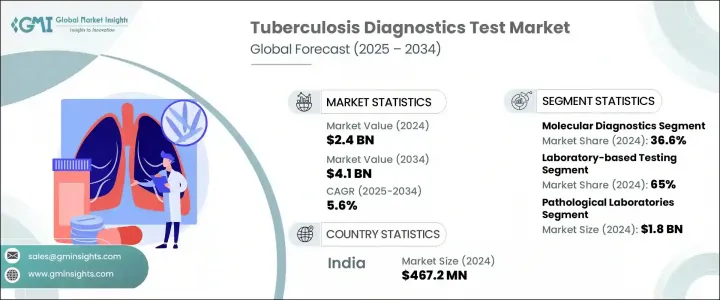

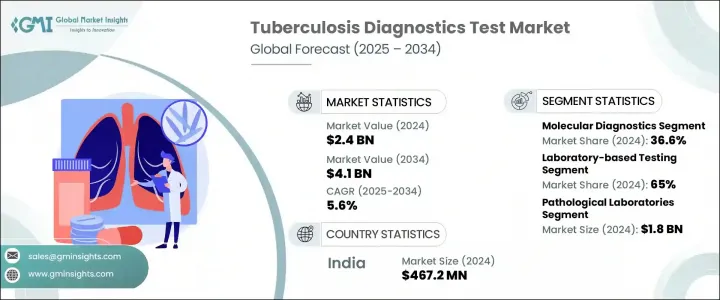

세계의 결핵 진단 검사 시장은 2024년에 24억 달러로 평가되었고, CAGR 5.6%로 성장할 전망이며, 2034년에는 41억 달러에 이를 것으로 추정되고 있습니다.

세계의 결핵 만연률 증가는 진단 기술의 진보와 공중 보건 의식의 급상승과 함께 신뢰성 높은 검사 도구에 대한 수요를 부추기고 있습니다. 포인트 오브 케어 검사의 도입이 진행되어, 계획적인 스크리닝 프로그램의 실시가 조기 발견율의 향상에 도움이 되고 있습니다. 관민 양 부문이 지원하는 이러한 대처는, 결핵의 만연을 억제하는데 있어서 지극히 중요한 스텝인 시의적절한 진단과 치료를 합리화하는 것을 목적으로 하고 있습니다.

시장 확대의 주된 요인은 조기 스크리닝의 대처를 강화하는 세계의 대처입니다. 정부가 지원하는 헬스케어 프로그램에서는 고위험 집단을 지원하기 위한 체계적인 전략을 펼쳐 진단 접근성을 향상시키고 있습니다. 이러한 대처에 의해, 지역 밀착형 검사 및 아웃리치에 의한 조기 발견이 가속하고 있습니다. 결핵 진단 검사는 결핵균의 존재를 검출하고 개인이 활동성 결핵인지 잠재성 결핵 감염인지를 판정하기 위해 사용됩니다. 정확한 동정이 보다 중시되는 가운데 이 시장에서는 계속해서 진단 플랫폼 전체의 기술 혁신과 인프라에 대한 투자가 확대되고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 24억 달러 |

| 예측 금액 | 41억 달러 |

| CAGR | 5.6% |

2024년에는 분자진단제가 주요 부문으로 부상하여 점유율 36.6%를 차지하였고, 2034년까지 CAGR 5.9%로 성장이 예측됩니다. 이들 진단제는 결핵균과 그 약제 내성 형질을 신속하고, 고감도, 고정밀도로 검출함으로써, 지금까지의 상식을 뒤집었습니다. 이 분야의 핵심 기술인 중합효소 연쇄반응(PCR)을 사용하여 건강관리자는 임상 검체로부터 결핵균을 정확하게 검출할 수 있어 조기 치료 결정을 보다 효과적으로 실시할 수 있게 되었습니다.

실험실 기반 검사 카테고리는 2024년 65%의 최대 점유율을 차지했습니다. 그 이점은 주로 복잡한 약물 내성 결핵 사례의 진단에 필수적인 정확하고 집중적인 검사 방법의 사용으로 인한 것입니다. 이러한 검사는 일반적으로 병원, 공중 보건 기관 및 민간 인증 검사 기관에서 실시됩니다. 일반적인 검사 기술로는 도말 현미경 검사, 배양 기반 진단, 인터페론-감마 방출 분석(IGRA) 등이 있으며, 모두 질병의 중증도와 잠재적인 내성에 대한 상세한 인사이트를 제공하고 임상의가 맞춤형 치료 계획을 세울 때의 지침이 됩니다.

