초고온 세라믹 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)

Ultra-High Temperature Ceramics (UHTCs) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1766211

리서치사:Global Market Insights Inc.

발행일:2025년 06월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

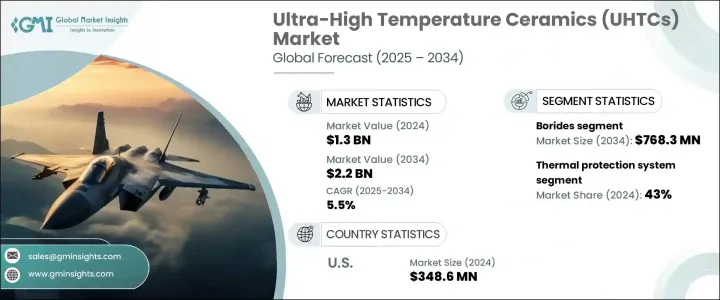

세계 초고온 세라믹 시장은 2024년 13억 달러로 평가되었으며, CAGR 5.5%로 성장하여 2034년에는 22억 달러에 이를 것으로 추정되고 있습니다. 기존의 재료가 고장나는 환경에서는 불가결합니다. 이 세라믹은 현재 고열 시스템에서 에너지 효율을 높이고 지속가능성의 목표를 달성하는데 있어서 매우 중요한 역할을 하고 있습니다. 그 용도는 선진적 추진력, 고속 비행 시스템, 차세대의 열 보호 응용 분야에서 확대되고 있습니다.

산업이 성능을 중시하고 배출을 줄이는 기술 혁신으로 전환함에 따라 UHTC에 대한 수요가 증가하고 있습니다. 세계의 군사 전략의 진화와 우주 탐사에 대한 주목이 높아짐에 따라 열에 강한 재료에 대한 요구가 가속화되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

13억 달러

예측 금액

22억 달러

CAGR

5.5%

붕소화물 부문은 2024년에 4억 5,610만 달러로 평가되었고, 2034년에는 7억 6,830만 달러로 성장할 것으로 예측됩니다. 이 부문은 뛰어난 열전도성, 탁월한 내산화성, 초고융점으로 우위를 유지하며, 최고 수준의 성능이 요구되는 용도에 최적입니다. UHTC 중에서도 붕소화물은 표준 세라믹이 견딜 수 있는 범위를 훨씬 뛰어넘는 기계적 부하와 온도를 견딜 수 있는 능력을 가지고 있기 때문에 가혹한 환경에서 특히 높게 평가되고 있습니다. 이러한 특성 때문에 붕소화물은 신뢰성이 중요시되는 추진 시스템이나 열 장벽에서 선호되는 재료 클래스가 되고 있습니다.

열 보호 시스템 부문은 43%의 점유율을 차지하며 여전히 주요 용도 부문입니다. 극초음속 비행과 우주 미션과 같은 매우 혹독한 환경에서 구조적 및 열적 무결성을 유지할 수 있는 재료에 대한 요구가 증가하고 있는 것이 이 부문에서 UHTC 수요에 박차를 가하고 있습니다. 지속적인 공기역학적 스트레스, 격렬한 마찰열, 급속한 대기 전이에 따라 성능을 발휘하는 UHTC의 능력은 절대적인 열 제어가 필요한 시스템에 필수적입니다. 우주와 방위기술의 혁신이 가속화됨에 따라 높은 내열성과 기계적 탄력성을 갖춘 재료에 대한 수요가 급증하고 있습니다.

미국의 초고온 세라믹(UHTC) 시장은 2024년에 3억 4,860만 달러를 창출하였습니다. 군사력의 근대화와 우주 개발에 대한 적극적인 노력으로 초내구성 재료에 대한 의존도가 높아지고 있습니다.

