알루미늄 허니콤 패널 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측

Aluminum Honeycomb Panels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1773313

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 235 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

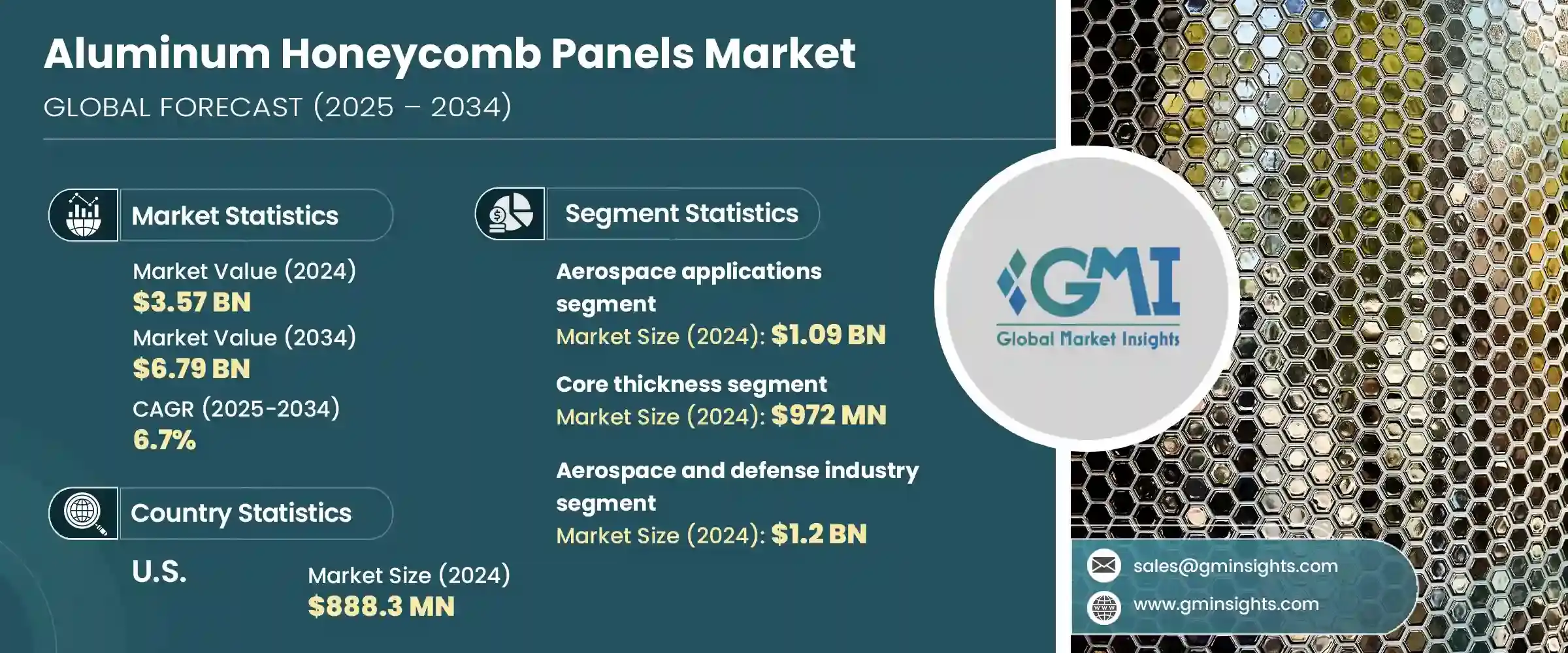

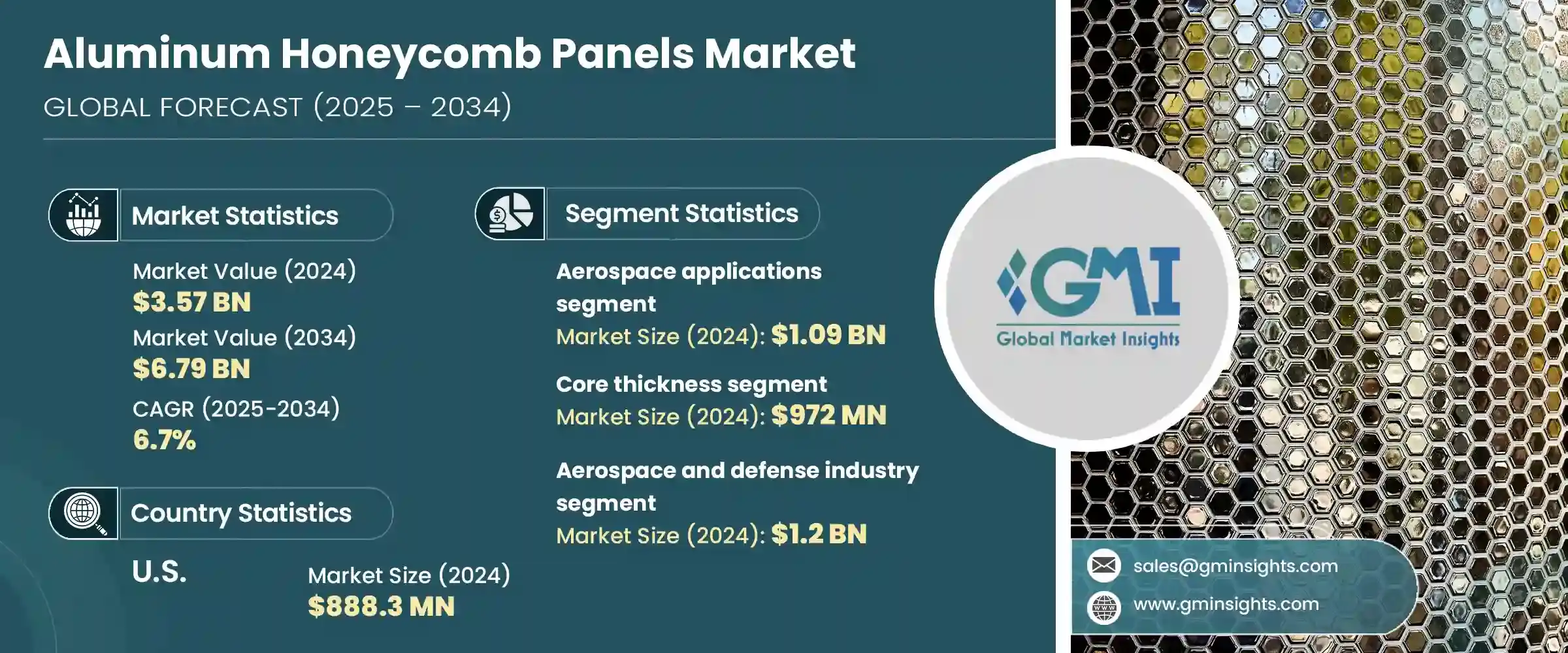

세계의 알루미늄 허니콤 패널 시장 규모는 2024년에 35억 7,000만 달러를 달성하였고, CAGR 6.7%로 성장하여 2034년까지는 67억 9,000만 달러에 이를 것으로 예측되고 있습니다.

이 성장은 주로 고강도와 저중량을 결합한 재료를 필요로 하는 여러 고성능 산업에 걸친 용도 증가에 의해 발생합니다. 수요는 특히 효율성과 구조적 완전성이 핵심인 분야에서 특히 두드러집니다. 이 패널은 구조물의 무게를 크게 증가시키지 않으면서 에너지 흡수, 내구성 및 다양한 응력에 대한 내성에 대한 엄격한 요구사항을 충족시키는 성질로 널리 인정받았습니다.

산업계가 에너지 절약과 지속 가능성 목표를 추구하는 가운데 경량이면서 견고한 소재에 대한 수요가 높아지고 있으며, 알루미늄 허니콤 패널은 이상적인 솔루션이 되고 있습니다. 이러한 재료를 사용하는 경향이 높아지고 있는 것도, 세계 시장에서의 알루미늄 허니콤 패널의 중요성 증가를 뒷받침하고 있습니다. 재활용성, 내화성, 단열성으로 인해 그 매력은 한층 더 높아지고 있으며 기능성과 환경친화성 모두가 요구되는 폭넓은 용도로 적합합니다.

