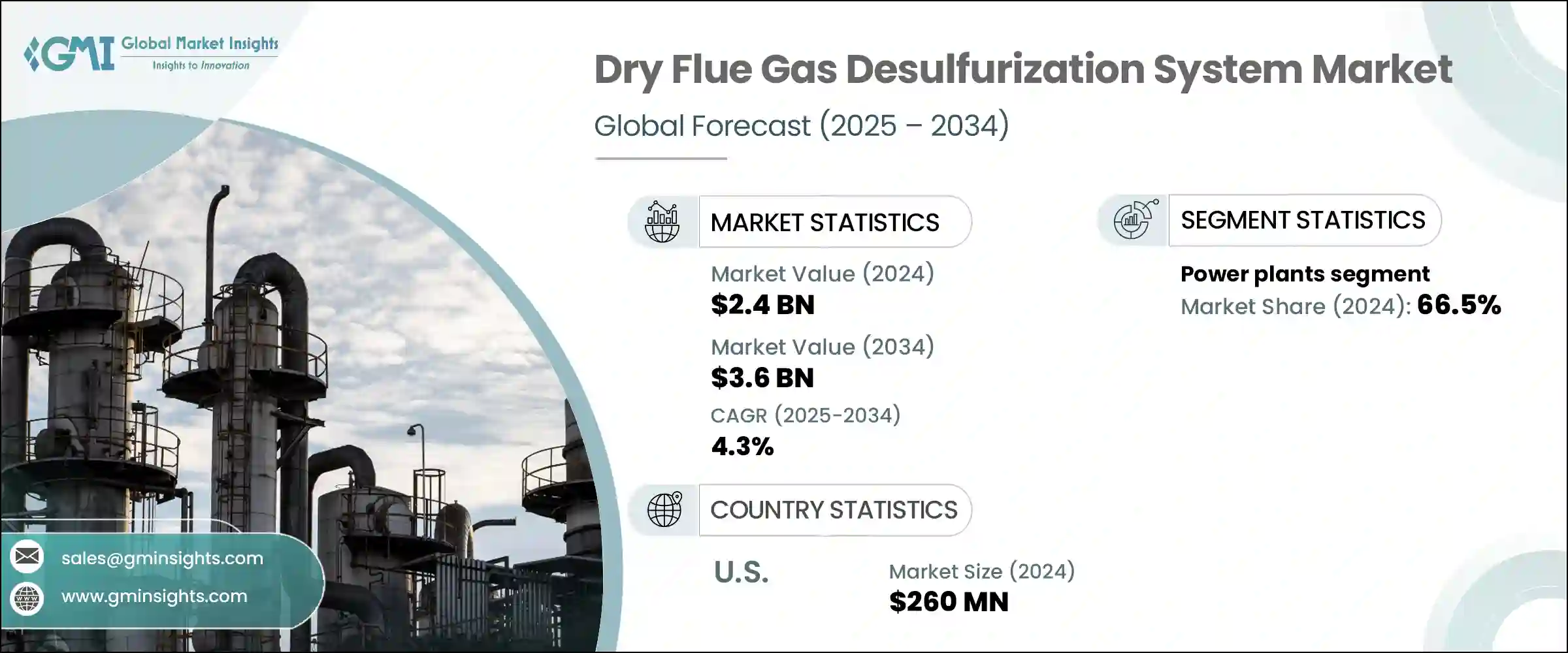

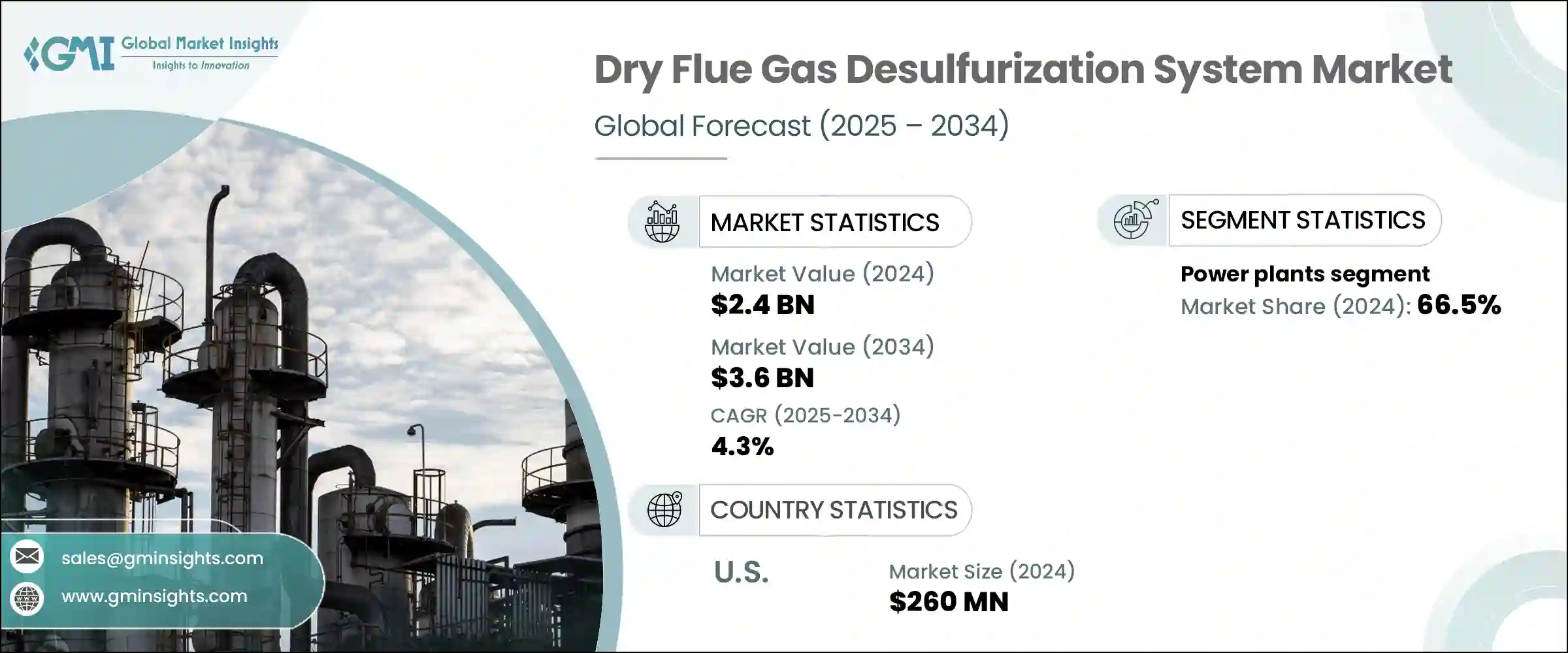

건식 배연 탈황 장치 세계 시장 규모는 2024년에 24억 달러로 평가되었고, CAGR 4.3%로 성장하여 2034년에는 36억 달러에 이를 것으로 예측됩니다.

시장 성장의 원동력은 강화된 환경 규제와 세계 청정 생산의 추진으로 인해 효율적인 이산화황(SO2) 배출 억제에 대한 산업계 수요가 증가하고 있다는 점입니다. 이러한 건식 FGD 기술은 물 소비량 감소, 시스템 복잡성 감소, 기존 인프라에 대한 통합 간소화 등 여러 가지 이점을 제공합니다. 발전, 화학 제조, 시멘트 제조, 금속 가공 등의 산업에서 규정 준수 및 지속가능성 전략의 일환으로 이러한 시스템의 도입이 증가하고 있습니다.

건식 탈황 시스템의 성능과 신뢰성은 기술 업그레이드를 통해 지속적으로 개선되고 있으며, 생산성을 저하시키지 않고 배출량을 줄이려는 기업에게 선호되는 선택이 되고 있습니다. 대기 오염 감소에 대한 여론과 규제 압력이 증가함에 따라 신흥 경제국의 산업계는 건식 탈황 장치에 대한 수요가 증가하고 있습니다. 건식 탈황 기술의 컴팩트한 설계와 모듈화 기능으로 기존 설비의 개조가 용이합니다. 유럽과 북미와 같은 지역에서는 특히 규제 준수와 환경 성능이 우선시되는 강력한 정책 시행과 녹색 이니셔티브가 확산되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 24억 달러 |

| 예측 금액 | 36억 달러 |

| CAGR | 4.3% |

용도별로는 발전 부문이 2024년 66.5%의 가장 큰 시장 점유율을 차지하며 2034년까지 3.6%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 이러한 성장은 주로 오래된 석탄 기반 발전소를 신속하고 비용 효율적으로 개조해야 하는 적극적인 배출 의무화로 인해 발생합니다. 건식 탈황 시스템은 물 사용량을 최소화하고, 설계를 간소화하며, 설치 기간을 단축하는 이상적인 시스템입니다. 특히, 전 세계적으로 에너지 전환이 진행되는 가운데, 토목 공사나 플랜트 오버홀에 많은 투자를 하지 않고도 배출 기준을 충족시킬 수 있습니다.

