전자상거래용 내열 포장 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)

E-Commerce Heat-Resistant Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1797693

리서치사:Global Market Insights Inc.

발행일:2025년 07월

페이지 정보:영문 185 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

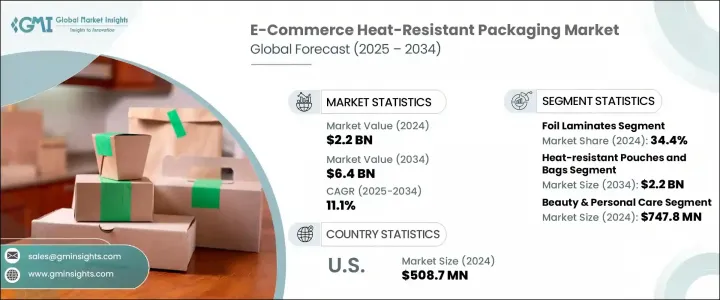

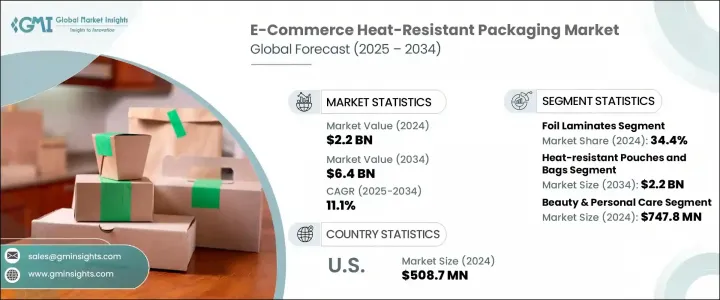

세계의 전자상거래용 내열 포장 시장 규모는 2024년에 22억 달러가 되고, CAGR 11.1%로 성장할 전망이며 2034년에는 64억 달러에 이를 것으로 예측되고 있습니다.

시장 확대는 주로 전자상거래의 지속적인 성장과 의약품 산업에서 열 보호에 대한 수요 증가에 의해 촉진되고 있습니다. 온라인 구매와 국제 배송이 급증함에 따라 다양한 온도 조건에서도 제품의 무결성을 유지할 수 있는 포장재에 대한 수요가 상당한 증가를 보였습니다. 소비자들은 특히 식품, 퍼스널 케어, 온도에 민감한 전자제품의 안전한 배송과 관련해 신뢰성과 지속가능성을 추구하고 있습니다. 포장 솔루션은 이제 단열 기능뿐만 아니라 최근 소비자의 기대에 부응하는 친환경적이어야 합니다. 가정 내 의료 서비스 증가와 제약 공급업체의 디지털화 확대는 단열 포장 수요에 성장세를 제공하고 있습니다.

생물학적 제제 및 인슐린과 같은 중요 제품의 규제 준수 및 온도 관리 역시 운송 중 안전한 배송을 위해 제조업체들이 고급 열 포장 기술을 채택하도록 촉진하고 있습니다. 이러한 민감한 의약품은 효능 유지 및 품질 저하 방지를 위해 물류 체인 전반에 걸쳐 2°C-8°C 범위의 엄격한 온도 관리가 필요합니다. 전 세계 규제 기관들이 의약품 콜드체인 무결성에 관한 지침을 강화함에 따라, 제조업체들은 정밀하고 검증된 온도 성능을 제공하는 포장 솔루션을 도입해야 하는 압박이 커지고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

22억 달러

예측 금액

64억 달러

CAGR

11.1%

2024년 기준 호일 라미네이트 부문이 34.4%로 최대 점유율을 차지했습니다. 이 소재는 우수한 단열 성능과 최소 무게로 포장 산업의 핵심 재료로 자리매김하고 있습니다. 특히 국제 운송을 중심으로 온도 민감 분야에서의 용도가 확대되고 있습니다. 다층 호일 기술의 신규 개발로 열 보존성과 내구성이 향상되어 장기간 운송 및 변동 기후 조건에서도 더 나은 보호 기능을 제공합니다.

