국소 약물 포장 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

Topical Drugs Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1797703

리서치사:Global Market Insights Inc.

발행일:2025년 07월

페이지 정보:영문 180 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

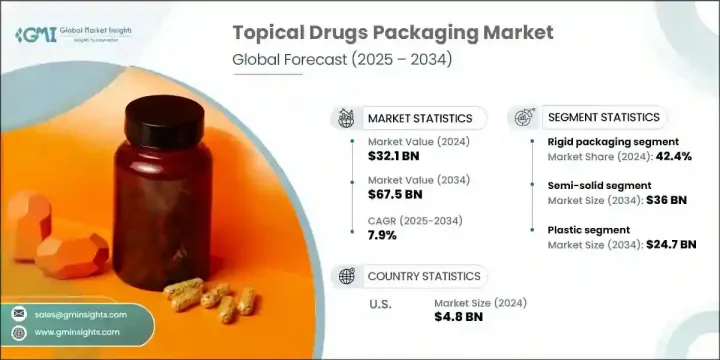

세계의 국소 약물 포장 시장은 2024년에 321억 달러로 평가되어 CAGR 7.9%로 성장할 전망이며 2034년에는 675억 달러에 이를 것으로 추정되고 있습니다.

피부 질환 증가와 소비자 직판 채널(특히 온라인) 확대가 주요 성장 촉진 요인으로 작용하고 있습니다. 전자상거래의 급성장은 의약품사들, 특히 국소 약물를 제공하는 기업들이 더 넓은 고객층에 직접 접근할 수 있는 새로운 길을 열었습니다.

여드름, 습진, 건선과 같은 피부 질환이 점점 더 흔해짐에 따라 의약품사들은 접근성이 높고 효과적인 국소 약물에 더 집중하고 있으며, 이는 결과적으로 안전하고 혁신적인 포장재에 대한 수요를 촉진합니다. QR 코드 검증, 변조 방지 실링, 추적 기능 등 디지털 기술의 포장 적용은 고가 및 일반의약품 피부과 제품에서 확산되고 있다. 지속가능성은 포장 선택을 지속적으로 재편하고 있다. 시장 업체들은 재활용 플라스틱, 리필 시스템, 생분해성 필름 등 친환경 솔루션을 통합하며 변화하는 소비자 및 규제 기대를 반영하고 있다. 이러한 지속가능한 포장 혁신은 환경적 영향을 줄일 뿐만 아니라 브랜드 평판과 소비자 신뢰도 향상에도 기여하고 있습니다. 기업들은 제품 수명 주기 전반에 걸쳐 폐기물을 최소화하는 경량화 및 자원 효율적 소재 개발에 점점 더 많은 투자를 하고 있습니다. 재활용 용이성을 위한 단일 소재 구조 사용과 탄소 발자국을 줄인 포장 공정이 업계 전반에 걸쳐 보편화되고 있습니다. 또한 사용된 포장을 수거하여 새 제품으로 재가공하는 폐쇄형 시스템에 대한 요구도 증가하고 있습니다. 이러한 노력은 전 세계 지속가능성 목표와 부합하는 동시에 윤리적이고 환경적으로 책임 있는 헬스케어 솔루션에 대한 증가하는 수요를 충족시키고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

321억 달러

예측 금액

675억 달러

CAGR

7.9%

2024년 기준 경질 포맷 부문은 42.4%의 점유율을 차지했습니다. 병, 유리 용기, 항아리 등은 보호 기능 제공, 제품 품질 보존, 저장 안정성 지원 측면에서 프리미엄 및 처방용 피부 치료제에 널리 사용됩니다. 특히 점성 제형 처리 능력과 민감한 용도에 대한 구조적 무결성 유지 능력으로 선호됩니다.

