Food Emulsifiers Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750581

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

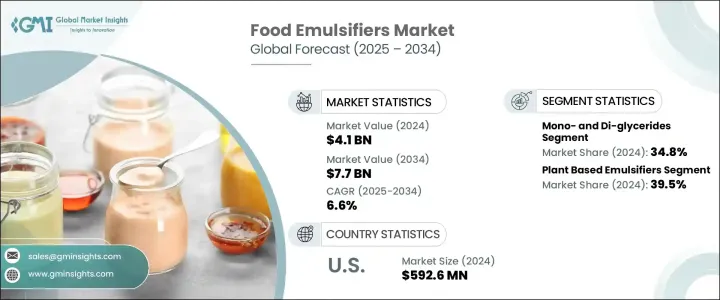

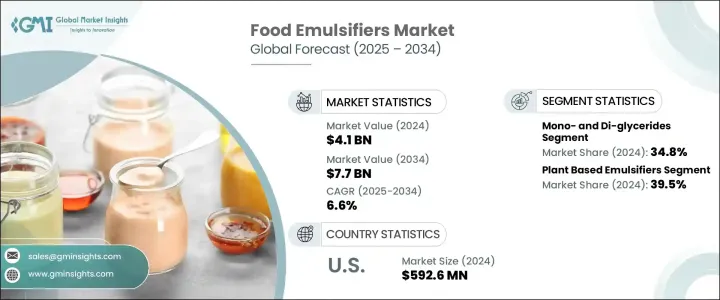

식품 유화제 시장은 2024년에는 41억 달러로 평가되었고 편의식품, 식물 유래 원료, 클린 라벨 제품에 대한 수요 증가에 견인되어 CAGR 6.6%를 나타내 2034년까지는 77억 달러에 이를 것으로 추정됩니다. 완료된 식품, 유아 영양 등 다양한 식품 분야에서 사용되고 있습니다. 또한, 모노글리세리드와 디글리세라이드 수요는 그 다용도성, 비용효과, 기능성 식품과 편의점에 있어서의 폭넓은 용도에 의해 계속 우위를 차지하고 있습니다.

지역별 성장이라는 점에서 식생활의 선호의 변화와 도시화의 진전에 의해 아시아태평양 시장이 급속히 확대되고 있습니다. 식품의 안전성과 라벨의 투명성에 대한 규제 당국의 지원의 고조도, 유화제 블렌드의 기술 혁신을 촉진해, 현대적인 식품 제조 공정에 있어서의 유화제의 존재감을 높여가고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

41억 달러

예측 금액

77억 달러

CAGR

6.6%

모노글리세리드·디글리세라이드 분야는 34.8%의 점유율을 차지하며, 2034년까지 연평균 복합 성장률(CAGR) 6.4%를 나타낼 것으로 예측됩니다. 긴 보존 기간과 일관성과 함께, 식품 업계에서 가장 사용되는 유화제의 하나로서의 지위를 확고한 것으로 하고 있습니다. 이렇게 널리 사용되고 있는 것과, 다기능성이 더해져, 모노글리세리드·디글리세라이드는 식품 제조에 있어서 지배적인 선택지로 계속하고 있습니다.

식물 유래의 유화제 부문은 2024년에 39.5%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 6.2%를 나타낼 것으로 예측됩니다. 제품을 요구하는 소비자가 늘어남에 따라, 대두, 해바라기, 카놀라 유래의 유화제 수요가 늘어나고 있습니다. 이러한 식물성 유화제는 영양학적 이점, 클린 라벨링, 지속 가능한 소싱으로 인해 인기를 얻고 있으며, 이는 모두 더 건강하고 환경 친화적인 식품 옵션에 대한 소비자 수요 증가와 맞물려 있습니다.

미국의 식품 유화제 강력한 식품 가공 산업과 편의점의 높은 소비로 2024년 시장 규모는 5억 9,260만 달러에 달했습니다. 건강과 웰니스의 경향이 높아지고 있는 것이 식물 유래나 천연의 대체품 등, 보다 혁신적인 유화제의 필요성을 높이고 있습니다.

