위성 기반 지구 관측 시장 :시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Satellite-Based Earth Observation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1797753

리서치사:Global Market Insights Inc.

발행일:2025년 07월

페이지 정보:영문 170 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

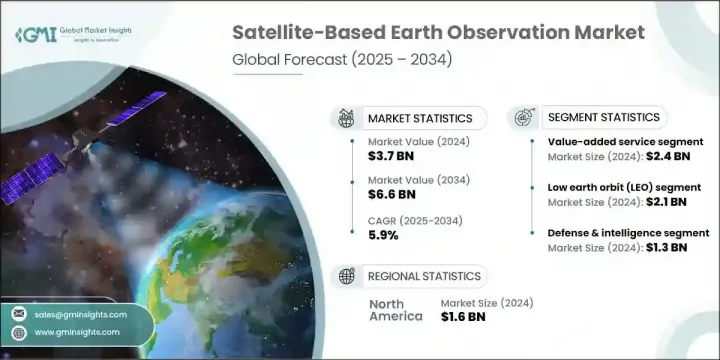

세계의 위성 기반 지구 관측 시장은 2024년에는 37억 달러로 평가되었으며 CAGR 5.9%를 나타내 2034년에는 66억 달러에 이를 것으로 예측됩니다.

기후 모니터링, 국가 안보, 환경 응용 분야에서 지리 공간 정보에 대한 의존도가 높아짐에 따라 일관된 수요가 이어지고 있습니다. 위성의 소형화와 배포 비용 절감의 진보는 소형 위성의 배치를 크게 뒷받침하고 있습니다. 이러한 소형 플랫폼은 농업, 방위, 재해 대응 등 다양한 분야에 비용 효율적인 고해상도 데이터를 제공합니다. 인공지능과 클라우드 컴퓨팅은 원시 위성 이미지를 실용적인 데이터로 변환하는 데 있어 매우 중요한 역할을 하여 산업계와 정부 기관의 의사결정을 강화하고 있습니다. 또한 기후 패턴 모니터링, 도시 성장 최적화, 자연재해 내성 향상을 목표로 하는 세계적 노력으로 수요도 높아지고 있습니다.

정밀도 향상, 데이터 전달 사이클 단축, 정교한 분석 플랫폼에 대한 간편한 액세스가 시장을 뒷받침하고 지속적으로 지상 상황을 거의 실시간으로 파악할 수 있게 되었습니다. 이러한 개선으로 데이터 수집부터 실용적인 의사결정까지의 시간이 크게 단축되어 농업, 환경보전, 도시계획, 긴급관리 등 분야의 이해관계자가 보다 효과적으로 대응할 수 있게 되었습니다. 인공위성 데이터를 AI 및 머신러닝과 통합함으로써 미묘한 환경 변화를 감지하고, 인프라를 모니터링하고, 작물의 건강 상태를 평가하고, 삼림 벌채와 오염을 전례 없는 정확도로 추적하는 능력이 더욱 높아지고 있습니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

당초 시장 규모

37억 달러

시장 규모 예측

66억 달러

CAGR

5.9%

부가가치 서비스 분야는 2024년 24억 달러를 창출했습니다. 이 성장은 위성 데이터에서 얻은 맞춤형 분석에 대한 요구가 증가하고 있습니다. 이러한 인사이트력은 인프라, 에너지, 스마트 시티, 농업과 같은 주요 부문에서 더 스마트한 계획과 운영을 지원합니다. AI를 탑재한 플랫폼 개발 및 분석 제산업체와의 제휴는 환경 추적 및 도시 개발과 같은 분야에서 보다 구체적인 솔루션을 가능하게 합니다. 통합 플랫폼을 통해 애널리틱스에 대한 액세스가 간소화됨에 따라 특히 빠르고 직관적이며 신뢰할 수 있는 정보 제공 시스템을 요구하는 사용자 간에 배포가 진행됩니다.

저궤도(LEO) 부문은 2024년 21억 달러로 평가되었습니다. 소형 위성과 컴팩트한 CubeSats의 상승은 이러한 플랫폼이 고해상도 비주얼과 신속한 재방문 간격을 제공하기 때문에 이러한 성장에 기여합니다. 빈번한 이미징은 토지 이용 매핑, 농작물 건강 추적, 긴급 대응 등의 용도를 지원합니다. 발사 제산업체와 위성 회사의 협력으로 접근성이 향상되고 운영 비용이 절감되었습니다. 이러한 장점은 특히 방위, 지속가능성, 환경 모니터링 분야에서 상세하고 지속적으로 관측할 수 있는 지구관측에 대한 상업적 및 사회적 관심의 확대를 가속화하고 있습니다.

