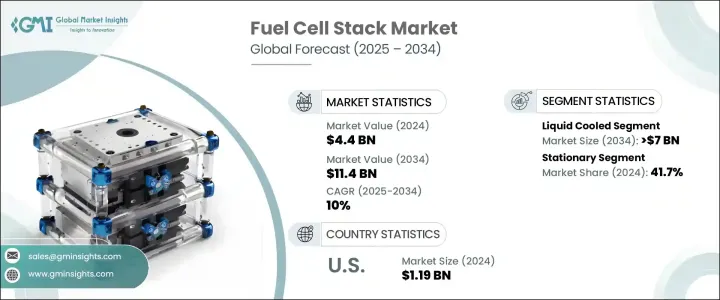

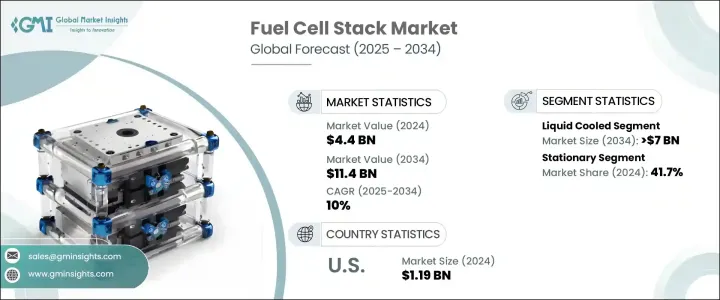

세계의 연료전지 스택 시장은 2024년에는 44억 달러로 평가되었고, CAGR 10%로 성장할 전망이며, 2034년에는 114억 달러에 이를 것으로 추정됩니다.

이 성장의 주요 요인은 연료전지를 포함한 지속 가능한 에너지 기술을 지원하는 규제 틀의 시행이 증가하고 있다는 것입니다. 국가와 산업계가 기후변화와 싸우고 온실가스 배출을 억제하는 노력을 강화하는 가운데 연료전지 스택은 다양한 용도로 큰 지지를 받고 있습니다. 세계 각국의 정부는 세제 혜택, 보조금, 연구 이니셔티브를 통해 청정 에너지 도입을 적극 추진하고 있어 시장 성장에 유리한 환경을 만들어 내고 있습니다. 기존의 에너지원이 환경에 미치는 영향에 대한 의식의 고조는 산업계에 제로 에미션 해결책으로의 시프트를 재촉하고 있으며, 이것이 연료전지 기술의 수요를 더욱 끌어올리고 있습니다. 게다가 수소 인프라 확대나, 특히 고성능차 및 대형차의 수송 수단으로의 연료전지의 통합은, 시장 개척의 새로운 길을 열 것으로 기대되고 있습니다. 성능, 비용 효율, 확장성 향상을 목표로 한 기술의 진보도 시장의 기세를 가속시키고 있습니다.

연료전지 스택 수요는 산업, 상업, 주택의 각 분야에서 청정에너지 대체를 지속적으로 추진하고 있는 것에 크게 영향을 받고 있습니다. 탈탄소화가 전략적 우선 사항이 됨에 따라 에너지 시스템에서 연료전지의 역할은 확대되고 있습니다. 하이브리드 셋업을 지원하고 그리드의 신뢰성을 향상시키며 효율적인 백업 전력을 제공하는 그 능력은 분야를 불문하고 매력적인 선택지가 되고 있습니다. 게다가 에너지 기업, 연구 기관, 제조업체를 포함한 이해 관계자간의 협력이, 제품 혁신 및 전개를 가속하는 데 도움이 되고 있습니다. 제조 프로세스를 합리화하고 재료 및 생산 기술의 개선을 통해 비용을 절감하는 노력으로 저렴한 가격과 입수 용이성이 향상되어 향후 수년간 폭넓은 채택이 가능할 것으로 예상됩니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 44억 달러 |

| 예측 금액 | 114억 달러 |

| CAGR | 10% |

제품 유형별로 볼 때 시장은 공냉식 연료전지 스택 및 액냉식 연료전지 스택으로 구분됩니다. 2022년에는 38억 달러, 2023년에는 41억 달러, 2024년에는 44억 달러를 기록했습니다. 이 중 액냉식 부문은 2034년까지 70억 달러를 넘을 것으로 예측되고 있습니다. 이 성장의 원동력이 되고 있는 것은, 연료 전지의 고출력 및 고부하 용도로의 사용 증가 및 고도의 열관리에 의한 성능 향상입니다. 액냉 시스템은 보다 안정적인 동작 조건, 보다 우수한 열방산, 긴 수명을 지원하기 때문에 안정적이고 신뢰성 높은 출력이 요구되는 분야에 최적입니다. 액체 냉각 시스템의 지속적인 개발로 성능 및 내구성이 중요시되는 산업용 및 상업용 백업 시스템에 점점 더 적합합니다.

연료전지 스택 시장은 용도별로 자동차, 거치형, 발전, 그 밖에 분류됩니다. 2024년에는 거치형 부문이 전체 시장의 41.7%를 차지했으며, 최대 점유율을 차지했습니다. 이러한 우위성은 거치형 연료전지 시스템의 진보 및 지속 가능하고 분산형 에너지 솔루션에 대한 수요 증가에 기인하고 있습니다. 산업계가 이산화탄소 배출량의 삭감을 목표로 하는 가운데, 거치형 연료전지 시스템은, 최소한의 배출량으로 빌딩이나 공장, 원격지의 시설에 전력을 공급하기 위해서 채용되고 있습니다. 또, 신재생 에너지원과의 호환성에 의해, 에너지 효율, 신뢰성, 백업 기능을 확보하는 하이브리드 시스템의 구축도 지원되고 있습니다.