세계의 초고온 세라믹(UTHC) 시장에 공헌하고 있는 주요 기업으로는 Rolls-Royce, Precision Ceramics, Lockheed Martin, Saint-Gobain, Lockheed Martin Corporation 등이 있습니다. 이러한 산업 대기업은 보다 높은 파괴 인성, 보다 긴 내용 연수 등 강화된 특성을 가진 UHTC의 개발을 목표로, 연구 개발에 대한 적을 좁힌 투자를 통해 시장에서의 지위를 강화하고 있습니다. 시스템에의 통합을 가능하게 하고 있습니다.또한, 수요의 증대에 대응하기 위해, 기업은 생산 능력을 확대해, 선진적 제조 기술을 추구하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 산업 고찰

생태계 분석

공급자의 상황

이익률

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

산업에 미치는 영향요인

성장 촉진요인

산업의 잠재적 리스크?과제

시장 기회

성장 가능성 분석

규제 상황

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

Porter's Five Forces 분석

PESTEL 분석

가격 동향

지역별

제품별

장래 시장 동향

기술과 혁신의 상황

현재의 기술 동향

신흥기술

특허 상황

무역 통계(HS코드)(참고: 무역 통계는 주요 국가에서만 제공됨)

주요 수입국

주요 수출국

지속가능성과 환경 측면

지속 가능한 사례

폐기물 삭감 전략

생산에 있어서의 에너지 효율

친환경 활동

탄소 발자국의 고려

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

지역별

북미

유럽

아시아태평양

라틴아메리카 항공

중동 및 아프리카

기업 매트릭스 분석

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

합병과 인수

파트너십 및 협업

신제품 발매

확대 계획

제5장 시장 규모와 예측 : 재료별, 2021-2034년

주요 동향

붕소화물

이붕화 지르코늄(ZrB2)

이붕화 하프늄(HfB2)

이붕화 탄탈(TaB2)

이붕화 티타늄(TiB2)

기타 붕화물

탄화물

탄화지르코늄(ZrC)

하프늄 카바이드(HfC)

탄화탄탈(TaC)

탄화티탄(TiC)

탄화규소(SiC)

기타 탄화물

질화물

질화 하프늄(HfN)

질화지르코늄(ZrN)

질화탄탈(TaN)

실리콘 질화물(Si3N4)

기타 질화물

복합재료 시스템

붕화물계 복합재료

탄화물계 복합재료

질화물계 복합재료

기타

기타 재료 유형

제6장 시장 규모와 예측 : 제품형태별, 2021-2034년

주요 동향

분말

벌크 컴포넌트

모놀리식 컴포넌트

복합부품

코팅

차열 코팅

내산화 코팅

내식성 코팅

기타 코팅 유형

섬유와 휘스커

기타

제7장 시장 규모와 예측 : 제조방법별, 2021-2034년

주요 동향

핫 프레스

방전 플라즈마 소결(SPS)

반응성 핫 프레스

가압 소결

화학 증착(CVD)

