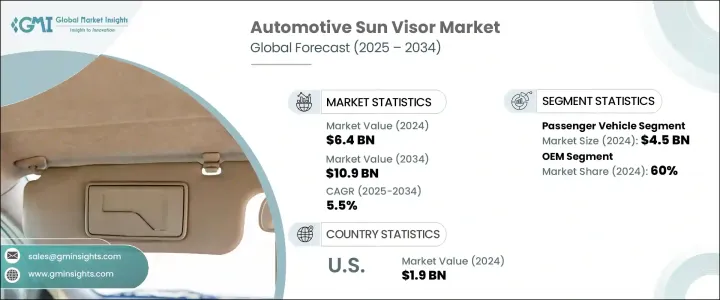

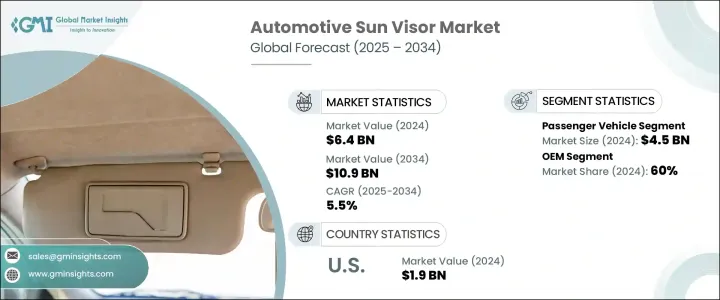

세계의 자동차 선바이저 시장 규모는 2024년에는 64억 달러로 평가되었고, 2034년에는 109억 달러에 이를 것으로 예측되며, CAGR 5.5%로 성장할 전망입니다.

이러한 성장은 전 세계적으로 자동차 생산량이 증가하고 있으며, 소비자들이 차량 내의 편안함과 도로 안전에 대한 기대가 높아지고 있기 때문에 촉진되고 있습니다. 자동차 제조사들이 특히 빠르게 성장하는 경제권에서 생산량을 확대함에 따라 선바이저와 같은 주요 내장 부품에 대한 수요가 지속적으로 증가하고 있습니다. 소비자들은 기본적인 그늘 제공을 넘어 통합 조명, 터치 컨트롤, 눈부심 감소 기술 등을 갖춘 고급 선바이저 시스템을 요구하고 있습니다. 이러한 업그레이드는 스타일과 기능을 모두 갖춘 내장 공간에 대한 수요 증가에 부응하며, 편안함과 가시성을 우선시하는 트렌드를 반영합니다. 또한 규제 기관과 안전 기준은 제조사가 상업용 및 승용차 모두에 향상된 선바이저 기능을 표준 사양으로 포함하도록 촉진하고 있습니다.

도로 안전에 대한 요구가 증가하는 것도 수요를 촉진하는 중요한 요인이 되고 있습니다. 선바이저는 운전자의 시야를 개선하고 눈부심으로 인한 사고를 예방하여 전 세계적으로 교통 사고를 줄이기 위한 노력에 부합합니다. 전기자동차는 현대적인 인테리어에 정교하고 맞춤화할 수 있는 선바이저 시스템이 필요하기 때문에 시장 성장에 더욱 기여하고 있습니다. 전기자동차 제조업체들은 고급스러운 실내 디자인에 완벽하게 어울리는 고품질의 첨단 선바이저를 선호하여 이 부문의 혁신을 촉진하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 64억 달러 |

| 예측 금액 | 109억 달러 |

| CAGR | 5.5% |

승용차는 2024년에 45억 달러의 시장 가치를 차지하며, 대량 생산과 일상적인 사용으로 전체 부문을 주도했습니다. 이러한 차량은 여러 지역에서 개인 이동 수단의 중심을 차지하고 있으며, 이는 선바이저와 같은 편안함을 향상시키는 인테리어 부품에 대한 지속적인 수요를 촉진하고 있습니다. 자동차 제조업체들이 미관 및 안전 개선에 지속적으로 투자함에 따라, 선바이저에는 조명 거울, 확장 플랩 및 스마트 기능이 장착되어 운전 경험을 향상시키고 있습니다. 엔트리급 모델에서 고급 세단에 이르기까지 다양한 차량에 제공되는 선바이저는 다양한 요구와 선호도에 맞는 다양한 솔루션을 보장합니다.

OEM 부문은 2024년에 60%의 점유율을 차지하며, 선바이저가 차량에 통합되는 방식에서 지배적인 역할을 유지하고 있습니다. 이러한 제조업체들은 엄격한 성능 및 안전 기준을 충족하기 위해 생산 단계에서 선바이저를 조달합니다. 맞춤형 공장 장착 부품을 공급할 수 있는 능력은 비용 효율적이고 원활한 선바이저 솔루션을 제공하는 데 경쟁 우위를 제공합니다. 자동차 제조사와 Tier 1 공급업체 간의 협력이 강화되면서, 조명 기능이 탑재된 화장 거울이나 브랜드 정체성과 소비자 기대를 반영하는 고급 소재를 적용한 혁신적인 제품이 등장하고 있습니다.