2024년 미국의 위성 기반 지구 관측 시장 규모는 13억 8,000만 달러로 평가되었습니다. 이 리더십은 위성 기술 혁신과 국가 안보 기술에 대한 대규모 투자로 인한 것입니다. 기업은 재해 대비, 기후 데이터 수집, 전략 모니터링 등 진화하는 요구에 맞게 제품을 제공해야 합니다. AI를 활용한 데이터 분석, 클라우드 기반의 제공 모델, 안전한 통신 시스템의 통합을 중시함으로써 미래의 정부 계약과 경쟁과의 계약에서 경쟁력을 유지하려는 벤더의 포지셔닝이 더욱 강화됩니다.

세계의 위성 기반 지구 관측 시장 주요 진출기업은 Planet Labs PBC, MinoSpace, GeoOptics Inc., ICEYE Oy, Capella Space Inc., OroraTech GmbH, Airbus Defence and Space, Spire Global, Inc., ImageSat International NV, Maxar Technologies Inc., BlackSky Tec. Inc., China Siwei Surveying and Mapping Technology Co. 등이 있습니다. 위성 기반 지구 관측 시장에서의 존재를 강화하기 위해, 각 회사는 보다 지능적인 데이터 분석을 위한 AI 및 머신러닝 알고리즘의 통합에 주력하고 있습니다. 많은 기업들이 분석회사와 파트너십을 맺고, 방위, 농업, 환경 모니터링 등 특정 업계에 맞는 커스터마이즈 서비스를 공동 개발하고 있습니다. 소형 위성의 별자리를 확장하면 보다 넓은 커버리지와 더 빈번한 데이터 수집이 가능합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

파괴적 혁신

생태계 분석

업계에 미치는 영향요인

성장 촉진요인

지리공간 데이터에 대한 수요 증가

기후 변화 감시

정부 및 방위 응용

클라우드 컴퓨팅과 AI 분석의 보급

위성의 소형화의 진보

함정과 과제

고액의 초기 투자와 시작 비용

궤도상의 파편과 우주의 혼잡

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

새로운 비즈니스 모델

컴플라이언스 요건

국방예산 분석

세계의 방위비의 동향

지역 방위 예산 배분

북미

유럽

아시아태평양

중동 및 아프리카

라틴아메리카

주요 방위 근대화 프로그램

예산 예측(2025-2034년)

업계의 성장에 미치는 영향

국가별 방위 예산

공급 체인의 탄력

지정학적 분석

인재 분석

디지털 변혁

합병, 인수, 전략적 제휴의 상황

위험 평가 및 관리

주요 계약 체결(2021-2024년)

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

시장 집중 분석

주요 기업의 경쟁 벤치마킹

재무실적의 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업의 넓이

기술

파괴적 혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

리더

챌린저

팔로워

틈새 기업

전략적 전망 매트릭스

주요 동향(2021-2024년)

기업 합병·인수(M&A)

사업 제휴 및 협력

기술진보

확대 및 투자 전략

지속가능성에 대한 노력

디지털 변혁의 대처

신흥기업/스타트업기업경쟁 구도

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

주요 동향

EO 데이터

광학 이미징 데이터

레이더 이미징 데이터

초분광 이미징 데이터

열적외선 영상 데이터

기타

부가가치 서비스

분석 및 인사이트 서비스

지리공간 인텔리전스 플랫폼

기타

제6장 시장 추계·예측 : 위성 궤도별(2021-2034년)

주요 동향

저궤도(LEO)

중궤도(MEO)

정지궤도(GEO)

제7장 시장 추계·예측 : 기술별(2021-2034년)

주요 동향

광학(전기 광학)

합성 개구 레이더(SAR)

초분광 및 다중 스펙트럼

열적외선 센서

LiDAR 시스템

기타

제8장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

농업 및 임업

국방 및 정보

환경 및 기후 모니터링

도시 및 인프라 계획

에너지, 광업 및 천연자원

해양 및 운송

기타

제9장 시장 추계·예측 : 최종 용도별(2021-2034년)

주요 동향

정부 및 방위

군사 및 정보 기관

민간정부 및 공공안전부문

상업용

농업 및 임업 기업

환경 서비스 제산업체

건설 및 도시계획회사

에너지 및 광업회사

해운 사업자

기타

연구 및 학계

기타

제10장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제11장 기업 프로파일

세계 주요 기업

각 지역의 주요 기업

파괴적 혁신/틈새 기업

Capella Space Inc.

Pixxel Inc

OroraTech GmbH

UrtheCast Corp.