적층 조형

기타 제조방법

제8장 시장 규모와 예측 : 용도별, 2021-2034년

주요 동향

열 보호 시스템

극초음속기의 앞 가장자리

재돌입기의 열 실드

로켓 노즐의 목구멍

연소실 라이너

기타

추진 시스템

로켓 엔진 부품

가스 터빈 부품

스크럼 제트의 컴포넌트

기타 추진 용도

고온 센서와 계측 기기

절삭 공구와 내마모 부품

노의 요소 도가니

원자력 용도

기타

제9장 시장 규모와 예측 : 최종용도산업별, 2021-2034년

주요 동향

항공우주 및 방위

군사항공우주

민간항공우주

우주 탐사

미사일 시스템

기타

산업

금속가공

유리 제조

화학처리

기타 산업용도

에너지

원자력 에너지

화석연료발전

기타 에너지 용도

일렉트로닉스 및 반도체

연구와 학술

기타

제10장 시장 규모와 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

기타 유럽

아시아태평양

중국

인도

일본

한국

호주

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

기타 중동 및 아프리카

제11장 기업 프로파일

Lockheed Martin Corporation

Rolls-Royce

Ultramet

BAE Systems

3M Company

CoorsTek

Morgan Advanced Materials

Kennametal

Aremco Products

Advanced Ceramics Manufacturing

Precision Ceramics USA

Kyocera Corporation

Saint-Gobain

SHW

영문 목차

영문목차

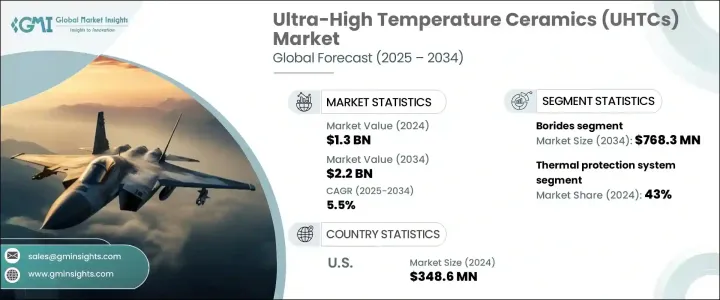

The Global Ultra-High Temperature Ceramics Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 2.2 billion by 2034. Growth in this sector is largely driven by technological advancements in defense, aerospace, automotive, and energy, which increasingly require materials capable of operating under extreme thermal and mechanical conditions. UHTCs are engineered to withstand temperatures exceeding 3000°C, making them essential in environments where conventional materials fail. These ceramics are now playing a pivotal role in enhancing energy efficiency and meeting sustainability goals in high-heat systems. Their use is expanding in advanced propulsion, high-speed flight systems, and next-gen thermal protection applications.

As industries shift towards performance-focused and emission-reducing innovations, demand for UHTCs continues to climb. Their importance is magnified in high-performance sectors pushing technological boundaries and requiring unmatched durability. In addition, evolving global military strategies and a greater focus on space exploration are accelerating the need for thermally resilient materials. With escalating investments across industrial verticals, particularly in the US, UHTCs are becoming indispensable in applications that demand resistance to oxidation, thermal shock, and mechanical stress.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$1.3 Billion

Forecast Value

$2.2 Billion

CAGR

5.5%

The Borides segment generated USD 456.1 million in 2024 and is expected to grow to USD 768.3 million by 2034. This category remains dominant due to its superior thermal conductivity, exceptional oxidation resistance, and ultra-high melting points, making it ideal for applications that demand the highest levels of performance. Among UHTCs, borides are specifically valued in extreme environments due to their capacity to endure mechanical loads and temperatures well beyond what standard ceramics can tolerate. These attributes make them the preferred material class in propulsion systems and thermal barriers where reliability is critical.

The thermal protection systems segment accounted for 43% share, remaining the leading application segment. The increasing need for materials that can maintain structural and thermal integrity in extremely harsh environments, such as during hypersonic travel or space-bound missions, is fueling demand for UHTCs in this segment. Their ability to perform under sustained aerodynamic stress, intense frictional heat, and rapid atmospheric transitions makes them indispensable for systems requiring absolute thermal control. As innovation accelerates in space and defense technologies, demand for materials with high heat tolerance and mechanical resilience is surging.

United States Ultra-High Temperature Ceramics (UHTCs) Market generated USD 348.6 million in 2024. This strong presence is driven by significant investments in advanced defense systems, space technology, and energy applications that rely heavily on materials capable of performing at elevated temperatures. The country's aggressive push to modernize military capabilities and space initiatives is increasing reliance on ultra-durable materials. Given the rising focus on next-generation propulsion and national defense strategies, the market for UHTCs in the US is expected to maintain steady momentum.

Key companies contributing to the Global Ultra-High Temperature Ceramics (UTHCs) Market include Rolls-Royce, Precision Ceramics, Lockheed Martin Corporation, Saint-Gobain, and Advanced Ceramics Manufacturing. These industry leaders are strengthening their market positions through targeted investments in R&D, aiming to develop UHTCs with enhanced properties such as higher fracture toughness and longer service life. Strategic collaborations with aerospace and defense organizations allow for customized material development and integration into critical systems. Firms are also scaling production capacities and pursuing advanced manufacturing techniques to meet growing demand. By diversifying applications and ensuring stringent quality control, these companies are positioning themselves for long-term leadership in this evolving field.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis

2.2 Key market trends

2.2.1 Regional

2.2.2 Material type

2.2.3 Product form

2.2.4 Manufacturing method

2.2.5 Application

2.2.6 End use Industry

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier Landscape

3.1.2 Profit Margin

3.1.3 Value addition at each stage

3.1.4 Factor affecting the value chain

3.1.5 Disruptions

3.2 Industry impact forces

3.2.1 Growth drivers

3.2.2 Industry pitfalls and challenges

3.2.3 Market opportunities

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 North America

3.4.2 Europe

3.4.3 Asia Pacific

3.4.4 Latin America

3.4.5 Middle East & Africa

3.5 Porter's analysis

3.6 PESTEL analysis

3.6.1 Technology and Innovation landscape

3.6.2 Current technological trends

3.6.3 Emerging technologies

3.7 Price trends

3.7.1 By region

3.7.2 By product

3.8 Future market trends

3.9 Technology and Innovation landscape

3.9.1 Current technological trends

3.9.2 Emerging technologies

3.10 Patent Landscape

3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only

3.11.1 Major importing countries

3.11.2 Major exporting countries

3.12 Sustainability and environmental aspects

3.12.1 Sustainable practices

3.12.2 Waste reduction strategies

3.12.3 Energy efficiency in production

3.12.4 Eco-friendly initiatives

3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.2.1 By region

4.2.1.1 North America

4.2.1.2 Europe

4.2.1.3 Asia Pacific

4.2.1.4 LATAM

4.2.1.5 MEA

4.3 Company matrix analysis

4.4 Competitive analysis of major market players

4.5 Competitive positioning matrix

4.6 Key developments

4.6.1 Mergers & acquisitions

4.6.2 Partnerships & collaborations

4.6.3 New Product Launches

4.6.4 Expansion Plans

Chapter 5 Market Size and Forecast, By Material Type, 2021-2034 (USD Billion) (Tons)

5.1 Key trends

5.2 Borides

5.2.1 Zirconium diboride (ZrB?)

5.2.2 Hafnium diboride (HfB?)

5.2.3 Tantalum diboride (TaB?)

5.2.4 Titanium diboride (TiB?)

5.2.5 Other borides

5.3 Carbides

5.3.1 Zirconium carbide (ZrC)

5.3.2 Hafnium carbide (HfC)

5.3.3 Tantalum carbide (TaC)

5.3.4 Titanium carbide (TiC)

5.3.5 Silicon carbide (SiC)

5.3.6 Other carbides

5.4 Nitrides

5.4.1 Hafnium nitride (HfN)

5.4.2 Zirconium nitride (ZrN)

5.4.3 Tantalum nitride (TaN)

5.4.4 Silicon nitride (Si?N?)

5.4.5 Other nitrides

5.5 Composite systems

5.5.1 Boride-based composites

5.5.2 Carbide-based composites

5.5.3 Nitride-based composites

5.5.4 Other composite systems

5.6 Other material types

Chapter 6 Market Size and Forecast, By Product Form, 2021-2034 (USD Billion) (Tons)

6.1 Key trends

6.2 Powders

6.3 Bulk components

6.3.1 Monolithic components

6.3.2 Composite components

6.4 Coatings

6.4.1 Thermal barrier coatings

6.4.2 Oxidation-resistant coatings

6.4.3 Erosion-resistant coatings

6.4.4 Other coating types

6.5 Fibers & whiskers

6.6 Other product forms

Chapter 7 Market Size and Forecast, By Manufacturing Method, 2021-2034 (USD Billion) (Tons)

7.1 Key trends

7.2 Hot pressing

7.3 Spark plasma sintering (SPS)

7.4 Reactive hot pressing

7.5 Pressureless sintering

7.6 Chemical vapor deposition (CVD)

7.7 Additive manufacturing

7.8 Other manufacturing methods

Chapter 8 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Tons)

8.1 Key trends

8.2 Thermal protection systems

8.2.1 Hypersonic vehicle leading edges

8.2.2 Reentry vehicle heat shields

8.2.3 Rocket nozzle throats

8.2.4 Combustion chamber liners

8.2.5 Other thermal protection applications

8.3 Propulsion systems

8.3.1 Rocket engine components

8.3.2 Gas turbine components

8.3.3 Scramjet components

8.3.4 Other propulsion applications

8.4 High-temperature sensors & instrumentation

8.5 Cutting tools & wear-resistant components

8.6 Furnace elements & crucibles

8.7 Nuclear applications

8.8 Other applications

Chapter 9 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Tons)

9.1 Key trends

9.2 Aerospace & defense

9.2.1 Military aerospace

9.2.2 Civil aerospace

9.2.3 Space exploration

9.2.4 Missile systems

9.2.5 Other aerospace & defense applications

9.3 Industrial

9.3.1 Metal processing

9.3.2 Glass manufacturing

9.3.3 Chemical processing

9.3.4 Other industrial applications

9.4 Energy

9.4.1 Nuclear energy

9.4.2 Fossil fuel power generation

9.4.3 Other energy applications

9.5 Electronics & semiconductor

9.6 Research & academia

9.7 Other end use industries

Chapter 10 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Tons)