Cargill, Inc. Corbion NV, Archer Daniels Midland Company(ADM), Kerry Group plc, Croda International Plc 등 세계의 식품 유화제 시장 주요 기업은 제품 포트폴리오의 다양화와 시장에서의 프레즌스 확대에 주력하고 있습니다. 또한, 효율 향상과 코스트 삭감을 위해서, 생산 공정의 강화도 진행하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

업계 생태계 분석

밸류체인에 영향을 주는 요인

이익률 분석

파괴적 혁신

향후 전망

제조업체

유통업체

트럼프 정권에 의한 관세에 대한 영향

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(판매가격)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

무역 통계(HS코드)

주요 수출국(2021-2024년)

주요 수입국(2021-2024년)

참고 : 위의 무역 통계는 주요 국가에 대해서만 제공됩니다.

소비자의 동향과 선호

클린 라벨 운동

유화제에 대한 소비자의 인식

천연과 합성의 취향

제품 처방에 미치는 영향

건강과 웰빙 동향

영양에 대한 우려

알레르기에 대한 고려 사항

식사 제한의 영향

지속가능성과 윤리적 배려

환경 영향 인식

지속 가능한 조달 우선

포장 고려 사항

식물 유래의 채식 동향

식물 유래 유화제 수요

채식 인증의 영향

투명성과 추적성 요구

지역에 의한 소비자의 선호의 차이

소비자 행동 분석

구매 결정 요인

가격 감도 분석

브랜드 충성도 패턴

소셜 미디어와 디지털이 소비자의 인식에 미치는 영향

공급망과 원재료 분석

원재료 조달 분석

주요 원재료

조달 지역

조달의 지속가능성

생산 공정 분석

제조 기술

품질관리조치

비용 구조 분석

유통 채널 분석

직접 채널과 간접 채널

전자상거래의 영향

유통의 과제

공급망의 과제

원재료 가격 변동

공급망의 혼란

물류의 과제

공급망 최적화 전략

지속 가능한 공급망의 실천

공급 체인의 기술 통합

가격 분석과 비용 구조

가격 분석 : 제품 유형별

가격 동향 분석(2021-2025년)

가격 예측(2025-2034년)

가격에 영향을 미치는 요인

원재료비

생산 비용

규제 준수 비용

시장 경쟁

지역별 가격 차이

주요 기업의 가격 전략

비용 구조 분석

원재료비

제조 비용

유통 비용

마케팅 및 판매 비용

수익성 분석 : 제품 부문별

기술의 진보와 혁신

최근 기술 개발

유화제 제조에 있어서의 신기술

효소 수식

마이크로 캡슐화

나노기술의 응용

클린 라벨의 혁신

천연 유화제의 대체품

효소 기반 솔루션

식물 유래의 혁신

지속가능한 생산기술

기능 개선

안정성 향상

텍스처 특성 개선

보존 기간 연장 솔루션

생산과 품질 관리에 있어서의 디지털 기술

특허 분석과 연구개발 동향

미래의 기술 로드맵

지속가능성과 환경에 미치는 영향

유화제의 환경 발자국

탄소 발자국 분석

물 사용량의 평가

폐기물의 발생과 관리

지속 가능한 조달 관행

팜유의 지속가능성 문제

대두 조달의 과제

대체 지속가능한 자원

생분해성과 생태독성 평가

순환형 경제의 접근

업계의 지속가능성에 대한 노력

지속가능성에 대한 규제압력

지속가능한 제품에 대한 소비자 수요

지속 가능한 관행의 비용 편익 분석

시장의 과제와 기회

주요 시장의 과제

건강에 대한 우려와 부정적인 인식

규제상의 장애물

원재료 가격 변동

클린 라벨 처방의 과제

시장 기회

식물 유래 유화제의 개발

신흥 시장 확대

기능성 식품의 응용

지속 가능한 유화제 솔루션

거시경제 요인의 영향

기술적 기회 평가

전략적 기회 매핑

미래 시장 전망과 예측

시장 예측 : 제품 유형별(2025-2030년)