시장 범위

시작연도

2024년

예측연도

2025-2034년

시작금액

35억 7,000만 달러

예측금액

67억 9,000만 달러

CAGR

6.7%

항공우주 분야에서는 알루미늄 허니컴 패널은 경량이며 고강도라는 필수 조건을 충족하므로 급속히 보급되고 있습니다. 특히 항공제조에서 중요한 설계의 유연성을 향상하는데 도움이 됩니다.

이러한 재료는 또한 건축 및 건설 업계에서도 보급되고 있습니다. 경량이며 강성이 높기 때문에 설치가 용이하고 수명이 길며, 구조적 역할에 있어서 뛰어난 성능을 발휘합니다. 또한 내연성 및 방음성으로 인해 클래딩 시스템, 천장, 칸막이용으로 사용되고 있습니다. 그린 건축 기준이나 지속 가능한 아키텍처로의 전환은 특히 신흥 경제국에서의 건축 관행에서 알루미늄 허니콤 패널의 채용율 향상으로 이어졌습니다.

제품 사양의 관점에서 코어 두께, 합금 유형, 셀 구성의 혁신을 통해 시장이 성장하고 있습니다. 다양한 코어 수치를 통해 맞춤형 하중 부담 특성을 구현할 수 있으며, 특정 합금은 내식성을 높여 구조성능을 최적화합니다.

최종 용도별로는 항공우주 및 방위산업이 2024년 시장에서 가장 큰 점유율을 차지하며 시장 규모 12억 달러를 달성하였고, 시장 점유율은 32.4%였습니다. 국방계획에 대한 투자 증가와 선진방위시스템을 위한 경량재료에 대한 중요성이 높아지고 있습니다.

또한 해양, 철도, 물류 등의 분야에서도 내식성, 열안정성, 가공용이성의 필요성으로 패널의 이용이 확대되고 있습니다. 패널은 또한 화물 시스템에서 사용하기에 적합합니다. 또한 산업기기 제조업체도 기밀기기의 구조프레임과 인클로저의 제조에 이러한 패널을 사용하고 있으며, 그 범용성과 일관적인 성능이 부각되고 있습니다.

미국의 알루미늄 허니콤 패널 시장은 2024년에는 8억 8,830만 달러를 달성하였고, 2025년부터 2034년에 걸쳐 CAGR 6.5%를 보일 것으로 예측됩니다. 또한 전기자동차와 군용 업그레이드에 대한 투자가 증가하고 있으며 시장 확대에 유리한 조건이 갖추어지고 있습니다.

경쟁구도에는 선진적인 제조, 다양한 제품 포트폴리오, 공급망에 걸친 전략적 파트너십의 조합에 의해 시장을 독점하고 있는 주요 복합재료 제조업체와 소재 제조업체가 명성을 높이고 있습니다. 세계의 규제기준과 지속 가능성 목표에 맞게 생산함으로써, 이들 기업은 경쟁력을 유지하고 대량 생산과 고사양 시장 모두에 대한 수요에 대응하고 있습니다.

목차

제1장 조사방법

시장의 범위와 정의

조사 디자인

조사 접근

데이터 수집방법

데이터 마이닝 소스

세계

지역/국가

기본 추정과 계산

기준연도 계산

시장 예측의 주요 동향

1차 조사와 검증

1차 정보

예측모델

조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

업계의 잠재적 리스크 및 과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(주 : 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속 가능성과 환경 측면

지속 가능한 관행

폐기물 감축 전략

생산에서의 에너지 효율

환경친화적인 노력

탄소발자국의 고려

제4장 경쟁구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

기업 매트릭스 분석

주요 시장기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병과 인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측, 용도(2021-2034년)

