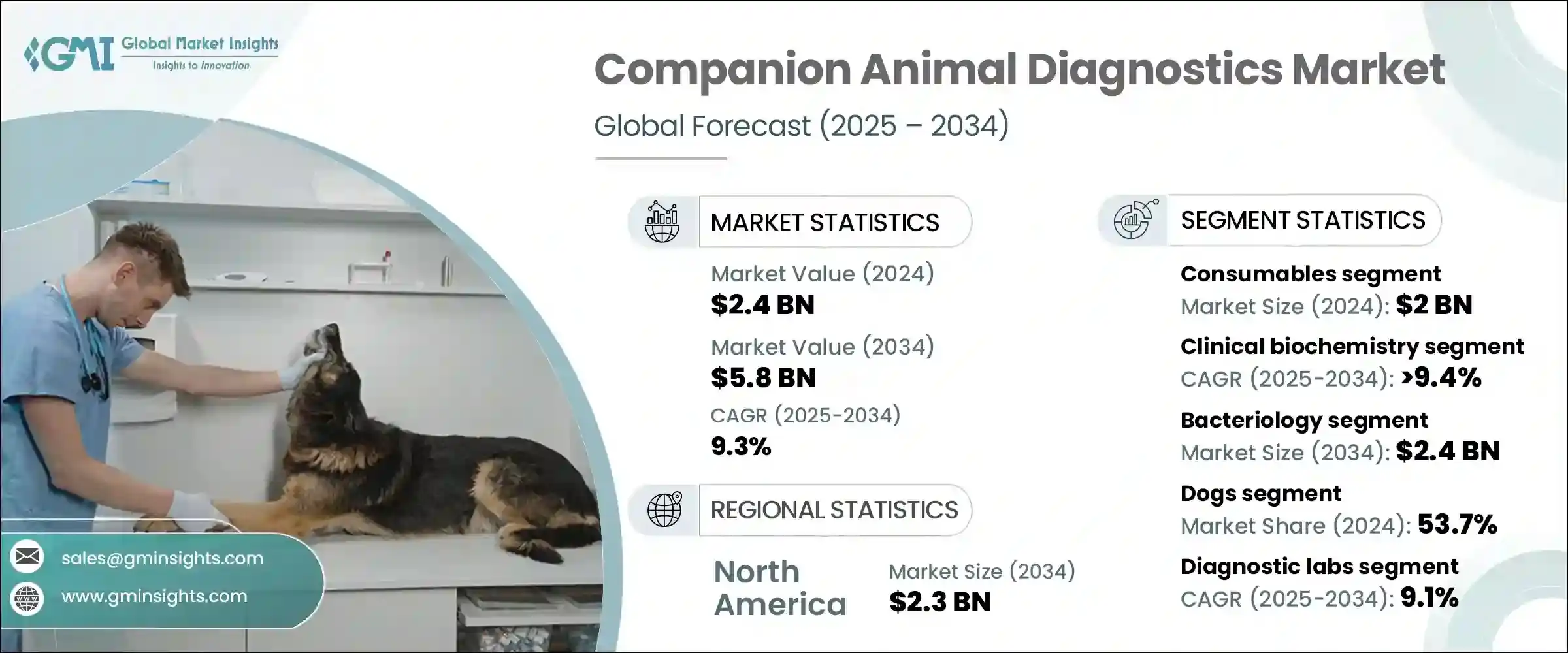

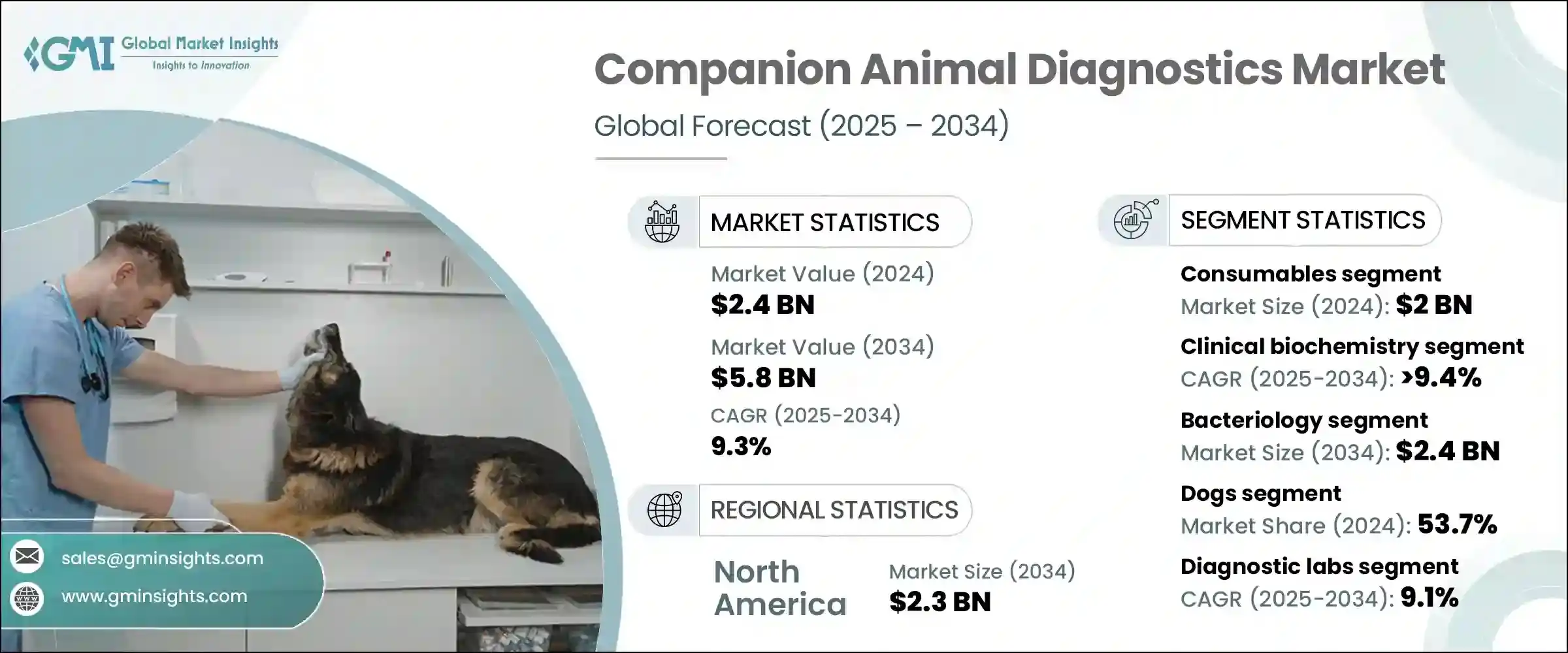

세계의 반려동물 진단약 시장은 2024년에는 24억 달러로 평가되며, CAGR 9.3%로 성장하며, 2034년에는 58억 달러에 달할 것으로 추정되고 있습니다.

이러한 성장의 원동력은 전 세계 반려동물 인구 증가, 반려동물 동반에 대한 선호도 증가, 동물의 만성 및 감염성 질환 진단이 급증하고 있기 때문입니다. 반려동물을 돌보는 것이 가정의 필수적인 부분으로 자리 잡으면서 수의학 서비스에 대한 지출은 지속적으로 증가하고 있습니다. 반려동물 보호자들은 동물을 가족의 일원으로 여기게 되었고, 그 결과 정기적인 건강 검진, 예방 의료, 적시 진단이 이루어지고 있습니다. 이러한 문화적 변화로 인해 동물의 건강에 대한 관심이 높아지면서 고급 진단 툴와 서비스에 대한 수요가 크게 증가하고 있습니다.

시장 확대는 인수공통전염병에 대한 인식이 높아지고 합병증을 예방하기 위한 조기 진단의 중요성이 높아지면서 시장 성장에 힘을 실어주고 있습니다. 수의학 전문가들은 장기 기능 장애, 대사 문제, 감염 등의 상태를 평가하기 위해 진단에 의존하고 있으며, 이는 이 분야의 성장을 더욱 촉진하고 있습니다. 또한 기술의 발전은 신속하고 정확하며 덜 침습적인 진단 기술을 가능하게 함으로써 이 분야를 재구성하고 있습니다. 수의 진단의 혁신은 더 빠른 시간 내에 치료 전략과 더 나은 통합을 가능하게 하여 진단을 동물 헬스케어의 핵심 요소로 만들고 있습니다. 전 세계에서 수의학 인프라가 강화됨에 따라 진단 제품 및 서비스에 대한 수요는 계속 증가할 것으로 예측됩니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작 금액 | 24억 달러 |