북미의 자동차 선바이저 시장은 2024년 19억 달러를 기록했으며, 2034년까지 연평균 성장률(CAGR) 5.8%로 성장할 것으로 예상됩니다. 미국 시장은 강력한 안전 규제와 기술 통합 차량 인테리어에 대한 수요 증가의 혜택을 계속 누리고 있습니다. 제조업체들은 실용성과 미학을 겸비한 다기능 선바이저로 전환하고 있습니다. 고급차 및 전기자동차 판매의 급증은 진화하는 프리미엄 운전 환경의 개념을 지원하는 고급 선바이저 디자인에 대한 수요를 촉진하고 있습니다. 현대적인 소재, 디지털 인터페이스 및 세련된 스타일을 통합하여 선바이저는 차량의 실내 경험에 필수적인 부품으로 변모하고 있습니다.

자동차 선바이저 시장을 형성하는 주요 기업은 Visteon, Tachi-S, Grupo Antolin, Continental, Setrag, IAC, Shiroki, Kasai Kogyo, Howa Textile, and Adient. 등이 있습니다. 이들 기업은 진화하는 소비자 요구를 충족시키기 위해 전략적 제품 혁신에 투자하고 있습니다. 많은 기업은 차량 전체 무게를 줄이면서 내구성을 유지하는 경량화 및 모듈식 디자인 개발에 집중하고 있습니다. 반사 방지 필름과 스마트 미러 솔루션 등 고급 소재 통합 기술이 성능 개선을 위해 적용되고 있습니다. 기업들은 자동차 제조사와의 협력을 강화해 브랜드 아이덴티티와 인체공학에 맞는 OEM 맞춤형 디자인을 제공하기 위해 노력하고 있습니다. 제조 기반을 확장하는 것, 특히 비용 효율적인 지역에서의 투자 확대, 제품 포트폴리오 다각화는 경쟁력 강화와 시장 확대를 위한 핵심 전략으로 남아 있습니다.

The Global Automotive Sun Visor Market was valued at USD 6.4 billion in 2024 and is estimated to grow at a CAGR of 5.5% to reach USD 10.9 billion by 2034. The growth is driven by the increasing vehicle production worldwide, along with rising consumer expectations for better in-cabin comfort and road safety, is driving this expansion. As automakers scale output-especially in fast-developing economies-the demand for key interior components like sun visors continues to rise. Consumers seek advanced sun visor systems beyond basic shading and incorporate features like integrated lighting, touch controls, and glare-reducing technology. These upgrades cater to the growing desire for stylish yet functional interiors that prioritize comfort and visibility. Additionally, regulatory bodies and safety standards are prompting manufacturers to include enhanced visor features as part of standard offerings in both commercial and passenger vehicles.

The growing need for road safety also plays a critical role in boosting demand. Sun visors improve driver visibility and help prevent glare-related incidents, aligning with global initiatives to reduce traffic accidents. Electric vehicles contribute further to the market's growth, as their modern interiors often call for sophisticated, customizable visor systems. EV manufacturers prefer high-quality, tech-enhanced visors that blend seamlessly into their advanced cabin designs fueling innovation across the segment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.4 Billion |

| Forecast Value | $10.9 Billion |

| CAGR | 5.5% |

Passenger vehicles accounted for a market value of USD 4.5 billion in 2024, leading the overall segment due to their large production volumes and everyday usage. These vehicles are central to personal mobility across regions, which fuels consistent demand for comfort-enhancing interior parts like sun visors. As automakers continue investing in aesthetic and safety improvements, sun visors are equipped with illuminated mirrors, extension flaps, and smart functionality to elevate the driving experience. From entry-level models to high-end sedans, the broad spectrum of vehicle offerings ensures a diverse range of visor solutions tailored to varying needs and preferences.

OEMs segment represented a 60% share in 2024, maintaining a dominant role in how sun visors are integrated into vehicles. These manufacturers source visors during the production stage to meet strict performance and safety criteria. Their ability to provide tailored, factory-fitted components gives them a competitive edge in delivering cost-effective and seamless visor solutions. Collaborations between automakers and Tier 1 suppliers have also intensified, allowing for innovative products with added features like lighted vanity mirrors and advanced materials that reflect brand identity and consumer expectations.

North America Automotive Sun Visor Market held USD 1.9 billion in 2024 and is set to grow at a CAGR of 5.8% through 2034. The American market continues to benefit from strong safety regulations and increasing demand for tech-integrated vehicle interiors. Manufacturers are shifting toward multi-functional sun visors that blend utility with aesthetics. A surge in luxury and electric vehicle sales drives the need for high-end sun visor designs that support the evolving concept of premium driving environments. Integrating modern materials, digital interfaces, and sleek styling transforms sun visors into essential components of the vehicle's cabin experience.

Leading players shaping the Automotive Sun Visor Market include Visteon, Tachi-S, Grupo Antolin, Continental, Setrag, IAC, Shiroki, Kasai Kogyo, Howa Textile, and Adient. These companies are investing in strategic product innovations to meet evolving consumer demands. Many focus on developing lightweight and modular designs that reduce overall vehicle weight while maintaining durability. Advanced material integration, such as anti-glare films and smart mirror solutions, is being used to improve performance. Firms are also strengthening collaborations with automakers to deliver OEM-specific designs that align with branding and ergonomics. Expanding manufacturing footprints, particularly in cost-effective regions, and diversifying product portfolios remain central strategies to enhance competitiveness and market reach.