시장 예측 : 용도별(2025-2030년)

시장 예측 : 지역별(2025-2030년)

신흥 시장 동향

향후 성장 촉진요인

시장 발전 시나리오

낙관적 시나리오

현실적 시나리오

비관적 시나리오

투자 기회 평가

미래경쟁 구도 예측

전략적 제안

시장 진출 전략

제품 개발 권장 사항

지역 확대의 기회

경쟁적 포지셔닝 전략

지속가능성 구현 로드맵

디지털 변혁 전략

규제 컴플라이언스 전략

마케팅 및 브랜딩 권장 사항

리스크 경감 전략

투자 우선순위화 프레임워크

공급자의 상황

이익률 분석

주요 뉴스와 대처

규제 상황

영향요인

성장 촉진요인

음료 업계의 성장이 제품 수요를 끌어올릴 가능성

가공 식품의 소비량 증가가 업계의 성장을 가속

유제품의 소비량 증가는 식품 유화제 업계의 성장을 가속할 가능성 증대

업계의 잠재적 리스크 및 과제

높아지는 건강에 대한 우려

제품의 클린 라벨 요건

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

서론

기업의 시장 점유율 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

제5장 시장 규모와 예측 : 유형별(2021-2034년)

주요 동향

모노 및 이-글리세리드

레시틴

소르비탄 에스테르

스테아로일 락틸레이트

폴리글리세롤 에스테르

폴리소르베이트

기타(DATEM, CSL 등)

제6장 시장 규모와 예측 : 원료별(2021-2034년)

주요 동향

식물 유래 유화제

대두 유래

해바라기 유래

팜 유래

기타 식물 공급원

동물성 유화제

합성 유화제

제7장 시장 규모와 예측 : 용도별(2021-2034년)

주요 동향

베이커리 및 제과

빵 및 롤

케이크 및 페이스트리

비스킷 및 쿠키

초콜릿 및 과자류

유제품 및 냉동 디저트

아이스크림 및 냉동 디저트

우유 및 크림 제품

치즈 제품

요구르트 및 발효유 제품

가공 육류 및 해산물

소시지 및 가공육

해산물 제품

인스턴트 식품 및 즉석 식품

수프 및 소스

드레싱 마요네즈

바로 먹을 수 있는 식사

음료

탄산음료

과일 주스 및 꿀

알코올 음료

식물성 음료

유아 영양 및 이유식

유아용 조제 분유

이유식 제품

기타

제8장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

스페인

이탈리아

러시아

아시아태평양

중국

인도

일본

호주

한국

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

사우디아라비아

남아프리카

아랍에미리트(UAE)

제9장 기업 프로파일

Archer Daniels Midland Company(ADM)

Cargill, Inc.

Croda International Plc

Kerry Group plc

Corbion NV

Ingredion Incorporated

Lasenor Emul, SL

Palsgaard A/S

Lonza

Riken Vitamin

KTH

영문 목차

영문목차

The Global Food Emulsifiers Market was valued at USD 4.1 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 7.7 billion by 2034, driven by the increasing demand for convenience foods, plant-based ingredients, and clean-label products. Emulsifiers play a vital role in improving the structure, stability, and shelf life of food products. They are used across various food sectors such as bakery, dairy, frozen desserts, beverages, processed meats, ready-to-eat meals, and infant nutrition. With an increasing shift toward clean label and vegan-friendly options, natural and plant-based emulsifiers such as lecithin, sunflower, and soy are gaining traction. Moreover, the demand for mono- and diglycerides continues to dominate due to their versatility, cost-effectiveness, and wide application in functional and convenience foods.

