백색 시멘트 시장 : 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)

White Cement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1755357

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

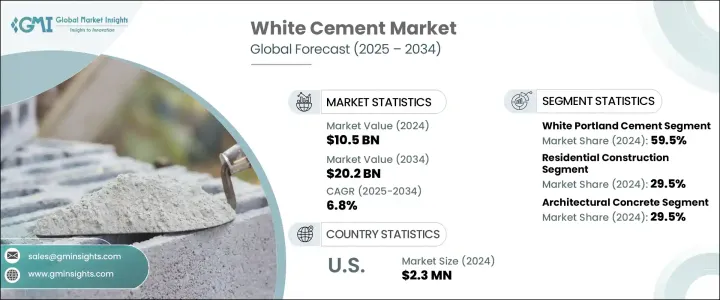

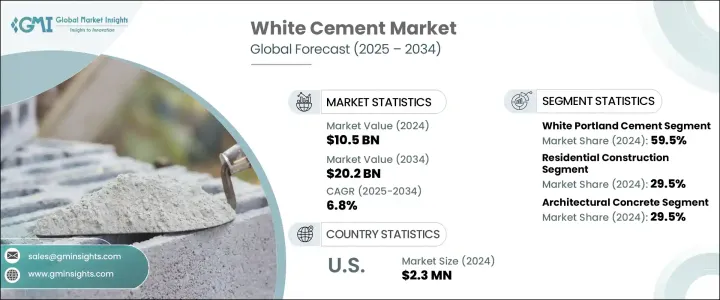

세계의 백색 시멘트 시장 규모는 2024년에 105억 달러로 평가되었고, 세계의 인프라 개척의 급증에 의해 CAGR 6.8%로 성장하여 2034년에는 202억 달러에 이를 것으로 예측되고 있습니다.

도시화가 급속히 진행되고 있는 가운데, 각 국 정부는 도로, 교량, 공공 건축물의 건설에 많은 투자를 실시하고 있어, 백색 시멘트와 같은 고품질로 외형도 아름다운 건축재료에 대한 수요가 높아지고 있습니다.

지속가능성은 백색 시멘트 시장을 발전시키는 또 다른 중요한 요인이 되고 있습니다. 건축가와 건설업자가 이산화탄소 배출량을 삭감하고자 하는 가운데 백색 시멘트는 에너지 절약과 환경 유지에 공헌하기 때문에 건설 업계에서 선호되는 재료로 자리매김하고 있습니다. 시장의 변화하는 요구에 대응하여 제조업체들은 향상된 강도와 빠른 설정 시간과 같은 향상된 성능 특성을 제공하는 새로운 백 시멘트 제형을 도입하고 있습니다. 실행 가능하고 비용 효율적인 것으로, 도시의 성장 기회가 계속되고, 건설 동향이 진화함에 따라, 이 시장은 그 기세를 유지해, 건축 재료 분야의 기존 기업이나 신규 참가 기업에 큰 기회를 제공할 것으로 예측됩니다.

시장 범위

시작 연도

2024년

예측 기간

2025-2034년

초기 시장 규모

105억 달러

시장 규모 예측

202억 달러

CAGR

6.8%

2024년에는 백색 포틀랜드 시멘트가 59.5%의 점유율을 차지했습니다. 백색 포틀랜드 시멘트는 높은 강도, 우수한 마무리, 미관으로 가장 널리 사용됩니다. 백색 포틀랜드 시멘트는 벽, 바닥, 조각 등 색상과 밝기의 균일성이 중요한 건축 및 장식용으로 주로 사용됩니다. 이 분야 수요는 고급 건축 프로젝트의 개발이 진행되어, 주택이나 상업 공간에서 시각에 호소하는 구조를 선호하는 경향이 강해지고 있는 것이 큰 요인이 되고 있습니다.

2024년 주택 건설 분야 시장 점유율은 29.5%였습니다. 백색 시멘트는 탁월한 마무리, 내구성 및 미적 가치로 주택 건설에 매우 선호되며 내부 및 외부 벽, 바닥재 및 장식 요소에 인기있는 옵션이 되었습니다. 도시화와 인구 증가에 힘입어 주택 수요 증가가 이 분야의 성장에 중요한 요소가 되고 있습니다. 주택 소유자가 우아하고 오래 지속되는 소재를 찾는 동안 백색 시멘트는 고급스럽고 오래 지속되는 주택 공간을 만들기 위한 선호 옵션입니다.

미국의 백색 시멘트 시장은 2024년에 230만 달러로 85%의 점유율을 차지했습니다. 이 나라는 건설 활동의 확대, 기술 발전, 지속 가능한 건축 관행에 대한 강력한 집중으로 인해 백색 시멘트 소비가 급격히 증가할 것으로 예상됩니다.