| 예측 금액 | 58억 달러 |

| CAGR | 9.3% |

제품 세분화에서 시장은 장비와 소모품으로 나뉘며, 2024년에는 소모품 부문이 20억 달러로 우위를 차지합니다. 이러한 우위는 시약, 검사 키트, 슬라이드, 튜브와 같은 소모품이 각 진단 과정에서 필수적인 역할을 하기 때문입니다. 장비와 달리 소모품은 검사할 때마다 소모품이 필요하므로 정기적인 구매가 필요하고 안정적인 시장 매출을 얻을 수 있습니다. 동물병원의 검사 빈도가 증가함에 따라 소모품 수요도 함께 증가할 것으로 예측됩니다. 정기 검진 및 예방 검진 추세는 사용량을 더욱 증가시킬 것입니다. 또한 더 많은 진단 절차가 신속하고 현장 진료 형태로 전환됨에 따라 일회용 용도에 맞게 조정된 소모품이 표준이 되고 있으며, 이는 부문 성장을 가속하고 있습니다.

애플리케이션별로 분석하면 세균학 부문은 2024년에 주요 카테고리로 부상하고 2034년에는 24억 달러에 달할 것으로 예측됩니다. 이 부문은 반려동물의 세균 감염을 감지하는 데 중요한 역할을 하며, 다양한 건강 상태에서 흔히 볼 수 있는 세균 감염을 감지하는 데 중요한 역할을 합니다. 피부 및 비뇨기 감염에서 호흡기 및 위장 문제에 이르기까지 세균성 병원체의 정확한 식별은 치료 계획에 필수적입니다. 배양 방법의 개선과 신속한 항원 검출 등 세균 진단의 현대적 발전으로 진단 효율성이 크게 향상되었습니다. 이러한 기술이 중앙 실험실과 현장 진료소 모두에서 사용할 수 있게 됨에 따라 진단학에서 세균학의 위상이 강화되고 있습니다.

동물 유형별로는 개가 2024년 53.7%의 압도적인 점유율로 시장을 주도했습니다. 이러한 우위는 반려동물로서 반려견이 널리 사육되고 있으며, 반려견의 건강관리에 대한 투자가 증가하고 있기 때문입니다. 반려견의 만성질환 빈도가 높아지면서 당뇨병, 신장질환, 관절염, 심혈관질환 등의 진단 검사에 대한 수요가 증가하고 있습니다. 정기적인 진단이 반려견의 질병 관리에 필수적인 요소로 자리 잡으면서 이 분야 수요를 더욱 증가시키고 있습니다.

최종 용도별로는 진단 실험실이 2024년에 가장 큰 시장 점유율을 차지하며, 2025-2034년 연평균 9.1%의 연평균 복합 성장률(CAGR)로 확대될 것으로 예측됩니다. 이러한 실험실은 고급 진단 시스템을 갖추고 숙련된 전문가가 상주하여 대량의 샘플을 효율적으로 처리할 수 있습니다. 정확하고 신속하며 종합적인 결과를 제공하는 능력으로 인해 신뢰할 수 있는 진단 지원을 원하는 수의사들이 선호하고 있습니다. 반려동물을 기르는 사람들이 늘어나면서 동물의 정기적인 건강 검진을 선택하는 사람들이 늘어남에 따라 진단 실험실의 역할이 더욱 중요해지고 있습니다.

지역별로는 북미가 2024년 10억 달러로 세계 반려동물 진단 의약품 시장을 주도하고 2034년에는 23억 달러로 연평균 8.8% 성장할 것으로 예상되며, 2024년에는 미국에서만 8억 9,330만 달러를 차지합니다. 높은 반려동물 사육률과 최첨단 진단 서비스의 광범위한 보급이 이 지역 수요를 주도하고 있습니다. 또한 강력한 수의학 의료 네트워크와 동물 건강에 대한 소비자 지출 증가는 북미 시장 성과를 지속적으로 강화하고 있습니다.

경쟁 구도는 몇몇 세계 및 지역 기업에 의해 형성되고 있으며, IDEXX Laboratories, Thermo Fisher Scientific, Zoetis, Heska Corporation과 같은 주요 기업이 세계 시장의 약 60-65%를 점유하고 있습니다. 이들 기업은 광범위한 제품 포트폴리오, 지역적 범위, 연구개발에 대한 지속적인 투자를 통해 리더십을 유지하고 있습니다. 한편, 수많은 로컬 기업이 비용 효율적인 진단 솔루션을 제공하고, 제휴, 인수, 신제품 개발을 통해 제품 라인을 확장함으로써 경쟁을 심화시키고 있습니다.