식품 및 음료 분야는 2034년까지 연평균 성장률(CAGR) 12.3%를 보일 것으로 예측됩니다. 대도시 지역의 생활 방식 변화, 신선한 식사에 대한 수요 증가, 전 세계 요리의 세계화로 인해 견고한 내열 포장재에 대한 요구가 더욱 강화되었다. 신속 배송 및 당일 배송 서비스의 확산으로 공급망 전반에 걸친 일관된 온도 관리가 해당 업계 기업들의 최우선 과제가 되었다.

미국의 전자상거래용 내열 포장 시장은 2024년 5억 870만 달러를 창출했습니다. 이 시장의 우위는 지속 가능한 물류 전략과 고급 콜드체인 시스템의 성공적 실행에서 비롯됩니다. 제조, 식품·음료, 제약 등 다양한 산업이 환경 목표 달성을 위해 재활용 가능한 단열 폼과 친환경 포장을 도입하고 있습니다. 에너지 효율적인 포장 옵션에 대한 미국의 강력한 집중은 이 부문에서의 선도적 위치를 지속적으로 공고히 하고 있습니다.

전자상거래용 내열 포장 시장의 주요 기업으로는 LD Packaging, DS Smith, Insulated Products Corporation, Novolex, Amcor, Aspect Solutions, Nordic Cold Chain Solutions, DBS Packaging 등이 있습니다. 해당 분야 기업들은 열효율과 환경 지속가능성을 결합한 소재 개발을 위해 연구개발에 적극 투자 중이다. 브랜드들은 친환경 솔루션에 대한 소비자 선호에 부응하기 위해 재활용 및 재사용이 가능한 단열 제품을 출시하고 있습니다. 또한 극한 기상 조건 하의 라스트마일 배송을 위한 맞춤형 포장 솔루션을 개발하기 위해 전자상거래 및 물류 업체들과 전략적 제휴를 맺는 기업들도 많습니다. 생산 능력과 전 세계 유통망 확장은 또 다른 주요 초점으로, 기업들이 지역별 수요에 보다 효과적으로 대응할 수 있게 합니다. 더불어 기업들은 온도 제어 규정을 충족하면서도 비용 효율성을 보장하는 맞춤형, 경량, 다층 포장 솔루션을 제공하는 디자인 혁신을 강조하고 있습니다.

목차

제1장 조사 방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 소스

세계

지역 및 국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

예측 모델

조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 촉진요인

성장 촉진요인

전자상거래 부문 성장

지속가능하고 생분해성 포장재료 수요 증가

라스트마일 배송에서의 콜드체인 준수 관련 엄격한 규제

열 보호를 필요로 하는 의약품 분야의 확대

온라인 식품 배달 서비스 및 밀키트 서비스의 성장

업계의 잠재적 위험 및 과제

고급 열 포장 재료의 높은 비용

제한된 재활용 가능성과 환경 문제

시장 기회

전자상거래 플랫폼과 포장 혁신 기업 간 협력

실시간 온도 모니터링을 위한 스마트 센서 통합

프리미엄 과자류 및 유기농 스킨케어와 같은 틈새 부문에서의 채택 증가

맞춤형, 브랜드 차별화된 보온 포장 개발

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

기술과 혁신의 상황

현재의 기술 동향

신흥기술

새로운 비즈니스 모델

규정 준수 요건

지속가능성 대책

지속 가능한 재료 평가

탄소발자국 분석

순환형 경제의 실현

지속가능성 인증 및 기준

지속가능성 ROI 분석

세계 소비자 감정 분석

특허 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 기업의 경쟁 벤치마킹

재무실적의 비교

수익

이익률

연구개발

제품 포트폴리오 비교

제품 라인업의 넓이

기술

혁신

지리적 존재의 비교

세계 실적 분석

서비스 네트워크의 범위

지역별 시장 침투율

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전(2021-2024년)

