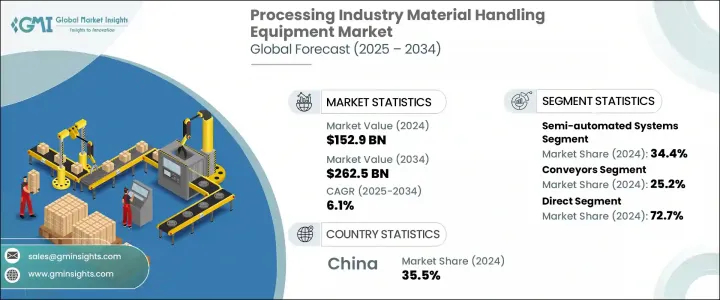

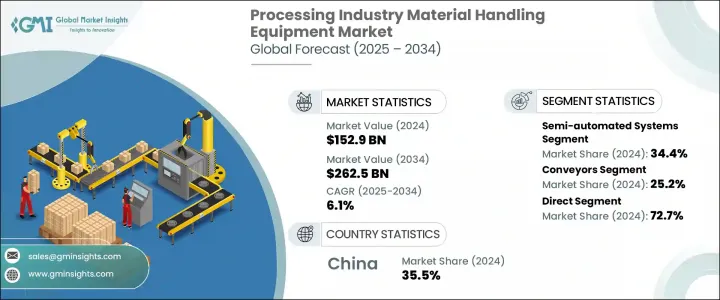

세계의 가공 산업용 자재관리 장비 시장은 2024년에는 1,529억 달러로 평가되었고, CAGR 6.1%로 성장할 전망이며, 2034년에는 2,625억 달러에 이를 것으로 추정되고 있습니다.

이 꾸준한 상승은 주로 가공 부문 전체에서 고도로 자동화된 솔루션에 대한 수요가 높아지고 있는 것에 기인하고 있습니다. 이 업계는 재료의 이동, 보관, 관리 방법을 재구축하는 지능형 기술의 통합으로 디지털 전환을 점점 더 받아들이고 있습니다. 자동화는 더 이상 미래의 동향이 아니라, 업무 효율, 비용 삭감, 노동자의 안전에 있어서 불가결한 요소가 되고 있습니다.

가공 업계 전체의 기업이 로봇 공학, AI, IoT 등의 혁신을 활용하여 워크플로우를 합리화하고, 실시간 가시성을 높이고, 보다 우수한 프로세스 제어에 의해 경쟁력을 획득하고 있습니다. 이러한 디지털 시스템은 생산량을 향상시킬 뿐만 아니라 수작업에 대한 의존을 줄이고 조작 실수를 최소화하며 가동 시간을 늘림으로써 낭비 없는 제조를 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1,529억 달러 |

| 예측 금액 | 2,625억 달러 |

| CAGR | 6.1% |

급속하게 진화하는 시장에서 기업이 생산성을 높이고 민첩성을 유지해야 한다는 압박의 고조에 직면하는 가운데, 최신의 자재관리 장비로의 시프트는 계속 가속화되고 있습니다. 스마트 핸들링 솔루션 채택으로 기업은 역동적인 생산 요구에 신속하게 대응할 수 있게 되었으며, 동시에 에너지 효율적인 운영과 머티리얼 핸들링 폐기물 최소화를 통해 지속 가능성 목표도 지원할 수 있게 되었습니다. 게다가 이러한 자동화 시스템은 다양한 산업 요건에 맞게 커스터마이징 할 수 있기 때문에 정밀도, 일관성, 적응성이 중요한 가공 용도에 최적입니다.

식품 가공에서 화학, 전자에 이르기까지 기업은 흐름을 강화하고 병목 현상을 줄이고 시설 내에서 원활한 이동을 보장하는 장비에 투자하고 있습니다. 이러한 근대화의 추진은 대규모 제조 오퍼레이션을 변혁할 뿐만 아니라, 완전 자율형 시스템에 고액의 투자를 하지 않고 경쟁력을 유지하는 것을 목표로 하는 중규모 시설에 있어서도 유익하다는 것이 증명되고 있습니다. 이러한 시프트의 누적 효과는, 가공 환경에 특화한 자재관리 장비에 대한 강력한 수요 궤도가 되고 있습니다.

