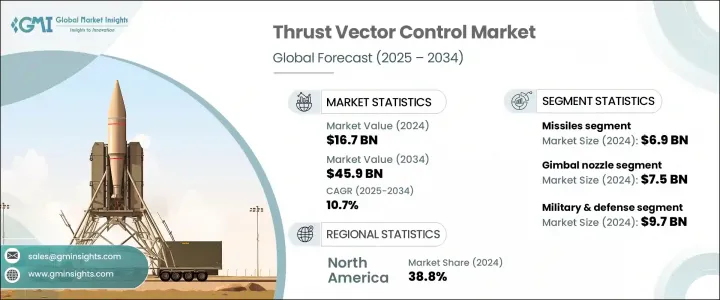

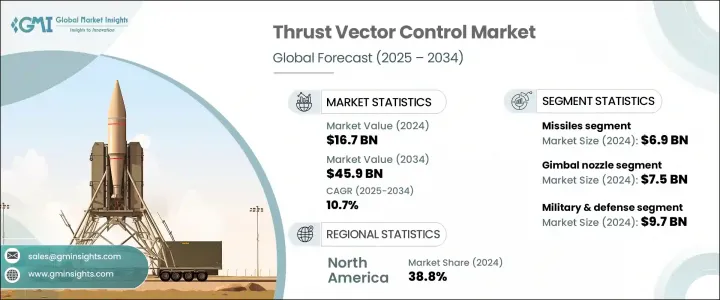

세계의 추력 벡터 제어 시장 규모는 2024년에 167억 달러로 평가되었고, CAGR 10.7%로 성장할 전망이며, 2034년에는 459억 달러에 이를 것으로 예측됩니다.

항공 우주 및 방위 산업 전체에서 선진 추진 시스템의 채용이 증가하고 있는 것이 이 시장의 성장을 가속하는 주요 요인입니다. 세계 정부 및 방위 기관은 미사일의 정확성, 발사 유연성, 비행 중 기동성을 높이는 기술에 대한 투자를 늘리고 있습니다. 각국이 현대적인 전쟁 능력과 우주 탐사 프로그램을 우선시하는 가운데 효율적이고 응답성이 높은 비행 제어 시스템에 대한 수요가 높아지고 있습니다. 엔진의 추력을 실시간으로 전환할 수 있는 TVC 시스템은 대기권 내 및 대기권 외부 미션 모두에서 필수적입니다.

이 성장을 지원하는 큰 힘의 하나는 정밀 유도탄 및 고속 비행 능력을 계속 중시하는 것입니다. 현대 전쟁에서는 적의 방어망을 피하고 정확하게 공격할 수 있는 빠르고 응답성이 높은 미사일 시스템에 대한 의존도가 높아지고 있습니다. 추력 벡터 제어 기술은 비행 중 방향 전환, 궤도 조정 및 공기 역학 성능 향상을 가능하게 함으로써 이러한 능력을 가능하게 합니다. 또한 인공위성 배치 및 궤도 미션에 대한 민간 부문의 진입이 증가하고 있기 때문에 스테이지 분리 및 궤도 투입 정밀도를 TVC에 크게 의존하는 발사 시스템에 대한 수요가 높아지고 있습니다. 항공우주 추진 기술 혁신은 또한 공기 저항을 줄이고 연료 효율을 높이고 엄격한 조건 하에서 더 나은 항행 제어를 제공하는보다 정교한 벡터링 기술을 채택하는 것을 제조업체에게 촉구합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 167억 달러 |

| 예측 금액 | 459억 달러 |

| CAGR | 10.7% |

2024년에는 미사일이 69억 달러를 차지하고 시장 최대의 용도 부문이 되었습니다. 목표와의 정확한 교전, 대기권 재돌입시의 제어 개선, 차세대 요격 시스템의 배치에 대한 요구의 고조가 미사일 플랫폼에서의 TVC 기구의 사용을 가속시키고 있습니다. 이 시스템은 공대공, 지대공, 지상 발사의 발사체에서 신속한 방향 전환 및 적응적인 움직임을 가능하게 합니다. 또한 전투 시나리오에서 미사일의 생존성 및 응답성을 높여 전략적 및 전술적 방위 작전에 필수적인 역할을 하고 있습니다.

