일회용 요실금 용품 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Disposable Incontinence Products Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1766312

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 200 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

세계의 일회용 요실금 용품 시장은 2024년 144억 달러로 평가되었으며 CAGR 6.9%로 성장해 2034년까지 282억 달러에 이를 것으로 추정됩니다.

이 일관된 시장 확대의 배경에는 요실금을 경험하는 사람 증가, 치료 및 관리 옵션에 대한 의식이 높아지고, 제조업체에 의한 지속적인 제품의 진보가 있습니다. 또한, 전자상거래의 발전은 구매 프로세스를 간소화하고, 사용자는 눈에 띄지 않고 제품을 이용할 수 있게 되었습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

144억 달러

예측 금액

282억 달러

CAGR

6.9%

일회용 요실금 솔루션은 흡수 패드, 성인용 서류, 보호복 등의 제품을 통해 불수의적인 방광과 창자의 누출을 관리할 수 있도록 설계되었습니다. 수술 후 환자, 만성 실금 환자에게 편안함, 존엄성 및 위생을 향상시키는 것입니다.

보호용 요실금 의류 부문은 시장을 선도했으며, 2024년에는 광범위한 채용과 사용 편의성으로 121억 달러로 평가되었습니다. 위생적이고 누설이 어려운 구조는 이용자가 활동적이고 자신감 넘치는 라이프스타일을 유지하는데 도움이 됩니다.

요실금 분야는 2024년 56.7%의 점유율을 차지했습니다. 고령화 사회에서의 요실금의 높은 유병률과 지속성은 제품 수요에 크게 기여하고 있습니다. 일회용 요실금 용품은 실용적이고 위생적 인 옵션을 제공합니다.

미국의 일회용 요실금 용품 시장은 2024년 27억 달러로 평가되었습니다.

일회용 요실금 용품 세계 시장에서 주요 기업은 Essity, BD, Coloplast, CardinalHealth, B Braun, Ontex, Attends, FUBURG, UROCARE, MEDLINE, Kimberly-Clark, cobaTec, ABENA, unicharm, Hollister 등이 있습니다. 일회용 요실금 용품 분야의 기업은 제품 혁신, 지속가능성, 유통 확대에 주력함으로써 시장에서의 지위를 높이고 있습니다. 전략적 제휴는 조기 채용 촉진에 도움이 되고 있습니다. 또한 각사는 현대의 소비자의 기호에 맞는 정기 구입형 모델이나 눈에 띄지 않는 배송 서비스를 제공하기 위해, 온라인으로의 프레즌스 확대를 도모하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

업계에 미치는 영향요인

성장 촉진요인

세계에서 실금의 유병률이 증가

정부에 의한 지원적인 상환정책

만성질환 발생률 증가와 노인 인구 증가

최근 기술 진보와 신제품 개발

업계의 잠재적 위험 및 과제

신흥국에서의 인지도와 제품 입수성의 부족

시장 기회

재택 헬스케어와 E-Commerce의 유통 채널의 확대

지속가능성을 중시한 생분해성과 친환경 솔루션

성장 가능성 분석

규제 상황

북미

유럽

세계 기타 지역

기술과 혁신의 상황

현재의 기술 동향

신흥기술

가격 동향

지역별

제품별

미래 시장 동향

상환 시나리오

상환 정책이 시장 성장에 미치는 영향

소비자 행동 분석

갭 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

세계

북미

유럽

세계 기타 지역

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

주요 발전

합병인수

파트너십 및 협업

신제품 발매

확장 계획

제5장 시장 추계 및 예측 : 제품별, 2021-2034년

주요 동향

실금 보호용 의류

일회용 보호 속옷

일회용 성인용 기저귀

옷감 성인용 기저귀

일회용 패드 및 라이너

남성용 보호용품

방광 제어 패드

실금 라이너

벨트 부착 및 미부착 속옷

일회용 언더패드

요도 카테터

유치 카테터(폴리 카테터)