JK 시멘트, Aalborg Portland, UltraTech Cement, Cemex, Cimsa 등 주요 기업들은 이러한 전략을 활용하여 백색 시멘트 수요 증가에 대응하고, 경쟁이 치열한 시장에서 우위를 차지하고자 합니다. 고강도 배합, 미관 마무리, 지속가능성 등, 특정의 요구에 대응하는 특수한 백색 시멘트를 개발하는 것으로, 각 사는 주택과 상업의 양부문으로부터의 높아지는 수요에 확실히 대응하고 있습니다. 생산 효율과 품질을 향상시키는 최첨단 기술에 대한 투자도 또한 중요한 전략입니다.

목차

제1장 분석 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

제조 공정 분석

원재료 분석 및 조달 전략

백색 시멘트와 회색 시멘트의 비교 분석

이익률 분석

밸류체인 분석

트럼프 정권의 관세 영향: 구조화된 개요

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS 코드) 참고: 위의 무역 통계는 주요 국가에 대해서만 제공됩니다

주요 수출국

주요 수입국

이익률 분석

주요 뉴스와 대처

기술의 정세

전통적인 제조 기술

첨단 제조 기술

신흥기술

특허 분석

규제 상황

시장 역학

시장 성장 촉진요인

미관건축자재 수요 증가

도시화와 인프라 정비의 개발

건축 용도에서의 채용 증가

프리캐스트·프리팹 건설의 성장

시장 성장 억제요인

회색 시멘트에 비해 높은 생산 비용

환경 문제와 탄소 배출

원재료 가격 변동

고품질 원재료의 입수에의 제약

시장 기회

생산 공정에 있어서의 기술의 진보

신흥국 수요 증가

친환경 백색 시멘트 변종 개발

응용 분야의 확대

시장의 과제

엄격한 환경 규제

생산에 있어서의 높은 에너지 소비

운송 및 물류의 과제

대체 재료와의 경쟁

규제 틀 분석

국제규격(ASTM C989/C989 M, EN 197-1)

지역의 규제와 기준

환경 컴플라이언스 요건

품질인증시스템

기술 상황

현재의 기술 동향

슬래그 시멘트 제조에 있어서의 신기술

디지털화와 인더스트리 4.0의 영향

연구개발 이니셔티브와 혁신·파이프라인

가격 분석

가격 동향 분석

비용 구조 분석

가격에 영향을 미치는 요인

지역별 가격 차이

PESTEL 분석

Porter's Five Forces 분석

규제 틀과 정부의 대처

COVID-19의 영향 백색 시멘트 시장

러시아와 우크라이나 분쟁이 공급망에 미치는 영향

신규 참가자 시장 진출 전략

가격 분석과 동향

무역 분석 : 수출입 시나리오

제4장 경쟁 구도

시장 점유율 분석

전략적 대시보드

주요 이해관계자와 시장 포지셔닝

경쟁 벤치마킹

경쟁 포지셔닝 매트릭스

경쟁 전략

신제품 개발

기업 합병·인수(M&A)

사업 제휴 및 협력

생산 능력 확장

주요 기업의 SWOT 분석

경쟁의 치열 : Porter's Five Forces 분석

제5장 시장 추정 및 예측 : 제품 유형별(2021-2034년)

주요 동향

백색 포틀랜드 시멘트

석공용 백색 시멘트

백색 포틀랜드 석회석 시멘트(PLC)

기타(백색 알루민산칼슘 시멘트 등)

제6장 시장 추정 및 예측 : 그레이드별(2021-2034년)

주요 동향

유형 52.5

유형 42.5

유형 32.5

기타

제7장 시장 추정 및 예측 : 용도별(2021-2034년)

주요 동향

주택건설

상업건설

인프라 개발

장식용도

제8장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

주요 동향

건축용 콘크리트

프리캐스트 제품

인조 대리석 바닥

수영장

싱크대와 장식 요소

기타

제9장 시장 추정 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

기타 유럽

아시아태평양

중국

인도

일본

호주

한국

기타 아시아태평양

라틴아메리카

브라질

멕시코

아르헨티나

기타 라틴아메리카

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

기타 중동?아프리카

제10장 기업 프로파일

Aalborg Portland A/S

Adana Cimento Sanayii TAS

Aditya Birla Group(UltraTech Cement Ltd.-Birla White)

Cementir Holding NV

Cemex SAB de CV

Cimsa Cimento Sanayi ve Ticaret AS.

Federal White Cement Ltd.

Holcim Group

JK Cement Ltd.

Lehigh White Cement Company

OYAK Cement

Ras Al Khaimah Cement Company(RAKCC)

Royal White Cement Inc.

Saveh White Cement Co.

Shargh White Cement Co.