발사체는 예측 기간 중 가장 빠른 CAGR 12.4%로 확대될 것으로 예상되고 있습니다. 상업 위성이나 정부가 지원하는 위성 미션의 증가에 의해, 추력 관리에 높은 정밀도가 요구되는 발사 시스템의 배치가 진행되고 있습니다. 추력 벡터링은 멀티 페이로드 핸들링, 정확한 궤도 정렬, 미션 고유의 궤도 구성 달성을 보장하는 데 필수적입니다. 특히 소형 위성의 배치 및 재사용 가능한 로켓의 대두로 벡터 제어 솔루션은 페이로드 역학과 미션 민첩성에서 새로운 요건을 충족시키기 위해 진화하고 있습니다.

기술별로는 짐벌 노즐 부문이 2024년 세계 시장을 독점하여 75억 달러의 수익을 올렸습니다. 짐벌 노즐은 엔진의 추력을 방향 전환하기 위해 선회하는 것으로 작동하며, 비행체의 방향 및 자세를 미세 조정하는 데 중요한 역할을 합니다. 기계적으로 간단하고 정밀한 제어가 가능하기 때문에 수직 발사 및 고속 미사일 조종에 매우 적합합니다. 유연하고 정확한 비행 시스템에 대한 요구가 높아짐에 따라 이러한 노즐은 새롭게 개발된 항공 우주 및 방위 프로그램에서 더 큰 지지를 받고 있습니다. 동적 안정성, 궤도 수정, 고도 제어에서 중요한 이점을 제공합니다.

최종 용도는 주로 우주기관과 군 및 방위기관으로 나뉘어져 있습니다. 군사 및 방위 부문은 2024년에 97억 달러로 평가되어 주요 부문으로 부상했습니다. 전 세계 군대가 전략적 현대화 프로그램을 강화하고 있으며, 그 중에는 응답 시간 단축, 목표 적응성 향상, 임무 성과 개선을 위한 선진적 TVC 시스템 통합이 포함되어 있습니다. 고속 요격 미사일부터 차세대 전투 플랫폼까지 정확한 타격 능력과 작전 유연성을 가능하게 하는 TVC의 역할은 계속 확대되고 있습니다. 특히, 진화하는 위협은, 방위 제조업체에 고도의 추력 백토링 솔루션에 크게 의존하는 적응 추진 시스템을 짜넣도록 재촉하고 있습니다.

지역별로는 북미가 압도적인 시장 점유율을 유지해 2024년 세계 매출의 38.8%를 차지했습니다. 이것은, 강고한 항공 우주 제조 인프라, 착실한 연구 개발 자금, 대기업 방위 관련 기업의 존재에 의지하고 있습니다. 이 지역은 대규모 조달 프로그램이나 뛰어난 조종성 및 추력 제어를 필요로 하는 차세대 항공기 플랫폼의 채택을 통해 CAGR 10.8%로 확대될 것으로 예측되고 있습니다. 미국은 단독으로 최대 시장을 유지하며 2024년에는 57억 달러에 이르렀습니다. 이 나라가 선진적인 항공 및 우주 전투 시스템의 구축에 주력하고 있는 것이, TVC 시장의 성장에 크게 기여하고 있습니다.

추력 벡터 제어 분야의 주요 업계 기업은 BAE Systems, BPS Space, Collins Aerospace, Honeywell International, JASC Corporation, Moog, Parker Hannifin 등이 있습니다. 이러한 기업은 제어 정밀도, 신뢰성, 여러 플랫폼에 대한 통합 유연성을 향상시키는 차세대 TVC 시스템에 일관되게 투자하고 있습니다. 항공우주와 방위의 전망이 계속 진화하는 가운데 정세 기술의 역할은 미션의 성공과 작전의 우위성에서 계속 중심적인 역할을 할 것으로 기대됩니다.