The Global Companion Animal Diagnostics Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 9.3% to reach USD 5.8 billion by 2034. This growth is driven by a rising number of pet owners worldwide, a growing inclination toward pet companionship, and a surge in the diagnosis of chronic and infectious diseases in animals. With pet care becoming an integral part of households, spending on veterinary services continues to climb. Pet owners are increasingly treating animals as part of the family, which results in regular health checks, preventive care, and timely diagnosis. This cultural shift has led to a stronger focus on animal wellness, significantly pushing up the demand for advanced diagnostic tools and services.

The market expansion is also underpinned by the increasing awareness of zoonotic diseases and the importance of early diagnosis in avoiding complications. Veterinary professionals are relying more on diagnostics to assess conditions like organ dysfunction, metabolic issues, and infections, which has further fueled the growth of this sector. Moreover, technological advancements are reshaping the landscape by enabling fast, accurate, and less invasive diagnostic techniques. Innovations in veterinary diagnostics are allowing faster turnaround times and better integration with treatment strategies, making diagnostics a critical component of animal healthcare. As veterinary care infrastructure strengthens globally, the demand for diagnostic products and services is expected to remain on an upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 9.3% |

In terms of product segmentation, the market is divided into instruments and consumables. In 2024, the consumables segment dominated with a value of USD 2 billion. This dominance is due to the essential role of consumables like reagents, testing kits, slides, and tubes in each diagnostic process. Unlike instruments, consumables are required for every test, resulting in recurring purchases and consistent market revenue. As the frequency of animal testing increases across clinics and hospitals, the demand for consumables is expected to follow suit. The trend toward regular checkups and preventive screenings further boosts usage. Additionally, with more diagnostic procedures moving toward rapid and point-of-care formats, consumables tailored for single-use applications are becoming standard, pushing segmental growth.

When analyzed by application, the bacteriology segment emerged as the leading category in 2024 and is expected to reach USD 2.4 billion by 2034. This segment plays a crucial role in detecting bacterial infections in companion animals, which are commonly seen across a wide range of health conditions. From skin and urinary infections to respiratory and gastrointestinal issues, accurate identification of bacterial pathogens is essential for treatment planning. Modern advancements in bacteriological diagnostics, including improved culturing methods and rapid antigen detection, have significantly elevated diagnostic efficiency. The increasing availability of such technologies at both central labs and point-of-care facilities strengthens the position of bacteriology in the diagnostics landscape.

Based on animal type, the dogs segment led the market with a commanding share of 53.7% in 2024. This dominance is attributed to the widespread ownership of dogs as companion animals and the rising investment in their healthcare. The higher frequency of chronic diseases in dogs has resulted in increased demand for diagnostic tests for conditions such as diabetes, kidney disorders, arthritis, and cardiovascular problems. Routine diagnostics have become essential for disease management in dogs, further driving the demand within this segment.

Regarding end use, diagnostic labs held the largest market share in 2024 and are anticipated to expand at a CAGR of 9.1% from 2025 to 2034. These labs are equipped with high-end diagnostic systems and staffed with trained professionals, allowing them to handle large sample volumes efficiently. Their ability to deliver accurate, quick, and comprehensive results makes them a preferred choice for veterinarians seeking reliable diagnostic support. As the number of pet owners increases and more people opt for regular health assessments for their animals, the role of diagnostic labs becomes even more central.

Regionally, North America led the global companion animal diagnostics market with a value of USD 1 billion in 2024, projected to reach USD 2.3 billion by 2034, growing at a CAGR of 8.8%. The U.S. alone accounted for USD 893.3 million in 2024. High pet ownership rates and the widespread availability of cutting-edge diagnostic services drive demand in the region. Additionally, a strong veterinary healthcare network and rising consumer expenditure on animal wellness continue to bolster market performance in North America.

The competitive landscape is shaped by several global and regional players, with key companies such as IDEXX Laboratories, Thermo Fisher Scientific, Zoetis, and Heska Corporation collectively holding around 60% to 65% of the global market. These firms maintain their leadership through broad product portfolios, geographic reach, and continuous investment in research and development. Alongside them, numerous local players are intensifying competition by offering cost-effective diagnostic solutions and expanding their product lines through partnerships, acquisitions, and new product development.