SHW

영문 목차

영문목차

The Global White Cement Market was valued at USD 10.5 billion in 2024 and is estimated to grow at 6.8% CAGR to reach USD 20.2 billion by 2034, driven by the surge in global infrastructure development. With urbanization progressing rapidly, governments are investing significantly in constructing roads, bridges, and public buildings, increasing the demand for high-quality, visually appealing building materials such as white cement.

Sustainability has become another key factor propelling the white cement market forward. Its heat-reflective properties make it an excellent choice for energy-efficient construction, aligning with the increasing demand for eco-friendly building materials. As architects and builders seek to reduce carbon footprints in their designs, white cement's benefits in contributing to energy savings and environmental sustainability have positioned it as a preferred material in the construction industry. In response to evolving market needs, manufacturers are introducing new formulations of white cement that offer enhanced performance characteristics, such as improved strength and faster setting times. These innovations are expanding the scope of white cement applications, making them more viable and cost-effective for large-scale construction projects. As urban growth continues and construction trends evolve, the market is expected to maintain its positive momentum, offering significant opportunities for established companies and new entrants in the building materials sector.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$10.5 Billion

Forecast Value

$20.2 Billion

CAGR

6.8%

In 2024, white Portland cement represented a 59.5% share. This segment is the most widely used due to its high strength, superior finish, and aesthetic appeal. It is predominantly employed in architectural and decorative applications, such as walls, flooring, and sculptures, where uniformity in color and brightness is essential. The demand for this segment is largely driven by the growing development of premium construction projects and an increasing preference for visually appealing structures in residential and commercial spaces.

The residential construction sector held a market share of 29.5% in 2024. White cement is highly favored in residential construction due to its exceptional finishing, durability, and aesthetic value, making it a popular choice for interior and exterior walls, flooring, and decorative elements. The rise in housing demand, fueled by urbanization and population growth, has been a key factor in the sector's growth. As homeowners seek materials that offer elegance and longevity, white cement has become a preferred option for creating high-end, lasting residential spaces.

U.S. White Cement Market held an 85% share valued at USD 2.3 million in 2024. The country is set to experience rapid growth in white cement consumption, driven by an expansion in construction activities, technological advancements, and a strong focus on sustainable building practices. The high demand for durable and aesthetically pleasing building materials, combined with a surge in infrastructure development, is significantly boosting the consumption of white cement in the U.S.

Key players such as J.K. Cement, Aalborg Portland, UltraTech Cement, Cemex, and Cimsa are capitalizing on these strategies to meet the growing demand for white cement and stay ahead in the highly competitive market. Companies in the white cement market have implemented several key strategies to bolster their presence and strengthen their market position. These include focusing on product innovation, expanding production capacities, and building strategic partnerships. By developing specialized white cement variants that cater to specific needs like high-strength formulations, aesthetic finishes, or sustainability, companies ensure they meet the growing demand from both residential and commercial sectors. Investment in cutting-edge technologies that improve production efficiency and quality is also a crucial strategy. This allows companies to meet the rising demand while ensuring superior product consistency.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research Methodology

1.2 Research Objectives

1.3 Market Definition and Scope

1.4 Market Segmentation

1.5 Data Sources

1.5.1 Primary Research

1.5.2 Secondary Research

1.6 Market Estimation Approach

1.7 Research Assumptions and Limitations

1.8 Base Year and Forecast Period

Chapter 2 Executive Summary

2.1 Market Snapshot

2.2 Global White Cement Market Highlights

2.3 Regional Market Highlights

2.4 Segmental Market Highlights

2.5 Competitive Landscape Snapshot

2.6 Investment Highlights and Strategic Recommendations

2.7 Key Market Trends and Future Growth Indicators

2.8 Analyst Perspective and Critical Insights

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Manufacturing process analysis

3.1.2 Raw material analysis and sourcing strategies

3.1.3 White cement vs. gray cement: comparative analysis

3.1.4 Profit margin analysis

3.1.5 Value chain analysis

3.2 Impact of trump administration tariffs - structured overview

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1 Supply-side impact (raw materials)