운영 모드의 관점에서 시장은 수동 시스템, 반자동 시스템, 완전 자동 시스템, IoT 지원 스마트 핸들링 시스템으로 분류됩니다. 이 중 반자동화 부문은 2024년 시장 리더로 부상하여 전체 수익의 약 34.4%를 차지했습니다. 이 부문은 예측 기간을 통해 CAGR 4.4% 이상으로 성장할 것으로 예측됩니다. 반자동 장치는 자동화의 장점과 운영자 제어의 최적 융합을 제공하며 유연성과 정확성을 모두 요구하는 비즈니스에 특히 매력적입니다. 이러한 시스템은 워크플로우가 다양한 시설에 특히 적합하며, 작업자는 반복 작업을 기계화하면서 사용자 정의된 작업을 효율적으로 관리할 수 있습니다. 합리적인 가격, 통합 편의성 및 유지 보수 요구 사항이 낮기 때문에 자율 주행으로 완전히 전환하지 않고 규모를 확장하려는 많은 가공업체에게 실용적인 선택이 되었습니다.

용도별로 보면 시장은 컨베이어, 크레인 호이스트, 지게차 산업용 트럭, 무인 반송차(AGV), 보관 및 검색 시스템, 로봇 자재관리 시스템, 벌크 자재관리 장비 등으로 구분됩니다. 컨베이어 분야는 2024년에 25.2%의 수익 점유율로 시장을 선도하였고, 2025-2034년 5.5% 이상의 CAGR을 나타낼 것으로 예측됩니다. 컨베이어 시스템이 널리 보급되고 있는 이유는 가공 공장 내의 다양한 지점에서 재료를 원활하게 운반하는 능력이 있기 때문입니다. 디자인의 다양성은 경량에서 대량의 수하물에 이르기까지 다양한 물품의 이동을 지원하여 처리 능력을 향상시키고 처리 시간을 최소화합니다. 이러한 시스템은 연속적인 생산 사이클에서 실행되는 산업에 필수적인 중단 없는 재료 흐름을 확보함으로써 공정 최적화에 크게 기여합니다.

시장은 유통 채널을 기반으로 직접 채널과 간접 채널로 나뉩니다. 2024년에는 직접 판매 부문이 72.7%의 수익 점유율로 지배적인 지위를 차지했으며 예측 기간을 통해 CAGR 4.7% 이상으로 성장할 것으로 예측됩니다. 직접 판매 채널은 구매자에게 적합한 솔루션과 기술 지원을 제공하여 강력한 가치 프로포지션을 창출합니다. 그러나 간접 부문은 계속 시장 확대에 중요한 역할을 하고 있습니다. 간접 부서는 고객에게 더 넓은 도달 범위를 제공하고, 맞춤화, 판매 후 지원, 유연한 자금 조달 옵션 등 특히 중소기업에 매력적인 추가 서비스를 제공합니다. 이러한 듀얼 채널 접근 방식은 제조업체가 개별 지원 서비스와 광범위한 접근성의 균형을 유지하는 데 도움이 됩니다.

지역별로는 중국이 2024년 아시아태평양 가공 산업용 자재관리 장비 시장에서 톱 러너로 부상하였으며 지역 점유율의 약 35.5%를 확보했습니다. 이 나라 시장은 2034년까지 20억 달러 이상에 달할 것으로 예측됩니다. 이러한 이점은 급속한 산업 개발, 견고한 제조 인프라, 자동화 및 스마트 제조 촉진을 목적으로 한 정부의 강력한 이니셔티브에 의해 뒷받침되고 있습니다. 지속적인 도시화와 지역 산업화에 대한 노력은 진보된 취급 시스템에 대한 수요를 더욱 촉진하고 중국을 아시아태평양 전체의 이 부문 성장에 중요한 공헌자로 삼고 있습니다.

가공 산업용 자재관리 장비 시장의 세계 정세를 형성하고 있는 유명한 기업으로는 Daifuku, Crown Equipment Corporation, Dematic Group, GEA, Fives Group, Hyster-Yale Materials Handling, JBT Corporation, Intelligrated, Junheinrich, Linde Material Handling, KION Group, Mitsubishi Log Industries Corporation 등이 있습니다. 이들 기업은 경쟁력을 강화하고 지능적으로 통합된 자재관리 솔루션에 대한 요구의 고조에 대응하기 위해 연구 개발, 파트너십, 세계 전개에 많은 투자를 하고 있습니다.

The Global Processing Industry Material Handling Equipment Market was valued at USD 152.9 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 262.5 billion by 2034. This steady rise is primarily attributed to the growing demand for advanced, automated solutions across processing sectors. The industry is increasingly embracing digital transformation, driven by the integration of intelligent technologies that are reshaping how materials are moved, stored, and managed. Automation is no longer a future trend-it has become an essential element of operational efficiency, cost reduction, and workforce safety.