미국 건식 배연 탈황 장치 시장 규모는 2024년 2억 6,000만 달러에 달할 것으로 예측됩니다. 이 시장의 호조는 엄격한 EPA 규제와 산업 공정에서 황 배출 감소에 대한 강조에 힘입은 것입니다. 건식 탈황 기술은 물 절약 기능, 기존 배기 가스 흐름에 쉽게 설치할 수 있다는 점, 업그레이드 시 가동 중단이 적다는 점 때문에 이 시장에서 두각을 나타내고 있습니다. 환경적 책임이 강화되는 가운데, 이러한 시스템은 미국 산업계가 규정 준수 요건을 효율적으로 충족하는 데 중요한 역할을 하고 있습니다.

건식 배연 탈황 장치 시장을 형성하는 주요 기업으로는 Mitsubishi Heavy Industries, GE Vernova, CECO Environmental, Babcock &Wilcox Enterprises 등이 있습니다. 건식 배연 탈황 장치 시장의 기업들은 에너지 생산자와의 파트너십 형성, 턴키 개조 솔루션 제공, 디지털 모니터링 및 예지보전 툴을 포함한 서비스 포트폴리오 확장 등의 전략적 이니셔티브에 집중하고 있습니다.

모듈식 시스템 설계와 물 효율이 높은 기술을 우선시함으로써 기업은 물이 부족한 지역에서 운영되는 산업의 현실적인 요구에 대응하고 있습니다. 연구개발에 대한 투자는 시스템 효율성 향상, 에너지 소비 감소, SO2 회수율 향상을 목표로 하고 있습니다. 제조업체들은 또한 산업이 확장되고 대기질 규제가 강화되고 있는 신흥 시장을 겨냥해 세계 시장 진출을 확대하고 있습니다. 자동화 및 스마트 제어의 통합을 통해 이들 기업은 산업별 배출 규제 기준과 운영상의 제약에 따라 보다 맞춤화된 컴플라이언스 대응 솔루션을 제공할 수 있게 되었습니다.

The Global Dry Flue Gas Desulfurization System Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 3.6 billion by 2034. The market growth is fueled by increasing industrial demand for efficient sulfur dioxide (SO2 ) emission control, driven by tightening environmental regulations and the global push toward cleaner production. These dry FGD technologies provide several advantages, including low water consumption, reduced system complexity, and simplified integration into existing infrastructure. Industries such as power generation, chemical manufacturing, cement production, and metal processing are increasingly installing these systems as part of compliance and sustainability strategies.

Technological upgrades continue to improve the performance and reliability of dry FGD systems, making them a preferred choice for businesses aiming to lower emissions without compromising productivity. As public and regulatory pressure mounts to cut air pollution, industries in fast-developing economies are seeing growing demand for these systems. Retrofitting existing facilities has become easier due to the compact design and modular capabilities of dry FGD technologies. In regions like Europe and North America, strong policy enforcement and green initiatives are leading to widespread adoption, especially where regulatory compliance and environmental performance are prioritized.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 4.3% |

In terms of application, the power generation segment held the largest market share at 66.5% in 2024 and is projected to grow at a CAGR of 3.6% through 2034. This growth is primarily driven by aggressive emission mandates that require older coal-based plants to be retrofitted quickly and cost-effectively. Dry FGD systems remain an ideal fit, offering minimal water usage, streamlined design, and quicker installation timelines. Their scalable, modular nature provides utilities with the flexibility to meet emission standards without heavy investment in civil engineering or plant overhaul, especially amid a broader global energy transition.

United States Dry Flue Gas Desulfurization System Market generated USD 260 million in 2024. The market's strength is supported by rigorous EPA regulations and a strong emphasis on reducing sulfur emissions in industrial processes. Dry FGD technologies stand out in this market for their water-saving features, ease of installation in pre-existing flue gas channels, and reduced operational interruptions during upgrades. As environmental accountability intensifies, these systems are playing a vital role in helping U.S. industries meet compliance requirements with efficiency.

Prominent players shaping the Dry Flue Gas Desulfurization System Market include Mitsubishi Heavy Industries, GE Vernova, CECO Environmental, and Babcock & Wilcox Enterprises. Companies in the dry flue gas desulfurization system market are focusing on strategic initiatives such as forming partnerships with energy producers, offering turnkey retrofit solutions, and expanding service portfolios to include digital monitoring and predictive maintenance tools.

By prioritizing modular system designs and water-efficient technologies, firms are addressing the practical needs of industries operating in water-scarce regions. Investments in R&D aim to enhance system efficiency, reduce energy consumption, and improve SO2 capture rates. Manufacturers are also expanding their global footprints by targeting emerging markets with industrial expansion and strict air quality regulations. Leveraging automation and smart control integration has allowed these companies to deliver more tailored, compliance-ready solutions that align with industry-specific emission control standards and operational constraints.