액체 제품 부문은 2025년부터 2034년까지 연평균 7.9%의 성장률을 보일 것으로 전망됩니다. 방부제 및 약용 스프레이를 포함한 액체 제품은 유출 및 오염을 방지하면서 유효 성분 보존과 투여 정확도를 지원하는 정밀하고 안전한 포장이 필요합니다.

북미의 국소 약물 포장 시장은 2024년 37.6%의 점유율을 기록했으며, 2025년부터 2034년까지 연평균 6.9%의 성장률을 보일 것으로 예상됩니다. 강력한 의약품 인프라, 일반의약품(OTC) 선호도, 증가하는 자가 관리 습관이 이 지역의 포장 혁신을 주도하고 있습니다. 전자상거래에 대한 의존도 증가와 안전성 및 규정 준수를 보장하는 사용자 친화적 포장이 미국과 캐나다의 수요 미래를 지속적으로 형성하고 있습니다.

국소 약물 포장 시장의 주요 기업으로는 West Pharmaceutical Services, Schott, AptarGroup, Gerresheimer, Amcor 등이 있습니다. 국소 약물 포장 기업들은 소비자와 제약 고객 모두의 변화하는 요구를 충족시키기 위해 지속 가능한 소재, 디지털 보안, 고급 분사 시스템에 대한 투자를 확대하고 있습니다. 브랜드들은 환경 규제와 소비자 선호에 부응하기 위해 재충전 가능 용기, 생분해성 포장 필름, 저탄소 제조 기술로 혁신을 추진하고 있습니다. 변조 방지 캡, 인체공학적 디자인, 추적성과 소비자 신뢰도를 높이는 일련화 기술 등을 통해 제품 차별화가 강화되고 있습니다. 기업들은 또한 전문 피부과 제품에 맞춤화된 포장 형식을 공동 개발하기 위해 의약품 제조사와 전략적 파트너십을 구축하고 있습니다.

목차

제1장 조사 방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역 및 국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

1차 정보

예측 모델

조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 촉진요인

성장 촉진요인

피부 질환 및 피부과 질환의 유병률 상승

편리하고 사용자 친화적인 포장 형태에 대한 수요 증가

일반의약품(OTC) 국소 의약품 제품 확대

전자상거래와 소비자 직접 판매 의약품 판매 성장

단위 용량 및 제어 투여 시스템에서의 혁신

업계의 잠재적 위험 및 과제

엄격한 규제 준수 및 승인 절차

어린이 및 노인 친화적인 포장 설계의 복잡성

시장 기회

피부과적 수요가 충족되지 않은 신흥 시장으로 확장

인증 및 환자 참여를 위한 스마트 포장 기술 통합

지속가능하고 생분해성 포장 솔루션에 대한 투자 증가

소매 약국 체인에 의한 자사 브랜드 국소 제품 라인 성장

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

가격 동향

과거 가격 분석(2021-2024년)

가격 동향 요인

지역별 가격 차이

가격 예측(2025-2034년)

가격 전략

새로운 비즈니스 모델

규정 준수 요건

지속가능성 대책

지속 가능한 재료의 평가

탄소발자국 분석

순환형 경제의 실현

지속가능성 인증 및 기준

지속가능성 ROI 분석

세계 소비자 감정 분석

특허 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 기업의 경쟁 벤치마킹

재무실적의 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업의 넓이

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전(2021-2024년)

합병과 인수

파트너십 및 협업

기술적 진보

확대 및 투자 전략

지속가능성에 대한 노력

디지털 변혁의 대처

신흥기업 및 스타트업기업경쟁 구도

제5장 시장 추계 및 예측, 포장 형태별(2021-2034년)

주요 동향

연포장

경질 포장

반경질 포장

제6장 시장 추계 및 예측, 포장 재료별(2021-2034년)

주요 동향

플라스틱

유리

금속

종이

알루미늄

기타

제7장 시장 추계 및 예측, 상품 유형별(2021-2034년)

주요 동향

병

캡 및 클로저

흡입기

튜브

항아리

기타

제8장 시장 추계 및 예측, 약제 유형별(2021-2034년)