3.2.2.2 Price volatility in key materials

3.2.2.3 Supply chain restructuring

3.2.2.4 Production cost implications

3.2.2.2 Demand-side impact (selling price)

3.2.2.2.1 Price transmission to end markets

3.2.2.2.2 Market share dynamics

3.2.2.2.3 Consumer response patterns

3.2.3 Key companies impacted

3.2.4 Strategic industry responses

3.2.4.1 Supply chain reconfiguration

3.2.4.2 Pricing and product strategies

3.2.4.3 Policy engagement

3.2.5 Outlook and future considerations

3.3 Trade statistics (HS code) Note: the above trade statistics will be provided for key countries only.

3.3.1 Major exporting countries

3.3.2 Major importing countries

3.4 Profit margin analysis

3.5 Key news & initiatives

3.5.1 Technology landscape

3.5.2 Traditional manufacturing technologies

3.5.3 Advanced manufacturing technologies

3.5.4 Emerging technologies

3.5.5 Patent analysis

3.6 Regulatory landscape

3.6.1 North America

3.6.2 Europe

3.6.3 Asia Pacific

3.6.4 Latin America

3.6.5 MEA

3.7 Market dynamics

3.7.1 Market drivers

3.7.1.1 Growing demand for aesthetic construction materials

3.7.1.2 Increasing urbanization and infrastructure development

3.7.1.3 Rising adoption in architectural applications

3.7.1.4 Growth in precast and prefabricated construction

3.7.2 Market Restraints

3.7.2.1 Higher production costs compared to gray cement

3.7.2.2 Environmental concerns and carbon emissions

3.7.2.3 Raw material price volatility

3.7.2.4 Limited availability of high-quality raw materials

3.7.3 Market Opportunities

3.7.3.1 Technological advancements in production processes

3.7.3.2 Growing demand in emerging economies

3.7.3.3 Development of eco-friendly white cement variants

3.7.3.4 Expansion of application areas

3.7.4 Market Challenges

3.7.4.1 Stringent Environmental Regulations

3.7.4.2 High energy consumption in production

3.7.4.3 Transportation and logistics challenges

3.7.4.4 Competition from alternative materials

3.7.5 Regulatory Framework Analysis

3.7.5.1. International standards (ASTM C989/C989 M, EN 197-1)

3.7.5.2 Regional regulations and standards

3.7.5.3 Environmental compliance requirements

3.7.5.4 Quality certification systems

3.7.6 Technology Landscape

3.7.6.1 Current technological trends

3.7.6.2 Emerging technologies in slag cement production

3.7.6.3 Digitalization and industry 4.0 impact

3.7.6.4 R&d initiatives and innovation pipeline

3.7.7 Pricing Analysis

3.7.7.1 Price trend analysis

3.7.7.2 Cost structure analysis

3.7.7.3 Factors affecting pricing

3.7.7.4 Regional price variations

3.8 PESTLE Analysis

3.9 Porter's five forces analysis

3.10 Regulatory framework and government initiatives

3.11 Impact of covid-19 on white cement market

3.12 Impact of Russia Ukraine conflict on supply chain

3.13 Market entry strategies for new players

3.14 Pricing analysis and trends

3.15 Trade analysis: import-export scenario

Chapter 4 Competitive Landscape, 2024

4.1 Market share analysis, 2024

4.2 Strategic dashboard

4.3 Key stakeholders and market positioning

4.4 Competitive benchmarking

4.5 Competitive positioning matrix

4.6 Competitive strategies

4.6.1 new product developments

4.6.2 mergers and acquisitions

4.6.3 partnerships and collaborations

4.6.4 capacity expansions

4.7 SWOT analysis of key players

4.8 competitive intensity - Porter's five forces analysis

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

5.1 Key trends

5.2 White Portland Cement

5.3 White Masonry Cement

5.4 White Portland Limestone Cement (PLC)

5.5 Others (White Calcium Aluminate Cement, etc.)

Chapter 6 Market Estimates and Forecast, By Grade, 2021 - 2034 (USD Billion) (Kilo Tons)

6.1 Key trends

6.2 Type 52.5

6.3 Type 42.5

6.4 Type 32.5

6.5 Others

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

7.1 Key trends

7.2 Residential Construction

7.3 Commercial Construction

7.4 Infrastructure Development

7.5 Decorative Applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

8.1 Key trends

8.2 Architectural Concrete

8.3 Precast Products

8.4 Terrazzo Flooring

8.5 Swimming Pools

8.6 Countertops and Decorative Elements

8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

9.1 Key trends

9.2 North America

9.2.1 U.S.

9.2.2 Canada

9.3 Europe

9.3.1 Germany

9.3.2 UK

9.3.3 France

9.3.4 Spain

9.3.5 Italy

9.3.6 Rest of Europe

9.4 Asia Pacific

9.4.1 China

9.4.2 India

9.4.3 Japan

9.4.4 Australia

9.4.5 South Korea

9.4.6 Rest of Asia Pacific

9.5 Latin America

9.5.1 Brazil

9.5.2 Mexico

9.5.3 Argentina

9.5.4 Rest of Latin America

9.6 Middle East and Africa

9.6.1 Saudi Arabia

9.6.2 South Africa

9.6.3 UAE

9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

10.1 Aalborg Portland A/S

10.2 Adana Cimento Sanayii T.A.S.

10.3 Aditya Birla Group (UltraTech Cement Ltd. - Birla White)