In terms of regional growth, the Asia Pacific market is expanding rapidly due to changing dietary preferences and rising urbanization. Europe and North America, while mature markets, continue to maintain strong demand for natural, sustainable, and clean-label ingredients. The growing regulatory support for food safety and label transparency is also driving the innovation of emulsifier blends, strengthening their presence in modern food production processes.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$4.1 Billion

Forecast Value

$7.7 Billion

CAGR

6.6%

The mono- and diglycerides segment holds 34.8% share and is forecasted to grow at a CAGR of 6.4% by 2034. These emulsifiers are highly regarded for their versatility, cost-effectiveness, and wide application across multiple sectors, including bakery, dairy, confectionery, and processed foods. Their ability to act as stabilizers, emulsifiers, and texturizers, combined with their long shelf life and consistency, has cemented their position as one of the most used emulsifiers in the food industry. This widespread usage, coupled with their multifunctionality, ensures that mono and diglycerides remain a dominant choice in food manufacturing.

The plant-based emulsifiers segment held 39.5% share in 2024 and is expected to grow at a CAGR of 6.2% through 2034, driven by a noticeable shift in consumer preferences toward natural, plant-derived ingredients that align with a more sustainable and health-conscious lifestyle. As more consumers seek eco-friendly and clean-label products, the demand for emulsifiers derived from soy, sunflower, and canola is growing. These plant-based emulsifiers are gaining popularity due to their nutritional benefits, clean labeling, and sustainable sourcing, all of which align with the rising consumer demand for healthier and environmentally responsible food options.

U.S. Food Emulsifiers Market was valued at USD 592.6 million in 2024 due to its strong food processing industry and high consumption of convenience foods. The country's robust bakery, dairy, and frozen dessert sectors further support the demand for emulsifiers. Additionally, the growing health and wellness trends among U.S. consumers are driving the need for more innovative emulsifiers, including plant-based and natural alternatives. The well-established supply chains and marketing systems in the U.S. contribute to its competitive advantage in obtaining raw materials from both local and international sources.

Leading players in the Global Food Emulsifiers Market, such as Cargill, Inc., Corbion N.V., Archer Daniels Midland Company (ADM), Kerry Group plc, and Croda International Plc, are focusing on diversifying their product portfolios and expanding their market presence. These companies are investing heavily in research and development to create cleaner, plant-based emulsifiers that meet the growing consumer demand for sustainable products. They are also enhancing their production processes to improve efficiency and reduce costs. Partnerships, mergers, and acquisitions are key strategies used by these companies to expand their market footprint and improve their competitive positioning in the global food emulsifier sector.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definition

1.2 Base estimates & calculations

1.3 Forecast calculation

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

1.5 Primary research and validation

1.5.1 Primary sources

1.5.2 Data mining sources

Chapter 2 Executive Summary

2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Factor affecting the value chain