간헐 카테터

외부 카테터

소변 가방

다리용 소변 가방

침대 사이드 소변 가방

제6장 시장 추계 및 예측 : 용도별, 2021-2034년

주요 동향

요실금

편실금

이중 실금

제7장 시장 추계 및 예측 : 실금 유형별, 2021-2034년

주요 동향

스트레스

혼합

충동

기타 실금 유형

제8장 시장 추계 및 예측 : 질병별, 2021-2034년

주요 동향

여성의 건강

임신과 출산

폐경

자궁 적출술

기타 여성의 건강 질환

만성 질환

정신장애

양성 전립선 비대증

방광암

기타 병

제9장 시장 추계 및 예측 : 재료별, 2021-2034년

주요 동향

면직물

초흡수제

플라스틱

라텍스

기타 재료

제10장 시장 추계 및 예측 : 남녀별, 2021-2034년

주요 동향

여성

남성

제11장 시장 추계 및 예측 : 연령별, 2021-2034년

주요 동향

20세 미만

20-39세

40-59세

60-79세

80세 이상

제12장 시장 추계 및 예측 : 유통 채널별, 2021-2034년

주요 동향

소매점

전자상거래

제13장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

주요 동향

병원

간병 시설

장기 케어 센터

외래수술센터(ASC)

기타 최종 용도

제14장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

네덜란드

아시아태평양

중국

일본

인도

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

제15장 기업 프로파일

ABENA

Attends

B Braun

BD

CardinalHealth

Coloplast

convaTec

essity

FUBURG

Hollister

Kimberly-Clark

MEDLINE

Ontex

unicharm

UROCARE

JHS

영문 목차

영문목차

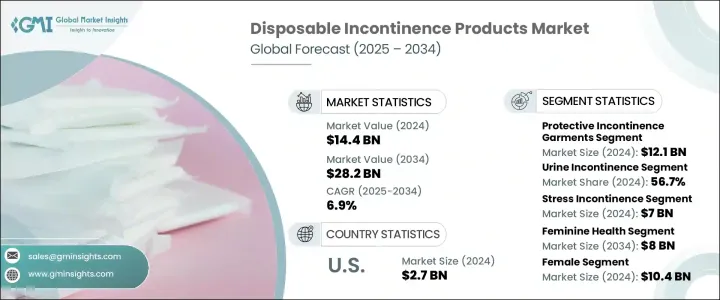

The Global Disposable Incontinence Products Market was valued at USD 14.4 billion in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 28.2 billion by 2034.

This consistent market expansion is fueled by the growing number of individuals experiencing urinary incontinence, rising awareness regarding treatment and management options, and continuous product advancements by manufacturers. Companies are prioritizing innovation in materials that are not only highly absorbent and skin-compatible but also biodegradable, aligning with both healthcare efficacy and environmental responsibility. In addition, the growth of e-commerce has simplified purchasing processes, enabling users to obtain products discreetly. This combination of convenience, functionality, and accessibility is accelerating demand across multiple care settings, from hospitals to home environments, contributing to the overall growth trajectory of the market.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$14.4 Billion

Forecast Value

$28.2 Billion

CAGR

6.9%

Disposable incontinence solutions are designed to help individuals manage involuntary bladder or bowel leakage through products such as absorbent pads, adult briefs, and protective garments. These items enhance comfort, dignity, and hygiene, especially for elderly users, post-surgical patients, and people with chronic incontinence. Designed for easy use and disposal, they serve both clinical and home care needs, offering reliable absorption and minimal discomfort.

The protective incontinence garments segment led the market and was valued at USD 12.1 billion in 2024, owing to its wide adoption and ease of use. These garments are preferred across hospitals, long-term care centers, and homes due to their reliable performance and comfort. Their absorbent, hygienic, and leak-resistant structure helps users maintain an active and confident lifestyle. They are available in multiple formats to address varying severity levels of incontinence, which enhances their appeal to both patients and caregivers.

Urine incontinence segment held a 56.7% share in 2024. Its high prevalence and persistent nature across aging populations significantly contribute to product demand. Effective solutions are necessary to manage prolonged episodes of urine leakage, with disposable incontinence products offering a practical and hygienic option. The growing number of elderly individuals dealing with such health concerns continues to boost the segment's prominence in the market.

United States Disposable Incontinence Products Market was valued at USD 2.7 billion in 2024. Increasing cases of stress urinary incontinence, especially among aging women, are pushing product demand. Factors such as menopause, obesity, and childbirth have contributed to pelvic floor complications, prompting women to seek treatment. The availability of advanced healthcare facilities, greater pelvic health awareness, and favorable reimbursement systems are further supporting market expansion in the country.