주요 동향

항공우주 용도

상용항공

항공기 바닥 시스템

인테리어 패널과 부품

구조 용도

군사 및 방위항공

우주 및 위성 용도

자동차 용도

전기자동차 부품

충돌 흡수 시스템

구조 보강

내부 및 외부 패널

건설과 아키텍처

커튼월 시스템

외관 클래딩

인테리어 디자인 용도

지붕과 구조 요소

해양 용도

조선 및 해군 용도

요트 및 레저 보트의 제조

해양 플랫폼 건설

산업 용도

기계설비 제조

공구와 지그

클린룸 및 실험실 용도

교통과 철도

고속철도 용도

도시교통시스템

상용차 용도

기타

가구와 디자인

신재생에너지의 응용

스포츠 및 레크리에이션 용품

제6장 시장 추계 및 예측 : 코어 유형과 사양별(2021-2034년)

주요 동향

코어 두께

매우 얇음(5mm-10mm)

표준(11mm-25mm)

중간(26mm-50mm)

두꺼움(51mm-100mm)

고내구성(100mm 이상)

알루미늄 합금 유형

3003 합금(상용등급)

5052 합금(항공우주급)

5056 합금(고성능 용도)

기타 특수 합금

셀의 크기와 구성

표준 육각형 셀

마이크로셀 구성

커스텀 셀 지오메트리

판재 소재

알루미늄판재

복합판재

하이브리드 구성

패널의 사이즈와 치수

표준패널

대형패널

커스텀사이즈 용도

제7장 시장 추계 및 예측 : 최종 이용 산업별(2021-2034년)

주요 동향

항공우주 및 방위산업

자동차산업

건축 및 건설업계

상업건설

주택용도

인프라 개발

해양 및 조선업

상업수송

해군 및 방위용도

레크리에이션용 마린마켓

해외 에너지부문

운송 및 물류

철도수송

상용차

대중교통기관

공업제조업

기계설비

클린룸 용도

특수 산업용도

기타

에너지와 발전

스포츠 및 레크리에이션

가구 및 인테리어 디자인

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동 및 아프리카

제9장 기업 프로파일

3A Composites Holding AG

Hexcel Corporation

Plascore Inc.

Alcoa Corporation

Novelis Inc.

Hunter Douglas NV

Toray Advanced Composites

Euro-Composites SA

Collins Aerospace(Raytheon Technologies)

Argosy International Inc.

Alucoil SL

Pacific Panels Inc.

Benecor Inc.

Liming Honeycomb Composites Co., Ltd.

KUMZ(Kamensk-Uralsky Metallurgical Works)

Eco Earth Solutions

Renoxbell Group

Foshan Alucrown Building Materials Co., Ltd.

Mass Transit Equipment LLP

UACJ Corporation

Schweiter Technologies AG

Shinko-North Co., Ltd.

Guangzhou Aloya Renoxbell Aluminum Co., Ltd.

Advanced Custom Manufacturing

Zodiac Aerospace(Safran)

B/E Aerospace

Triumph Group Inc.

The NORDAM Group LLC

Flatiron Panel Products

Corex-Honeycomb

3M Company

Armacell International SA

MC Gill Corporation

TenCate Advanced Composites

Oerlikon Metco

Boeing Encore Interiors LLC

Safran SA

Rockwell Collins(Collins Aerospace)

Avcorp Industries Inc.

Yamaton Corporation

Shuangdie Group

SPEE3D

Zimmermann Group

BoDo Plastics

Duramax

LIDA PLASTIC INDUSTRY

Gayatri Corporation

Viva Composite Panel Pvt Ltd

Go Alubuild Pvt Ltd

Kukreja Brothers

Uniwell International Enterprises Corp.

Prance Building Materials

DJ Aluminum

Alumetal

TOPCOMB

Chaluminium

Jixiang Aluminum

CSM

영문 목차

영문목차

The Global Aluminum Honeycomb Panels Market was valued at USD 3.57 billion in 2024 and is estimated to grow at a CAGR of 6.7% to reach USD 6.79 billion by 2034. This growth is primarily driven by increasing applications across multiple high-performance industries that require materials combining strength with low weight. The demand is particularly pronounced in sectors where performance efficiency and structural integrity are key, such as aerospace, automotive, construction, and industrial manufacturing. These panels are widely recognized for their ability to meet stringent requirements related to energy absorption, durability, and resistance to various stresses without significantly increasing the weight of structures.