GeoOptics Inc.

KTH

영문 목차

영문목차

The Global Satellite-Based Earth Observation Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 5.9% to reach USD 6.6 billion by 2034. Increasing reliance on geospatial intelligence for climate surveillance, national security, and environmental applications is driving consistent demand. Advancements in satellite miniaturization and lower deployment costs have significantly boosted the deployment of smaller satellites. These compact platforms deliver cost-effective, high-resolution data across several sectors, including agriculture, defense, and disaster response. Artificial intelligence and cloud computing play a pivotal role in transforming raw satellite imagery into actionable data, thereby enhancing decision-making for industries and governments alike. Demand is also rising due to global efforts aimed at monitoring climate patterns, optimizing urban growth, and improving resilience to natural disasters.

Enhanced accuracy, shorter data delivery cycles, and easy access to sophisticated analytics platforms continue to push the market forward, enabling near real-time insights into Earth's surface conditions. These improvements are drastically reducing the time between data collection and actionable decision-making, allowing stakeholders in sectors such as agriculture, environmental conservation, urban planning, and emergency management to respond more effectively. The integration of satellite data with AI and machine learning has further amplified the ability to detect subtle environmental changes, monitor infrastructure, assess crop health, and track deforestation or pollution with unprecedented precision.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$3.7 billion

Forecast Value

$6.6 billion

CAGR

5.9%

The value-added services segment generated USD 2.4 billion in 2024. This growth is tied to the increasing requirement for customized analysis derived from satellite data. These insights support smarter planning and operations in key sectors such as infrastructure, energy, smart cities, and agriculture. Integration of AI-powered platforms and partnerships with analytics providers allows for more specific solutions in areas like environmental tracking and city development. Simplified access to analytics through unified platforms increases adoption, especially among users seeking fast, intuitive, and reliable information delivery systems.

The low Earth orbit (LEO) segment was valued at USD 2.1 billion in 2024. The rise of small satellites and compact CubeSats contributes to this growth, as these platforms deliver high-resolution visuals and rapid revisit intervals. Frequent imaging supports applications such as land use mapping, crop health tracking, and emergency response. Collaboration between launch providers and satellite firms has improved access and reduced operational costs. These advantages have accelerated the expansion of commercial and public interest in detailed, constant Earth observation, especially across defense, sustainability, and environmental monitoring initiatives.

United States Satellite-Based Earth Observation Market generated USD 1.38 billion in 2024. This leadership stems from large-scale investment in satellite innovation and national security technologies. Companies must align their product offerings with evolving needs in disaster readiness, climate data gathering, and strategic surveillance. Emphasis on integrating AI-driven data analysis, cloud-based delivery models, and secure communications systems will further enhance the positioning of vendors seeking to remain competitive in future government contracts and commercial engagements.

Key participants in the Global Satellite-Based Earth Observation Market include Planet Labs PBC, MinoSpace, GeoOptics Inc., ICEYE Oy, Capella Space Inc., OroraTech GmbH, Airbus Defence and Space, Spire Global, Inc., ImageSat International N.V., Maxar Technologies Inc., BlackSky Technology Inc., LiveEO GmbH, L3Harris Technologies Inc., China Siwei Surveying and Mapping Technology Co., Ltd., and MDA Space Ltd. To strengthen their presence in the satellite-based Earth observation market, companies are focusing on integrating AI and machine learning algorithms for more intelligent data interpretation. Many are forming partnerships with analytics firms to co-develop customized services tailored to specific industries like defense, agriculture, and environmental monitoring. Expanding constellations of smaller satellites enables broader coverage and more frequent data collection.

Table of Contents

Chapter 1 Methodology and scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Product type trends

