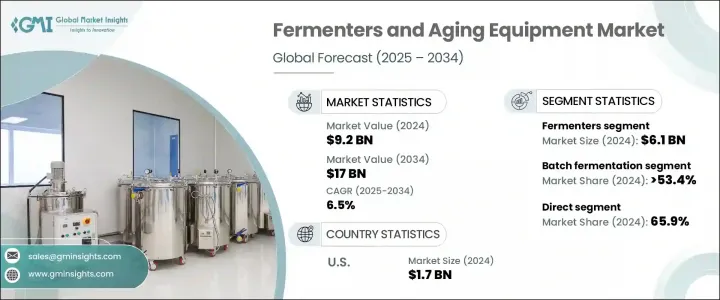

세계의 발효조 및 숙성 장비 시장 규모는 2024년에 92억 달러로 평가되었고, CAGR 6.5%를 나타내 2034년에는 170억 달러에 이를 것으로 추정되고 있습니다.

이 시장 성장의 원동력은 발효와 숙성 과정에 의존하는 여러 산업에 걸친 수요 증가입니다. 최첨단 발효 시스템에 대한 요구는 생물제제, 단일클론항체, 백신 등 수요가 높아지고 있는 바이오의약품 분야의 진보가 주요 요인이 되어 높아지고 있습니다. 건강 관리에 대한 세계 투자 확대와 만성 질환의 급증은 효율적이고 오염되지 않은 발효 과정에 대한 추가 주력을 촉진하고 있습니다.

자동화 시스템이나 일회용 발효조 등의 기술의 채용에 의해 오퍼레이션이 합리화되어, 생산 성과가 향상하고 있습니다. 이와 병행하여, 식품 및 식품 산업은 고품질의 자연 가공 제품의 인기 덕분에 장비의 노후화를 계속 추진하고 있습니다. 지속가능성과 자연식품 가공에 대한 관심도 커다란 촉매이며, 다양한 제조 셋업에 발효와 숙성 기술을 모두 통합할 것을 촉구하고 있습니다. APAC 등의 신흥경제권도 현대발효조술의 전개를 지원하는 산업화의 진전과 인프라의 개선에 의해 중요한 역할을 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 92억 달러 |

| 예측 금액 | 170억 달러 |

| CAGR | 6.5% |

발효조는 여러 산업 분야에서 널리 사용되고 있기 때문에 시장 전체를 계속 지배하고 있습니다. 이러한 시스템은 생물학적 제제, 효소, 치료 화합물, 발효 식품의 생산에 필수적인 미생물 및 세포 배양 배양에 중요한 역할을 합니다. 그 용도는 일반적으로 범위가 제한되는 에이징 장치와 비교할 때 훨씬 광범위합니다. 정밀하고 확장 가능한 생산에 대한 수요가 증가함에 따라 제조업체는 차세대 발효조 개발에 적극적으로 투자하고 있습니다. 이러한 시스템에는 향상된 모니터링, 자동화, 내오염성 등의 기능이 내장되어 있습니다. 보다 높은 효율성과 적응성을 가능하게 하는 이러한 혁신은 특히 제품의 일관성과 순도가 중요한 분야에서 생산자가 시장의 요구에 신속하게 대응할 수 있도록 합니다.

2024년에는 배치 발효 부문이 53.4%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR)은 7.3%를 나타낼 것으로 예측됩니다. 이 발효 방법은 조작의 간편성과 광범위한 적응성 때문에 바이오 의약품 산업과 식품 산업 모두에서 가장 선호되고 있습니다. 배치 처리는 성분의 첨가, 처리 및 제거를 제어된 환경에서 수행할 수 있어 다양한 제품 카테고리에 이상적인 간단한 설정을 제공합니다. 이 기술은 정밀도, 유연성 및 깨끗한 처리가 최우선으로 되는 중소규모 생산에 특히 적합합니다. 연속 생산과 대규모 생산과 같은 복잡성 없이 세밀한 모니터링이 필요한 고가치 제품의 제조를 지원합니다.

미국의 발효조 및 숙성 장비 시장은 67.7%의 점유율을 차지했으며 2024년에는 17억 달러를 창출했습니다. 이 나라의 이점은 고급 의약품 제조 환경, 정교한 연구시설, 강력한 공급업체 네트워크로 인해 발생합니다. 생물 제제와 개인화 치료 시장이 급속히 발전함에 따라 대규모 제조업체와 개발 위탁 기관 모두에서 보다 정교한 발효 솔루션에 대한 관심이 높아지고 있습니다. 미국은 의약품 생산과 혁신을 향상시키기 위한 공공 부문과 민간부문의 지속적인 투자의 혜택을 계속 받고 있습니다.