Key players in the Global Disposable Incontinence Products Market include Essity, BD, Coloplast, CardinalHealth, B Braun, Ontex, Attends, FUBURG, UROCARE, MEDLINE, Kimberly-Clark, convaTec, ABENA, unicharm, and Hollister. Companies in the disposable incontinence products space are enhancing their market position by focusing on product innovation, sustainability, and distribution expansion. Many are investing in R&D to develop eco-friendly materials, odor-control technology, and ultra-thin, high-absorption products that increase user comfort and discretion. To meet the evolving needs of aging populations, players are launching tailored product lines catering to different levels of incontinence severity. Strategic collaborations with healthcare providers and caregivers help promote early adoption. Additionally, firms are expanding their online presence to offer subscription-based models and discreet delivery services, which resonate with modern consumer preferences.

Table of Contents

Chapter 1 Methodology and Scope

1.1 Market scope and definitions

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Product

2.2.3 Application

2.2.4 Incontinence type

2.2.5 Disease

2.2.6 Material

2.2.7 Gender

2.2.8 Age group

2.2.9 Distribution channel

2.2.10 End Use

2.3 CXO perspectives: strategic imperatives

2.3.1 Key decision points for industry executives

2.3.2 Critical success factors for market players

2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Value addition at each stage

3.1.3 Factor affecting the value chain

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.1.1 Growing prevalence of incontinence across the globe

3.2.1.2 Supportive reimbursement policies by governments

3.2.1.3 Increasing incidence of chronic diseases coupled with rising elderly population

3.2.1.4 Recent technological advancements and new product developments

3.2.2 Industry pitfalls and challenges

3.2.2.1 Lack of awareness and product availability in emerging countries

3.2.3 Market opportunities

3.2.3.1 Expansion of home healthcare and e-commerce distribution channels

3.2.3.2 Sustainability-driven biodegradable and eco-friendly solutions

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Rest of the world

3.5 Technology and innovation landscape

3.5.1 Current technological trends

3.5.2 Emerging technologies

3.6 Price trends

3.6.1 By region

3.6.2 By product

3.7 Future market trends

3.8 Reimbursement scenario

3.8.1 Impact of reimbursement policies on market growth

3.9 Consumer behaviour analysis

3.10 Gap analysis

3.11 Porter's analysis

3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 Global

4.2.2 North America

4.2.3 Europe

4.2.4 Rest of the world

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers and acquisitions

4.6.2 Partnerships and collaborations

4.6.3 New product launches

4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

5.1 Key trends

5.2 Protective incontinence garments

5.2.1 Disposable protective underwear

5.2.2 Disposable adult diaper

5.2.3 Cloth adult diaper

5.2.4 Disposable pads and liners

5.2.4.1 Male guards

5.2.4.2 Bladder control pads

5.2.4.3 Incontinence liners

5.2.4.3.1 Belted and beltless undergarments

5.2.4.3.2 Disposable under pads

5.3 Urinary catheter

5.3.1 Indwelling (foley) catheter

5.3.2 Intermittent catheter

5.3.3 External catheter

5.4 Urine bag

5.4.1 Leg urine bag

5.4.2 Bedside urine bag

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

6.1 Key trends

6.2 Urine incontinence

6.3 Fecal incontinence

6.4 Dual incontinence

Chapter 7 Market Estimates and Forecast, By Incontinence Type, 2021 – 2034 ($ Mn)

7.1 Key trends

7.2 Stress

7.3 Mixed

7.4 Urge

7.5 Other incontinence types

Chapter 8 Market Estimates and Forecast, By Disease, 2021 – 2034 ($ Mn)

8.1 Key trends

8.2 Feminine health

8.2.1 Pregnancy and childbirth

8.2.2 Menopause

8.2.3 Hysterectomy

8.2.4 Other feminine health diseases

8.3 Chronic disease

8.4 Mental disorders

8.5 Benign prostatic hyperplasia

8.6 Bladder cancer

8.7 Other diseases

Chapter 9 Market Estimates and Forecast, By Material, 2021 – 2034 ($ Mn)

9.1 Key trends

9.2 Cotton fabrics

9.3 Super absorbents

9.4 Plastic

9.5 Latex

9.6 Other materials

Chapter 10 Market Estimates and Forecast, By Gender, 2021 – 2034 ($ Mn)

10.1 Key trends

10.2 Female

10.3 Male

Chapter 11 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

11.1 Key trends

11.2 40 to 59 years

11.3 60 to 79 years

11.4 20 to 39 years

11.5 Below 20 years

11.6 80+ years

Chapter 12 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

12.1 Key trends

12.2 Retail stores

12.3 E-commerce

Chapter 13 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

13.1 Key trends

13.2 Hospital

13.3 Nursing facilities

13.4 Long-term care centers

13.5 Ambulatory surgical centers

13.6 Other end users

Chapter 14 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)