지역별로는 북미가 2024년 세계 연료전지 스택 시장에서 28.7%의 점유율을 차지했습니다. 미국만의 시장 규모는 2022년 10억 5,000만 달러, 2023년 11억 1,000만 달러, 2024년 11억 9,000만 달러에 달했습니다. 이 지역의 개발을 뒷받침하는 것은 수소 충전 인프라의 정비와 연료 전지 자동차의 도입 확대입니다. 수소 공급망 정비에 민관이 지속적으로 투자함으로써 이 지역 시장은 더욱 강화되고 북미는 세계 연료전지 시장에서 중요한 위치를 차지할 것으로 예상됩니다.

시장 상황의 경쟁 구도는 기존 기업과 신흥 이노베이터를 특징으로 합니다. 주요 기업 5사(Plug Power, Ballard Power Systems, Fuel Cell Energy, Bloom Energy사, Doosan Fuel Cell)는, 합계로 시장 점유율 45% 이상을 차지하고 있습니다. 유력 기업이 생산 규모 확대와 시스템 비용 절감에 주력하는 한편, 신흥 기업은 니치 용도를 타겟으로 해, 신재생 에너지 기술과의 통합을 모색하고 있습니다. 각사가 제조 효율의 향상 및 대체 재료의 채용에 노력하는 가운데, 비용 대비 효과가 높고 확장성이 높은 연료 전지 솔루션을 제공하기 위한 경쟁이 격화하고 있습니다. 전략적 투자, 정부 지원, 청정 에너지 목표와의 정합은 시장 역학을 계속 재구축하여 업계 전체의 혁신과 경쟁을 촉진하고 있습니다.

The Global Fuel Cell Stack Market was valued at USD 4.4 billion in 2024 and is estimated to grow at a CAGR of 10% to reach USD 11.4 billion by 2034. This growth is largely fueled by the increasing enforcement of regulatory frameworks that support sustainable energy technologies, including fuel cells. As nations and industries intensify efforts to combat climate change and curb greenhouse gas emissions, fuel cell stacks are gaining significant traction across various applications. Governments around the world are actively promoting clean energy adoption through tax incentives, subsidies, and research initiatives, creating a favorable environment for market growth. Growing awareness of the environmental impact of conventional energy sources is prompting industries to shift toward zero-emission solutions, which is further bolstering the demand for fuel cell technology. Additionally, the expansion of hydrogen infrastructure and the integration of fuel cells into transportation-especially for high-performance and heavy-duty vehicles-are expected to create new avenues for market development. Technological advances aimed at improving performance, cost-efficiency, and scalability are also accelerating market momentum.

The demand for fuel cell stacks is heavily influenced by the continuous push for clean energy alternatives in the industrial, commercial, and residential sectors. As decarbonization becomes a strategic priority, the role of fuel cells in energy systems is expanding. Their ability to support hybrid setups, improve grid reliability, and provide efficient backup power makes them an attractive choice across sectors. Moreover, collaborations among stakeholders-including energy companies, research institutes, and manufacturers-are helping accelerate product innovation and deployment. Efforts to streamline manufacturing processes and reduce costs through improved materials and production techniques are expected to enhance affordability and accessibility, enabling broader adoption in the years ahead.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.4 Billion |

| Forecast Value | $11.4 Billion |

| CAGR | 10% |

In terms of product type, the market is segmented into air-cooled and liquid-cooled fuel cell stacks. The industry recorded USD 3.8 billion in 2022, USD 4.1 billion in 2023, and USD 4.4 billion in 2024. Among these, the liquid-cooled segment is projected to surpass USD 7 billion by 2034. This growth is being driven by the increasing use of fuel cells in high-power and intensive-duty applications, along with enhanced performance enabled by advanced thermal management. Liquid cooling systems support more stable operating conditions, better heat dissipation, and extended lifespan-making them ideal for sectors that demand consistent and reliable power output. The ongoing development of liquid-cooled systems is making them increasingly suitable for industrial and commercial backup systems where performance and durability are critical.

On the basis of application, the fuel cell stack market is categorized into automotive, stationary, power generation, and others. In 2024, the stationary segment held the largest share, accounting for 41.7% of the overall market. This dominance can be attributed to advancements in stationary fuel cell systems and the growing demand for sustainable and decentralized energy solutions. As industries seek to reduce their carbon footprints, stationary fuel cell systems are being adopted to power buildings, factories, and remote facilities with minimal emissions. Their compatibility with renewable energy sources also supports the creation of hybrid systems that ensure energy efficiency, reliability, and backup capabilities.

Regionally, North America held a 28.7% share of the global fuel cell stack market in 2024. The U.S. market alone was valued at USD 1.05 billion in 2022, USD 1.11 billion in 2023, and USD 1.19 billion in 2024. Growth in this region is supported by the development of hydrogen refueling infrastructure and increased deployment of fuel cell-powered vehicles. Continued public and private investment in building out hydrogen distribution networks is expected to strengthen the regional market further, positioning North America as a key player in the global fuel cell landscape.

The competitive landscape of the fuel cell stack market is marked by a combination of established companies and emerging innovators. The top five players- Plug Power, Ballard Power Systems, FuelCell Energy, Bloom Energy, and Doosan Fuel Cell-collectively contribute over 45% of the total market share. While dominant firms focus on scaling up production and reducing system costs, startups are targeting niche applications and exploring integration with renewable energy technologies. As companies strive to enhance manufacturing efficiency and adopt alternative materials, the race to provide cost-effective and scalable fuel cell solutions is intensifying. Strategic investments, government support, and alignment with clean energy goals continue to reshape market dynamics, encouraging innovation and competition throughout the industry.