3.1.2 Profit margin analysis

3.1.3 Disruptions

3.1.4 Future outlook

3.1.5 Manufacturers

3.1.6 Distributors

3.2 Trump administration tariffs

3.2.1 Impact on trade

3.2.1.1 Trade volume disruptions

3.2.1.2 Retaliatory measures

3.2.2 Impact on the industry

3.2.2.1 Supply-side impact (raw materials)

3.2.2.1.1 Price volatility in key materials

3.2.2.1.2 Supply chain restructuring

3.2.2.1.3 Production cost implications

3.2.2.2 Demand-side impact (selling price)

3.2.2.2.1 Price transmission to end markets

3.2.2.2.2 Market share dynamics

3.2.2.2.3 Consumer response patterns

3.2.3 Key companies impacted

3.2.4 Strategic industry responses

3.2.4.1 Supply chain reconfiguration

3.2.4.2 Pricing and product strategies

3.2.4.3 Policy engagement

3.2.5 Outlook and future considerations

3.3 Trade statistics (HS Code)

3.3.1 Major exporting countries, 2021 - 2024 (Kilo Tons)

3.3.2 Major importing countries, 2021 - 2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only.

3.4 Consumer trends and preferences

3.4.1 Clean label movement

3.4.1.1 Consumer perception of emulsifiers

3.4.1.2 Natural vs. synthetic preferences

3.4.1.3 Impact on product formulation

3.4.2 Health and wellness trends

3.4.2.1 Nutritional concerns

3.4.2.2 Allergen considerations

3.4.2.3 Dietary restrictions impact

3.4.3 Sustainability and ethical considerations

3.4.3.1 Environmental impact awareness

3.4.3.2 Sustainable sourcing preferences

3.4.3.3 Packaging considerations

3.4.4 Plant-based vegan trends

3.4.4.1 Demand for plant-derived emulsifiers

3.4.4.2 Vegan certification impact

3.4.5 Transparency and traceability demands

3.4.6 Regional consumer preference variations

3.5 Consumer behavior analysis

3.5.1 Purchase decision factors

3.5.2 Price sensitivity analysis

3.5.3 Brand loyalty patterns

3.6 Social media and digital influence on consumer perception

3.7 Supply chain and raw material analysis

3.7.1 Raw material sourcing analysis

3.7.1.1 Key raw materials

3.7.1.2 Sourcing regions

3.7.1.3 Sustainability in sourcing

3.7.2 Production process analysis

3.7.2.1 Manufacturing technologies

3.7.2.2 Quality control measures

3.7.2.3 Cost structure analysis

3.7.3 Distribution channel analysis

3.7.3.1 Direct vs. indirect channels

3.7.3.2 E-commerce impact

3.7.3.3 Distribution challenges

3.7.4 Supply chain challenges

3.7.4.1 Raw material price volatility

3.7.4.2 Supply chain disruptions

3.7.4.3 Logistics challenges

3.7.5 Supply chain optimization strategies

3.7.6 Sustainable supply chain practices

3.7.7 Technology integration in supply chain

3.8 Pricing analysis and cost structure

3.8.1 Price point analysis by product type

3.8.2 Price trend analysis 2021–2025

3.8.3 Price forecast 2025–2034

3.8.4 Factors affecting pricing

3.8.4.1 Raw material costs

3.8.4.2 Production costs

3.8.4.3 Regulatory compliance costs

3.8.4.4 Market competition

3.8.4.5 Regional price variations

3.8.4.6 Pricing strategies of key players

3.8.4.7 Cost structure analysis

3.8.4.8 Raw material costs

3.8.4.9 Manufacturing costs

3.8.4.10 Distribution costs

3.8.4.11 Marketing and sales costs

3.8.5 Profitability analysis by product segment

3.9 Technological advancements and innovations

3.9.1 Recent technological developments

3.9.2 Emerging technologies in emulsifier production

3.9.2.1 Enzymatic modification

3.9.2.2 Microencapsulation

3.9.2.3 Nanotechnology applications

3.9.3 Clean label innovations

3.9.3.1 Natural emulsifier alternatives

3.9.3.2 Enzyme-based solutions

3.9.3.3 Plant-based innovations

3.9.4 Sustainable production technologies

3.9.5 Functional improvements

3.9.5.1 Enhanced stability

3.9.5.2 Improved texture properties

3.9.5.3 Extended shelf life solutions

3.9.6 Digital technologies in production and quality control

3.9.7 Patent analysis and r&d trends

3.9.8 Future technology roadmap

3.10 Sustainability and environmental impact

3.10.1 Environmental footprint of emulsifiers

3.10.1.1 Carbon footprint analysis

3.10.1.2 Water usage assessment