Companies across processing industries are leveraging innovations such as robotics, AI, and IoT to streamline workflows, enhance real-time visibility, and gain a competitive edge through better process control. These digital systems not only improve production output but also support lean manufacturing by reducing reliance on manual labor, minimizing operational errors, and increasing uptime.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $152.9 Billion |

| Forecast Value | $262.5 Billion |

| CAGR | 6.1% |

As businesses face heightened pressure to boost productivity and maintain agility in rapidly evolving markets, the shift toward modern material handling equipment continues to accelerate. The adoption of smart handling solutions has enabled companies to respond faster to dynamic production needs, while also supporting sustainability goals through energy-efficient operations and minimizing material waste. Furthermore, these automated systems can be tailored for various industrial requirements, making them ideal for processing applications where precision, consistency, and adaptability are critical.

From food and beverage processing to chemicals and electronics, enterprises are investing in equipment that enhances flow, reduces bottlenecks, and ensures seamless intra-facility movement. This push toward modernization is not only transforming large manufacturing operations but is also proving beneficial for mid-sized facilities aiming to stay competitive without investing heavily in fully autonomous systems. The cumulative effect of these shifts is a robust demand trajectory for material handling equipment tailored specifically to processing environments.

In terms of operation mode, the market is categorized into manual systems, semi-automated systems, fully automated systems, and IoT-enabled smart handling systems. Among these, the semi-automated segment emerged as the market leader in 2024, capturing around 34.4% of the overall revenue. This segment is forecasted to grow at a CAGR of over 4.4% through the forecast period. Semi-automated equipment offers an optimal blend of automation benefits and operator control, which is particularly appealing to businesses that require both flexibility and precision. These systems are especially suitable for facilities with varying workflows, enabling operators to manage customized tasks efficiently while mechanizing repetitive activities. Their affordability, ease of integration, and lower maintenance requirements make them a practical choice for many processing firms aiming to scale without transitioning fully to autonomous operations.

On the basis of application, the market is segmented into conveyors, cranes and hoists, forklifts and industrial trucks, automated guided vehicles (AGVs), storage and retrieval systems, robotic material handling systems, bulk material handling equipment, and others. The conveyors segment led the market in 2024 with a revenue share of 25.2%, and it is anticipated to register a CAGR of over 5.5% from 2025 to 2034. The widespread deployment of conveyor systems is due to their ability to transport materials seamlessly across different points within processing plants. Their design versatility supports the movement of a wide range of goods, from lightweight items to bulk loads, thereby improving throughput and minimizing handling times. These systems contribute significantly to process optimization by ensuring uninterrupted material flow, which is essential for industries that operate on continuous production cycles.

The market, based on distribution channel, is divided into direct and indirect channels. In 2024, the direct sales segment held the dominant position with a revenue share of 72.7% and is projected to grow at a CAGR of over 4.7% throughout the forecast period. Direct channels offer buyers better access to tailored solutions and technical support, creating strong value propositions. However, the indirect segment continues to play a critical role in market expansion. It enables broader customer reach and provides additional services such as customization, post-sale assistance, and flexible financing options, which are especially appealing to small and mid-sized enterprises. This dual-channel approach helps manufacturers maintain a balance between personalized service and wide-scale accessibility.

Regionally, China emerged as the front-runner in the Asia-Pacific processing industry material handling equipment market in 2024, securing approximately 35.5% of the regional share. The country's market is projected to exceed USD 2 billion by 2034. This dominance is fueled by rapid industrial development, a robust manufacturing infrastructure, and strong governmental initiatives aimed at boosting automation and smart manufacturing. Continued urbanization and regional industrialization efforts further drive the demand for advanced handling systems, making China a key contributor to the sector's growth across APAC.

Prominent players shaping the global landscape of the processing industry material handling equipment market include Daifuku, Crown Equipment Corporation, Dematic Group, GEA, Fives Group, Hyster-Yale Materials Handling, JBT Corporation, Intelligrated, Jungheinrich, Linde Material Handling, KION Group, Mitsubishi Logisnext, Tetra Pak, SSI Schaefer Group, and Toyota Industries Corporation. These companies are investing heavily in R&D, partnerships, and global expansions to strengthen their competitive positions and cater to the increasing need for intelligent and integrated material handling solutions.