아시아태평양의 결핵 진단 검사 시장은 2025-2034년 연평균 복합 성장률(CAGR) 5.6%를 보일 것으로 예측됩니다. 이 성장의 요인으로는 결핵 환자 수 증가, 공중 보건 교육의 확대, 진단 실험실 접근의 확대, 진단 인프라의 강화를 목적으로 한 정부 지원 정책 등이 있습니다. 이 지역에서는 헬스케어에 대한 투자가 계속되고 있기 때문에 첨단 결핵 검사 솔루션에 대한 수요가 높아질 것으로 예측됩니다.

이 분야를 선도하는 주요 기업은 Danaher Corporation, Abbott Laboratories, bioMerieux, Qiagen NV, Becton, Dickinson and Company, and F. Hoffmann-La Roche 등이 있습니다. 시장에서의 존재감을 높이기 위해, 톱 기업은 분자 진단 및 신속 진단 기술을 진보시키는 연구 개발에 다액의 투자를 실시했습니다. 헬스케어 프로바이더나 연구 기관과의 전략적 합병이나 공동 연구는, 각사의 진단 포트폴리오나 세계적인 사업 전개의 확대에 도움이 되고 있습니다. 몇몇 기업은 특히 고부하 지역의 저자원 환경을 위해 저비용으로 휴대 가능한 결핵 검사 솔루션 개발에 주력하고 있습니다. 게다가 제조사는 검사 감도를 최적화하고 납기를 단축해 자사의 플랫폼이 국제적인 규제 기준을 충족하고 있는 것을 보증하고 있습니다. 이러한 전략에 의해, 접근성, 정확성, 효율성이 강화되어 각 회사는 장기적인 시장 리더로서의 지위를 확립하고 있습니다.

The Global Tuberculosis Diagnostics Test Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 4.1 billion by 2034. Increasing TB prevalence worldwide, coupled with advancements in diagnostic technologies and a sharp rise in public health awareness, are fueling demand for reliable testing tools. The rising adoption of point-of-care testing and the implementation of structured screening programs are helping improve early detection rates. These efforts, supported by both public and private sectors, aim to streamline timely diagnosis and treatment, crucial steps in controlling the spread of tuberculosis.

A major driver behind the market's expansion is the global effort to strengthen early screening initiatives. Government-backed healthcare programs are rolling out structured strategies to support high-risk populations with better diagnostic access. These initiatives are accelerating early identification through community-based testing and outreach. Tuberculosis diagnostic tests are used to detect the presence of the mycobacterium tuberculosis bacteria and to determine if an individual has active TB or a latent TB infection, which is essential for guiding treatment decisions. With more emphasis on accurate identification, the market continues to witness greater investment in innovation and infrastructure across diagnostic platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $4.1 Billion |

| CAGR | 5.6% |

In 2024, molecular diagnostics emerged as the leading segment, contributing 36.6% share and projected to grow at a CAGR of 5.9% through 2034. These diagnostics have changed the game by offering fast, sensitive, and accurate detection of Mycobacterium tuberculosis and its drug resistance traits. The use of polymerase chain reaction (PCR) as a central technique in this space enables healthcare providers to detect TB bacteria from clinical samples with precision, making early treatment decisions more effective.

The laboratory-based testing category held the largest share 65% in 2024. Its dominance is primarily attributed to the use of accurate, centralized testing methods critical for diagnosing complex and drug-resistant TB cases. These tests are typically performed in hospitals, public health institutions, and private certified laboratories. Common testing techniques include smear microscopy, culture-based diagnostics, and interferon-gamma release assays (IGRAs), all of which offer in-depth insight into disease severity and potential resistance, guiding clinicians in creating tailored treatment plans.

Asia Pacific Tuberculosis Diagnostics Test Market is expected to grow at a CAGR of 5.6% from 2025 to 2034. Factors contributing to this growth include the increasing number of TB cases, expanding public health education, greater access to diagnostic labs, and supportive governmental policies aimed at strengthening diagnostic infrastructure. As the region continues to invest in healthcare, the demand for advanced TB testing solutions is forecasted to rise.

Prominent players leading this space include Danaher Corporation, Abbott Laboratories, bioMerieux, Qiagen N.V., Becton, Dickinson and Company, and F. Hoffmann-La Roche. To strengthen their market presence, top firms are heavily investing in R&D to advance molecular and rapid diagnostic technologies. Strategic mergers and collaborations with healthcare providers and research institutions are helping companies expand their diagnostic portfolios and global footprint. Several players are focusing on creating low-cost, portable TB testing solutions tailored for low-resource settings, particularly in high-burden regions. Additionally, manufacturers are optimizing test sensitivity, reducing turnaround time, and ensuring their platforms meet international regulatory standards. These strategies collectively enhance accessibility, accuracy, and efficiency, positioning companies for long-term market leadership.