주요 동향

액체

반고체

고체

경피

제9장 시장 추계 및 예측, 클로저 유형별(2021-2034년)

주요 동향

스크류 캡

플립탑 캡

펌프 디스펜서

스포이드

노즐

제10장 시장 추계 및 예측, 투여 방법별(2021-2034년)

주요 동향

안과

비강

경피

제11장 시장 추계 및 예측, 용도별(2021-2034년)

주요 동향

피부과

안과

기타

제12장 시장 추계 및 예측, 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제13장 기업 프로파일

세계 주요 기업

Amcor

AptarGroup

Gerresheimer

Schott

West Pharmaceutical Services

지역의 주요 기업

북미

Catalent

WestRock

Sonoco Products

ProAmpac

Silgan Holdings

유럽

Bormioli Pharma

Constantia Flexibles

Mondi

SGD Pharma

아시아태평양

Huhtamaki

Nipro

EPL Limited

틈새 기업/혁신 기업

CCL Industries

LOG Pharma Primary Packaging

Nelipak

HBR

영문 목차

영문목차

The Global Topical Drugs Packaging Market was valued at USD 32.1 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 67.5 billion by 2034. Rising skin conditions and growing direct-to-consumer sales channels, particularly online, are among the primary growth drivers. The boom in e-commerce has opened new pathways for pharmaceutical companies, especially those offering topical solutions, to reach broader audiences directly.

With skin conditions like acne, eczema, and psoriasis becoming increasingly prevalent, pharmaceutical firms are focusing more on accessible and effective topical treatments, which in turn boosts demand for safe and innovative packaging. Digital tech adoption in packaging-such as QR verification, tamper-proof seals, and track-and-trace capabilities-is gaining traction in high-value and OTC dermatology products. Sustainability continues to reshape packaging choices. Market players are integrating eco-conscious solutions, including recyclable plastics, refill systems, and biodegradable films, reflecting shifting consumer and regulatory expectations in the pharmaceutical sector. These sustainable packaging innovations are not only helping reduce environmental impact but also enhancing brand reputation and consumer trust. Companies are increasingly investing in the development of lightweight, resource-efficient materials that minimize waste throughout the product lifecycle. The use of mono-material structures for easier recyclability, along with reduced carbon footprint packaging processes, is becoming more common across the industry. Additionally, there's a growing push for closed-loop systems, where used packaging is collected and reprocessed into new products. Such initiatives align with global sustainability goals while meeting the rising demand for ethical and environmentally responsible healthcare solutions.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$32.1 Billion

Forecast Value

$67.5 Billion

CAGR

7.9%

In 2024, the rigid formats segment held a 42.4% share. Bottles, glass containers, and jars are widely used for premium and prescription skin treatments as they offer protection, preserve product quality, and support storage stability. These containers are particularly favored for their ability to handle viscous formulations and maintain structural integrity for sensitive applications.

The liquid product segment is forecasted to grow at a CAGR of 7.9% from 2025 to 2034. Liquids, including antiseptics and medicated sprays, demand precise, secure packaging that prevents spills and contamination while supporting active ingredient preservation and dosing accuracy.

North America Topical Drugs Packaging Market held 37.6% share in 2024 and is set to grow at a CAGR of 6.9% throughout 2025-2034. Strong pharmaceutical infrastructure, a preference for OTC medication, and growing self-care habits are advancing packaging innovation in this region. Increased reliance on e-commerce and user-friendly packaging that ensures safety and compliance continues to shape the demand landscape in the US and Canada.