합병과 인수

파트너십 및 협업

기술적 진보

확대 및 투자 전략

지속가능성에 대한 노력

디지털 변혁의 대처

신흥기업 및 스타트업기업경쟁 구도

제5장 시장 추계 및 예측, 재료 유형별(2021-2034년)

주요 동향

호일 라미네이트

내열 플라스틱

단열지 기반 재료

단열 폼

기타

제6장 시장 추계 및 예측, 제품 유형별(2021-2034년)

주요 동향

내열 파우치 및 백

단열 상자 및 용기

보호 라이너 및 인서트

보온 봉투

기타

제7장 시장 추계 및 예측, 최종 용도별(2021-2034년)

주요 동향

미용 및 퍼스널케어

식품 및 음료

전자 및 전기

의료 및 의약품

기타

제8장 시장 추계 및 예측, 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

네덜란드

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제9장 기업 프로파일

Amcor plc

Aspect Solutions Ltd.

Cryopak

DBS Packaging

DS Smith

Insulated Products Corporation.

LD PACKAGING CO .,LTD

Nordic Cold Chain Solutions

Novolex

Perstorp

Puropak(Foshan) Co., Ltd.

Sealed Air

Sonoco ThermoSafe

Taghleef Industries

Thermal Packaging Solutions Ltd.

ZTJ Packaging Co., Ltd.

HBR

영문 목차

영문목차

The Global E-Commerce Heat-Resistant Packaging Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 11.1% to reach USD 6.4 billion by 2034. Market expansion is primarily driven by the ongoing growth of e-commerce and the increasing need for thermal protection in the pharmaceutical industry. With the surge in online purchases and international deliveries, the demand for packaging that can maintain product integrity under varied temperature conditions has significantly increased. Consumers are seeking reliability and sustainability, especially when it comes to the safe delivery of food, personal care items, and temperature-sensitive electronics. Packaging solutions must now not only provide thermal insulation but also be environmentally friendly, aligning with modern customer expectations. Rising healthcare delivery to homes and the growing digital presence of pharmaceutical suppliers have added momentum to the demand for insulated packaging.

Regulatory compliance and temperature control for critical products like biologics and insulin are also pushing manufacturers to adopt advanced thermal packaging technologies for secure delivery during transport. These sensitive pharmaceuticals require strict adherence to temperature ranges throughout the logistics chain, often between 2°C to 8°C, to preserve efficacy and avoid degradation. As global regulatory bodies tighten guidelines around pharmaceutical cold chain integrity, manufacturers are under increasing pressure to implement packaging solutions that offer precise, validated temperature performance.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$2.2 Billion

Forecast Value

$6.4 Billion

CAGR

11.1%

The foil laminates segment held the largest share in 2024, accounting for 34.4%. These materials are becoming a staple in the packaging industry due to their excellent insulation capabilities and minimal weight. Their application across temperature-sensitive sectors is growing, especially for international shipments. New developments in multi-layer foil technology are improving thermal retention and resistance, offering better protection during extended transit periods and under fluctuating climate conditions.

The food & beverage segment is projected to grow at a CAGR of 12.3% through 2034. Shifting lifestyles in metropolitan areas, rising demand for fresh meals, and the globalization of cuisine have all intensified the requirement for robust heat-resistant packaging. The rising adoption of fast and same-day delivery services has made consistent temperature control across the supply chain a top priority for businesses in this sector.

U.S. E-Commerce Heat-Resistant Packaging Market generated USD 508.7 million in 2024. Its dominance stems from the successful execution of sustainable logistics strategies and advanced cold chain systems. Various industries-including manufacturing, food and beverage, and pharmaceuticals-are embracing recyclable insulation foams and eco-conscious packaging to meet environmental goals. The country's strong focus on energy-efficient packaging options continues to shape its leadership position in this sector.