3.10.1.3 Waste generation and management

3.10.2 Sustainable sourcing practices

3.10.2.1 Palm oil sustainability issues

3.10.2.2 Soy sourcing challenges

3.10.2.3 Alternative sustainable sources

3.10.3 Biodegradability and eco-toxicity assessment

3.10.4 Circular economy approaches

3.10.5 Industry sustainability initiatives

3.10.6 Regulatory pressures for sustainability

3.10.7 Consumer demand for sustainable products

3.10.8 Cost-benefit analysis of sustainable practices

3.11 Market challenges and opportunities

3.11.1 Key market challenges

3.11.1.1 Health concerns and negative perception

3.11.1.2 Regulatory hurdles

3.11.1.3 Raw material price volatility

3.11.1.4 Clean label formulation challenges

3.11.2 Market opportunities

3.11.2.1 Plant-based emulsifier development

3.11.2.2 Emerging markets expansion

3.11.2.3 Functional food applications

3.11.2.4 Sustainable emulsifier solutions

3.11.3 Impact of macro-economic factors

3.11.4 Technological opportunity assessment

3.11.5 Strategic opportunity mapping

3.12 Future market outlook and forecast

3.12.1 Market forecast by product type 2025–2030

3.12.2 Market forecast by application 2025–2030

3.12.3 Market forecast by region 2025–2030

3.12.4 Emerging market trends

3.12.5 Future growth drivers

3.12.6 Market evolution scenarios

3.12.6.1 Optimistic scenario

3.12.6.2 Realistic scenario

3.12.6.3 Pessimistic scenario

3.12.7 Investment opportunities assessment

3.12.8 Future competitive landscape projection

3.13 Strategic recommendations

3.13.1 Market entry strategies

3.13.2 Product development recommendations

3.13.3 Regional expansion opportunities

3.13.4 Competitive positioning strategies

3.13.5 Sustainability implementation roadmap

3.13.6 Digital transformation strategies

3.13.7 Regulatory compliance strategies

3.13.8 Marketing and branding recommendations

3.13.9 Risk mitigation strategies

3.13.10 Investment prioritization framework

3.14 Supplier landscape

3.15 Profit margin analysis

3.16 Key news & initiatives

3.17 Regulatory landscape

3.18 Impact forces

3.18.1 Growth drivers

3.18.1.1 Growing beverage industry may fuel product demand

3.18.1.2 Increasing consumption of processed foods will foster industry growth

3.18.1.3 Growth in consumption of dairy products is likely to favor food emulsifier industry growth

3.18.2 Industry pitfalls & challenges

3.18.2.1 Growing health concerns

3.18.2.2 Clean label requirements for the product

3.19 Growth potential analysis

3.20 Porter’s analysis

3.21 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share analysis

4.3 Competitive positioning matrix

4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Type 2021 - 2034 (USD Billion, Kilo Tons)

5.1 Key trends

5.2 Mono- and Di-glycerides

5.3 Lecithin

5.4 Sorbitan esters

5.5 Stearoyl lactylates

5.6 Polyglycerol esters

5.7 Polysorbates

5.8 Others (DATEM, CSL, etc.)

Chapter 6 Market Size and Forecast, By Source, 2021 - 2034 (USD Billion, Kilo Tons)

6.1 Key trends

6.2 Plant-based emulsifiers

6.3 Soy-derived

6.4 Sunflower-derived

6.5 Palm-derived

6.6 Other plant sources

6.7 Animal-based emulsifiers

6.8 Synthetic emulsifiers

Chapter 7 Market Size and Forecast, By Application, 2021 - 2034 (USD Billion, Kilo Tons)

7.1 Key trends

7.2 Bakery and confectionery

7.2.1 Bread and rolls

7.2.2 Cakes and pastries

7.2.3 Biscuits and cookies

7.2.4 Chocolate and confectionery

7.3 Dairy and frozen desserts

7.3.1 Ice cream and frozen desserts

7.3.2 Milk and cream products

7.3.3 Cheese products

7.3.4 Yogurt and fermented dairy

7.4 Processed meat and seafood

7.4.1 Sausages and processed meats

7.4.2 Seafood products

7.5 Convenience foods and ready meals

7.5.1 Soup and sauces

7.5.2 Dressings and mayonnaise

7.5.3 Ready-to-eat meals

7.6 Beverages

7.6.1 Carbonated drinks

7.6.2 Fruit juices and nectars

7.6.3 Alcoholic beverages

7.6.4 Plant-based beverage

7.7 Infant nutrition and baby food

7.7.1 Infant formula

7.7.2 Baby food products

7.8 Other

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)