Leading companies in Topical Drugs Packaging Market include West Pharmaceutical Services, Schott, AptarGroup, Gerresheimer, and Amcor. Topical drug packaging companies are investing heavily in sustainable materials, digital security, and advanced dispensing systems to cater to the evolving needs of both consumers and pharmaceutical clients. Brands are innovating with refillable containers, biodegradable packaging films, and low-carbon manufacturing to align with environmental regulations and consumer preferences. Product differentiation is being enhanced through tamper-proof closures, ergonomic design, and serialization technologies that add traceability and consumer confidence. Companies are also forming strategic partnerships with pharmaceutical manufacturers to co-develop packaging formats tailored to specialized dermatological products.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Packaging type trends

2.2.2 Packaging material trends

2.2.3 Product types trends

2.2.4 Drug type trends

2.2.5 Closure type trends

2.2.6 Mode of administration trends

2.2.7 Application trends

2.2.8 Regional trends

2.3 TAM Analysis, 2025-2034 (USD Million)

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Rising prevalence of skin diseases and dermatological disorders

3.2.1.2 Growing demand for convenient and user-friendly packaging formats

3.2.1.3 Expansion of over-the-counter (OTC) topical drug products

3.2.1.4 Growth of e-commerce and direct-to-consumer pharmaceutical sales

3.2.1.5 Innovation in unit dose and controlled-dispensing systems

3.2.2 Industry pitfalls and challenges

3.2.2.1 Stringent regulatory compliance and approval processes

3.2.2.2 Complexities in designing child-resistant yet senior-friendly packaging

3.2.3 Market opportunities

3.2.3.1 Expansion into emerging markets with underserved dermatological needs.

3.2.3.2 Integration of smart packaging technologies for authentication and patient engagement.

3.2.3.3 Rising investment in sustainable and biodegradable packaging solutions.

3.2.3.4 Growth of private-label topical product lines by retail pharmacy chains.

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Price trends

3.8.1 Historical price analysis (2021-2024)

3.8.2 Price trend drivers

3.8.3 Regional price variations

3.8.4 Price Forecast (2025-2034)

3.9 Pricing strategies

3.10 Emerging business models

3.11 Compliance requirements

3.12 Sustainability measures

3.12.1 Sustainable materials assessment

3.12.2 Carbon footprint analysis

3.12.3 Circular economy implementation

3.12.4 Sustainability certifications and standards

3.12.5 Sustainability ROI Analysis

3.13 Global consumer sentiment analysis

3.14 Patent analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Sustainability initiatives

4.4.6 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Packaging Type, 2021 - 2034 (USD Million & Kilo Tons)

5.1 Key trends

5.2 Flexible packaging

5.3 Rigid packaging

5.4 Semi-rigid packaging

Chapter 6 Market Estimates and Forecast, By Packaging Material, 2021 - 2034 (USD Million & Kilo Tons)

6.1 Key trends

6.2 Plastic

6.3 Glass

6.4 Metal

6.5 Paper

6.6 Aluminium

6.7 Others

Chapter 7 Market Estimates and Forecast, By Product Types, 2021 - 2034 (USD Million & Kilo Tons)

7.1 Key trends

7.2 Bottles

7.3 Caps & closures

7.4 Inhalers

7.5 Tubes

7.6 Jars

7.7 Others

Chapter 8 Market Estimates and Forecast, By Drug Type, 2021 - 2034 (USD Million & Kilo Tons)

8.1 Key trends

8.2 Liquid

8.3 Semi-solid

8.4 Solid

8.5 Transdermal

Chapter 9 Market Estimates and Forecast, By Closure Type, 2021 - 2034 (USD Million & Kilo Tons)

9.1 Key trends

9.2 Screw cap

9.3 Flip-top cap

9.4 Pump dispenser

9.5 Dropper

9.6 Nozzle

Chapter 10 Market Estimates and Forecast, By Mode of Administration, 2021 - 2034 (USD Million & Kilo Tons)

10.1 Key trends

10.2 Ophthalmic usage

10.3 Nasal usage

10.4 Dermal usage

Chapter 11 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Million & Kilo Tons)

11.1 Key trends

11.2 Dermatology

11.3 Ophthalmology

11.4 Others

Chapter 12 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Kilo Tons)