As industries continue to pursue energy-saving and sustainability goals, the demand for lightweight yet robust materials is rising, which makes aluminum honeycomb panels an ideal solution. The rising trend of using these materials in modern infrastructure, transportation systems, and specialized equipment housing further supports their growing relevance in global markets. Their appeal is enhanced by their recyclability, fire resistance, and thermal insulation properties, making them suitable for a wide range of applications that require both functionality and environmental responsibility.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$3.57 billion

Forecast Value

$6.79 billion

CAGR

6.7%

In the aerospace segment, aluminum honeycomb panels are gaining rapid traction as they fulfill essential criteria such as lightweight and high strength. The aerospace applications segment alone was valued at USD 1.09 billion in 2024 and is projected to register a CAGR of 7.5% from 2025 to 2034. These panels help enhance fuel efficiency and enable improved design flexibility, which is critical in aviation manufacturing. Their usage extends to interior partitions, flooring systems, and structural elements, where weight reduction is crucial without compromising performance. As aircraft manufacturers increase focus on cost-efficient and fuel-saving technologies, the preference for aluminum honeycomb structures continues to strengthen.

These materials are also finding growing acceptance in the building and construction industry. Their combination of low weight and high rigidity allows for easier installation, longer lifespan, and superior performance in structural roles. Their fire-resistant and sound-insulating features further contribute to their use in cladding systems, ceilings, and partitions, particularly in commercial and institutional buildings. The shift toward green building codes and sustainable architecture has led to higher adoption of aluminum honeycomb panels in construction practices, especially in developed economies.

From a product specification standpoint, the market is advancing through innovations in core thickness, alloy types, and cell configurations. The core thickness segment, which was valued at USD 972 million in 2024, is expected to grow at a CAGR of 7% over the forecast period. Varying core dimensions offer customized load-bearing capabilities across applications, while specific alloys enhance corrosion resistance and optimize structural performance. Manufacturers are also developing tailored panel shapes and sizes to cater to specific design or technical requirements. These innovations are making aluminum honeycomb panels more adaptable to complex environments across multiple industries.

In terms of end-use, the aerospace and defense industry accounted for the largest share of the market in 2024, valued at USD 1.2 billion and holding a 32.4% market share. This segment is expected to expand at a CAGR of 7.2% through 2034. The growth is fueled by increased investment in national defense programs and a growing emphasis on lightweight materials for advanced defense systems. In the automotive industry, particularly in the electric vehicle segment, the panels contribute to extended range and better performance by reducing overall vehicle weight.

Additionally, their growing usage in sectors like marine, rail, and logistics is driven by the need for corrosion resistance, thermal stability, and ease of fabrication. These characteristics make the panels well-suited for use in ship interiors, train compartments, and cargo systems. Industrial manufacturers also rely on these panels to build structural frames and enclosures for sensitive equipment, which highlights their versatility and performance consistency.

In the United States, the aluminum honeycomb panels market was valued at USD 888.3 million in 2024 and is projected to grow at a CAGR of 6.5% from 2025 to 2034. The country's position as a global hub for aircraft production, along with rising investments in electric vehicles and military upgrades, is creating favorable conditions for market expansion. The emphasis on environmentally friendly construction practices and energy efficiency in commercial buildings further supports domestic demand.

The competitive landscape features major composite and material producers who dominate the market through a combination of advanced manufacturing, diverse product portfolios, and strategic partnerships across supply chains. These companies continuously invest in research and development to improve product strength, fire resistance, and adaptability to meet evolving industrial standards. By aligning production with global regulatory norms and sustainability targets, these firms maintain their competitive edge and cater to both high-volume and high-specification market demands. Their established relationships with OEMs and contractors ensure long-term business continuity, while their commitment to automation and quality control reinforces their leadership in critical end-use segments.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Application

2.2.3 Core Type and Specifications

2.2.4 End use Industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)