The Global Thrust Vector Control Market was valued at USD 16.7 billion in 2024 and is estimated to grow at a CAGR of 10.7% to reach USD 45.9 billion by 2034. The increasing adoption of advanced propulsion systems across the aerospace and defense industries is a primary factor driving the growth of this market. Governments and defense agencies worldwide are increasing their investments in technologies that enhance missile precision, launch flexibility, and in-flight maneuverability. As countries continue to prioritize modern warfare capabilities and space exploration programs, the demand for efficient and responsive flight control systems has intensified. TVC systems, which allow for real-time redirection of engine thrust, are becoming essential in both atmospheric and exo-atmospheric missions.

One of the significant forces behind this growth is the continued emphasis on precision-guided munitions and high-speed flight capabilities. Modern warfare increasingly relies on fast, responsive missile systems that can evade enemy defenses and strike with accuracy. Thrust vector control technologies make these abilities possible by allowing mid-flight directional changes, trajectory adjustments, and improved aerodynamic performance. Additionally, growing private sector participation in satellite deployment and orbital missions has fueled demand for launch systems that rely heavily on TVC for stage separation and orbital insertion accuracy. Innovations in aerospace propulsion are also pushing manufacturers to adopt more sophisticated vectoring technologies that reduce drag, enhance fuel efficiency, and provide greater navigational control in challenging conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $16.7 Billion |

| Forecast Value | $45.9 Billion |

| CAGR | 10.7% |

In 2024, missiles represented the largest application segment in the market, accounting for USD 6.9 billion. The increasing need for accurate target engagement, improved control during atmospheric reentry, and the deployment of next-gen interceptor systems is accelerating the use of TVC mechanisms in missile platforms. These systems enable fast redirection and adaptive movement in air-to-air, surface-to-air, and ground-launched projectiles. They also enhance missile survivability and responsiveness in combat scenarios, making them indispensable in strategic and tactical defense operations.

Launch vehicles are anticipated to expand at the fastest CAGR of 12.4% over the forecast period. The growing number of commercial and government-backed satellite missions has resulted in the deployment of launch systems that demand high precision in thrust management. Thrust vectoring is essential in ensuring multi-payload handling, accurate trajectory alignment, and achieving mission-specific orbital configurations. Especially with the rise of small satellite deployments and reusable rockets, vector control solutions are evolving to meet new requirements in payload dynamics and mission agility.

By technology, the gimbal nozzle segment dominated the global market in 2024, generating USD 7.5 billion in revenue. Gimbal nozzles, which operate by pivoting to redirect engine thrust, play a critical role in fine-tuning the direction and attitude of flight vehicles. Their mechanical simplicity and ability to offer precise control make them ideal for both vertical launches and high-speed missile maneuvers. As demand increases for flexible and accurate flight systems, these nozzles are gaining more traction in newly developed aerospace and defense programs. They provide key advantages in dynamic stability, trajectory correction, and altitude control.

The end-use landscape is primarily split between space agencies and military & defense institutions. The military & defense sector emerged as the leading segment, valued at USD 9.7 billion in 2024. Armed forces worldwide are ramping up strategic modernization programs that include the integration of advanced TVC systems for faster response times, greater target adaptability, and improved mission outcomes. From high-speed interceptors to next-generation combat platforms, the role of TVC in enabling precise strike capabilities and operational flexibility continues to grow. In particular, evolving threats are pushing defense manufacturers to incorporate adaptive propulsion systems that rely heavily on advanced thrust vectoring solutions.

Regionally, North America maintained the dominant market share, accounting for 38.8% of global revenue in 2024, supported by robust aerospace manufacturing infrastructure, steady research and development funding, and the presence of major defense contractors. The region is projected to expand at a CAGR of 10.8%, driven by large-scale procurement programs and the adoption of next-generation aircraft platforms that require superior maneuverability and thrust control. The United States remained the single largest market, reaching USD 5.7 billion in 2024. The country's focus on building advanced air and space combat systems is a major contributor to TVC market growth.

Key industry players in the thrust vector control space include BAE Systems, BPS Space, Collins Aerospace, Honeywell International, JASC Corporation, Moog, and Parker Hannifin. These companies are consistently investing in next-gen TVC systems that offer improved control precision, reliability, and integration flexibility across multiple platforms. As the aerospace and defense landscape continues to evolve, the role of thrust vector control technologies is expected to remain central to mission success and operational superiority.