Thermo Fisher Scientific, Alfa Laval AB, Sartorius AG, Merck KGaA(MilliporeSigma), GEA Group AG 등 주요 시장 선수들은 전략적 노력을 통해 경쟁 구도를 적극적으로 형성하고 있습니다. 이러한 기업들은 바이오프로세스와 식품업계의 진화하는 요구에 대응하는 보다 스마트하고 모듈화된 확장 가능한 시스템을 도입하기 위한 연구개발을 우선하고 있습니다. 또한 각 지역의 제조 거점, 현지화된 서비스 센터, 전략적인수를 통해 세계적인 발자취를 확대하고 있습니다. 학술기관이나 바이오의약품기업과의 제휴는 이들 기업이 시장의 변화를 선점하고 신기술을 신속하게 시험·전개하는 데 도움이 되고 있습니다. 제품 성능 향상, 자동화 진전, 통합 디지털 솔루션 제공으로 이 기업들은 시장에서의 입지를 강화하고 유연하고 효율적인 가공 기술에 대한 수요에 부응하고 있습니다.

The Global Fermenters and Aging Equipment Market was valued at USD 9.2 billion in 2024 and is estimated to grow at a CAGR of 6.5% to reach USD 17 billion by 2034. This market growth is fueled by the increasing demand across multiple industries that rely on fermentation and aging processes. The need for cutting-edge fermentation systems is rising, driven largely by advancements in the biopharmaceutical sector, where biologics, monoclonal antibodies, and vaccines are seeing heightened demand. Growing investments in healthcare globally and a surge in chronic disease prevalence are prompting further focus on efficient and contamination-free fermentation processes.

The adoption of technologies such as automated systems and single-use fermenters has streamlined operations and improved production outcomes. Alongside, the food and beverage industry continue to push growth in aging equipment, thanks to the popularity of high-quality, naturally processed products. Interest in sustainability and natural food processing is another major catalyst, encouraging the integration of both fermentation and aging technologies across various manufacturing setups. Emerging economies in regions such as APAC are also playing a key role due to increased industrialization and infrastructure improvements that support the deployment of modern fermentation technologies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.2 Billion |

| Forecast Value | $17 Billion |

| CAGR | 6.5% |

Fermenters continue to dominate the overall market, owing to their wide-ranging usage across several industrial verticals. These systems play a crucial role in cultivating microorganisms and cell cultures essential for producing biologics, enzymes, therapeutic compounds, and fermented food items. Their applications are far more extensive when compared to aging equipment, which is generally more limited in scope. As demand for precision-driven and scalable production intensifies, manufacturers are actively investing in the development of next-generation fermenters. These systems incorporate features such as enhanced monitoring, automation, and contamination resistance. By enabling higher efficiency and adaptability, these innovations are making it easier for producers to respond quickly to market needs, especially in sectors where product consistency and purity are critical.

In 2024, the batch fermentation segment held a 53.4% share and is projected to grow at a CAGR of 7.3% through 2034. This fermentation method remains the most preferred across both biopharma and food industries because of its operational simplicity and broad adaptability. Batch processing allows ingredients to be added, processed, and removed in a controlled environment, offering a straightforward setup ideal for a variety of product categories. This technique is particularly well-suited to small- to medium-scale production runs, where precision, flexibility, and clean processing are paramount. It supports the manufacturing of high-value products that require detailed oversight without the complications of continuous or large-scale operations.

United States Fermenters and Aging Equipment Market held a 67.7% share and generated USD 1.7 billion in 2024. The country's dominance stems from its advanced pharmaceutical manufacturing landscape, sophisticated research facilities, and strong supplier networks. A rapidly evolving market for biologics and personalized therapies is fueling interest in more advanced fermentation solutions across both large-scale manufacturers and contract development organizations. The US continues to benefit from sustained public and private sector investments aimed at improving pharmaceutical output and innovation.

Key market players, including Thermo Fisher Scientific, Alfa Laval AB, Sartorius AG, Merck KGaA (MilliporeSigma), and GEA Group AG, are actively shaping the competitive landscape through strategic efforts. These firms are prioritizing research and development to introduce smarter, modular, and scalable systems that meet the evolving needs of bioprocessing and food industries. They are also expanding their global footprint through regional manufacturing hubs, localized service centers, and strategic acquisitions. Partnerships with academic institutions and biopharma companies help these players stay ahead of market shifts and rapidly test and deploy new technologies. By enhancing product performance, increasing automation, and offering integrated digital solutions, these companies are solidifying their market positions and responding to the demand for flexible and efficient processing technologies.