2.2.2 Satellite orbit trends

2.2.3 Technology trends

2.2.4 Application trends

2.2.5 End use trends

2.2.6 Regional trends

2.3 TAM Analysis, 2025-2034 (USD Billion)

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry ecosystem analysis

3.3 Industry impact forces

3.3.1 Growth drivers

3.3.1.1 Increasing demand for geospatial data

3.3.1.2 Climate change monitoring

3.3.1.3 Government and defense applications

3.3.1.4 Proliferation of cloud computing and AI analytics

3.3.1.5 Advancements in satellite miniaturization

3.3.2 Pitfalls and challenges

3.3.2.1 High Initial Investment and Launch Costs

3.3.2.2 Orbital Debris and Space Congestion

3.4 Growth potential analysis

3.5 Regulatory landscape

3.5.1 North America

3.5.2 Europe

3.5.3 Asia Pacific

3.5.4 Latin America

3.5.5 Middle East & Africa

3.6 Porter's analysis

3.7 PESTEL analysis

3.8 Technology and Innovation landscape

3.8.1 Current technological trends

3.8.2 Emerging technologies

3.9 Emerging business models

3.10 Compliance requirements

3.11 Defense budget analysis

3.12 Global defense spending trends

3.13 Regional defense budget allocation

3.13.1 North America

3.13.2 Europe

3.13.3 Asia Pacific

3.13.4 Middle East and Africa

3.13.5 Latin America

3.14 Key defense modernization programs

3.15 Budget forecast (2025-2034)

3.15.1 Impact on industry growth

3.15.2 Defense budgets by country

3.16 Supply chain resilience

3.17 Geopolitical analysis

3.18 Workforce analysis

3.19 Digital transformation

3.20 Mergers, acquisitions, and strategic partnerships landscape

3.21 Risk assessment and management

3.22 Major contract awards (2021-2024)

Chapter 4 Competitive landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.2.2 Market Concentration Analysis

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Sustainability initiatives

4.4.6 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market estimates and forecast, By Product Type, 2021 - 2034 (USD Million)

5.1 Key trends

5.2 EO Data

5.2.1 Optical imaging data

5.2.2 Radar imaging data

5.2.3 Hyperspectral imaging data

5.2.4 Thermal infrared imaging data

5.2.5 Others

5.3 Value-added services

5.3.1 Analytics & Insight Services

5.3.2 Geospatial Intelligence Platforms

5.3.3 Others

Chapter 6 Market estimates and forecast, By Satellite Orbit, 2021 - 2034 (USD Million)

6.1 Key trends

6.2 Low earth orbit (LEO)

6.3 Medium earth orbit (MEO)

6.4 Geostationary orbit (GEO)

Chapter 7 Market estimates and forecast, By Technology, 2021 - 2034 (USD Million)

7.1 Key trends

7.2 Optical (electro-optical)

7.3 Synthetic aperture radar (SAR)

7.4 Hyperspectral & multispectral

7.5 Thermal infrared sensors

7.6 LiDAR systems

7.7 Others

Chapter 8 Market estimates and forecast, By Application, 2021 - 2034 (USD Million)

8.1 Key trends

8.2 Agriculture & forestry

8.3 Defense & intelligence

8.4 Environmental & climate monitoring

8.5 Urban & infrastructure planning

8.6 Energy, mining & natural resources

8.7 Maritime & transportation

8.8 Others

Chapter 9 Market estimates and forecast, By End Use, 2021 - 2034 (USD Million)

9.1 Key trends

9.2 Government & defense

9.2.1 Military & intelligence agencies

9.2.2 Civil government & public safety departments

9.3 Commercial

9.3.1 Agribusiness & forestry companies

9.3.2 Environmental service providers

9.3.3 Construction & urban planning firms

9.3.4 Energy & mining companies

9.3.5 Maritime logistics operators

9.3.6 Others

9.4 Research & academia

9.5 Others

Chapter 10 Market estimates and forecast, By Region, 2021 - 2034 (USD Million)

10.1 Key trends

10.2 North America

10.2.1 U.S.

10.2.2 Canada

10.3 Europe

10.3.1 Germany

10.3.2 UK

10.3.3 France

10.3.4 Spain

10.3.5 Italy

10.3.6 Netherlands

10.4 Asia Pacific

10.4.1 China

10.4.2 India

10.4.3 Japan

10.4.4 Australia

10.4.5 South Korea

10.5 Latin America

10.5.1 Brazil

10.5.2 Mexico

10.5.3 Argentina

10.6 Middle East and Africa

10.6.1 Saudi Arabia

10.6.2 South Africa

10.6.3 UAE

Chapter 11 Company profiles

11.1 Global Key Players

11.1.1 Maxar Technologies Inc.

11.1.2 Airbus Defence and Space

11.1.3 Planet Labs PBC

11.1.4 ImageSat International N.V.

11.1.5 Spire Global Inc

11.2 Regional Key Players

11.2.1 North America

11.2.1.1 BlackSky Technology Inc.

11.2.1.2 L3Harris Technologies Inc

11.2.1.3 MDA Space Ltd.

11.2.2 Europe

11.2.2.1 LiveEO GmbH

11.2.2.2 Satellite Vu Ltd.

11.2.2.3 ICEYE Oy

11.2.3 Asia-Pacific

11.2.3.1 SpaceWill Information Co., Ltd.

11.2.3.2 MinoSpace

11.2.3.3 XRTech Group

11.2.3.4 China Siwei Surveying and Mapping Technology Co., Ltd.