Leading companies in the E-Commerce Heat-Resistant Packaging Market include LD Packaging, DS Smith, Insulated Products Corporation, Novolex, Amcor, Aspect Solutions, Nordic Cold Chain Solutions, and DBS Packaging. Companies in this sector are actively investing in R&D to develop materials that combine thermal efficiency with environmental sustainability. Brands are introducing recyclable and reusable insulation products to align with consumer preferences for eco-friendly solutions. Many are also forming strategic partnerships with e-commerce and logistics providers to create tailored packaging solutions for last-mile delivery under extreme weather conditions. Expanding production capabilities and global distribution networks is another major focus, allowing firms to address regional demand more effectively. Additionally, businesses are emphasizing design innovation-offering customizable, lightweight, and multi-layer packaging that meets temperature control regulations while ensuring cost efficiency.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Material type trends

2.2.2 Product type trends

2.2.3 End use trends

2.2.4 Regional

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growth in e-commerce sector

3.2.1.2 Rising demand for sustainable and biodegradable packaging materials

3.2.1.3 Stringent regulations for cold chain compliance in last-mile delivery

3.2.1.4 Expansion of pharmaceutical sector requiring thermal protection

3.2.1.5 Growth of online food delivery and meal kit services

3.2.2 Industry pitfalls and challenges

3.2.2.1 High cost of advanced thermal packaging materials

3.2.2.2 Limited recyclability and environmental concerns

3.2.3 Market opportunities

3.2.3.1 Partnerships between E-commerce platforms and packaging innovators

3.2.3.2 Integration of smart sensors for real-time temperature monitoring

3.2.3.3 Increased adoption in niche segments like premium confectionery and organic skincare

3.2.3.4 Development of customizable, brand-differentiated insulated packaging

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and Innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Emerging business models

3.9 Compliance requirements

3.10 Sustainability Measures

3.10.1 Sustainable Materials Assessment

3.10.2 Carbon Footprint Analysis

3.10.3 Circular Economy Implementation

3.10.4 Sustainability Certifications and Standards

3.10.5 Sustainability ROI Analysis

3.11 Global consumer sentiment analysis

3.12 Patent analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 Latin America

4.2.1.5 Middle East & Africa

4.3 Competitive benchmarking of key players

4.3.1 Financial performance comparison

4.3.1.1 Revenue

4.3.1.2 Profit margin

4.3.1.3 R&D

4.3.2 Product portfolio comparison

4.3.2.1 Product range breadth

4.3.2.2 Technology

4.3.2.3 Innovation

4.3.3 Geographic presence comparison

4.3.3.1 Global footprint analysis

4.3.3.2 Service network coverage

4.3.3.3 Market penetration by region

4.3.4 Competitive positioning matrix

4.3.4.1 Leaders

4.3.4.2 Challengers

4.3.4.3 Followers

4.3.4.4 Niche players

4.3.5 Strategic outlook matrix

4.4 Key developments, 2021-2024

4.4.1 Mergers and acquisitions

4.4.2 Partnerships and collaborations

4.4.3 Technological advancements

4.4.4 Expansion and investment strategies

4.4.5 Sustainability initiatives

4.4.6 Digital transformation initiatives

4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Million & Kilo Tons)

5.1 Key trends

5.2 Foil laminates

5.3 High-temperature resistant plastics

5.4 Insulated paper-based materials

5.5 Thermal insulating foams

5.6 Others

Chapter 6 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Million & Kilo Tons)

6.1 Key trends

6.2 Heat-resistant pouches and bags

6.3 Insulated boxes and containers

6.4 Protective liners and inserts

6.5 Thermal mailers and envelopes

6.6 Others

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Million & Kilo Tons)

7.1 Key trends

7.2 Beauty & personal care

7.3 Food & beverages

7.4 Electronics & electrical

7.5 Healthcare & pharmaceuticals

7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million & Kilo Tons)