자동차 솔라 패널 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Vehicle-Integrated Solar Panels Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1750446

리서치사:Global Market Insights Inc.

발행일:2025년 05월

페이지 정보:영문 160 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

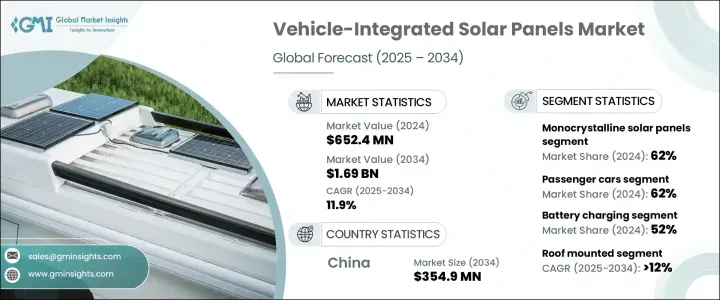

세계의 자동차 솔라 패널 시장은 2024년 6억 5,240만 달러로 평가되었고, 전동 이동성으로의 이행이 넓어지고, 재생에너지에 대한 세계의 뒷받침이 강해지고 있는 가운데, 차량 통합형 솔라 시스템 수요가 견인해, CAGR 11.9%로 성장하여 2034년에는 16억 9,000만 달러에 달할 것으로 예상됩니다.

운송 시스템의 현대화에 따라 자동차 제조업체는 외부 충전 시스템에 대한 의존성을 줄이기 위해 태양광 발전을 자동차에 직접 통합하는 것을 고려하고 있습니다.

환경 의식, 불안정한 연료 가격, 탈탄소 교통 솔루션에 대한 정부 지원 증가가 시장 성장에 기여하고 있습니다. 바이어는 내열 솔라 소재, 원활한 디자인 통합, 실시간 에너지 추적 등 선진적인 차량 기능을 우선하고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

6억 5,240만 달러

예측 금액

16억 9,000만 달러

CAGR

11.9%

승용차는 2024년에 62%의 점유율을 차지해 시장을 선도해 2034년까지 연평균 복합 성장률(CAGR) 12.3%를 보일 것으로 예측됩니다. 이러한 차량은 표면이 평평하고 공기역학적으로 뛰어나므로 VISP 기술에 이상적인 플랫폼이 됩니다. 일사량이 많은 지역에서는 자기충전 능력이 도시와 도시 간의 이동에 특히 귀중한 것이 됩니다.

단결정 솔라 패널 부문은 62%의 점유율을 차지하며, 2034년까지의 CAGR은 12.2%로 예상되고 있습니다. 그늘이나 고온의 환경에서도 잘 동작하는 것으로 알려진 단결정 패널은 자동차의 루프탑이나 보닛에 최적입니다. 세련된 외관과 일관된 질감에 의해 성능과 미관이 중시되는 프리미엄 EV에 인기가 있습니다.

아시아태평양의 차재 일체형 태양광 패널 시장은 2024년에 48%의 점유율을 차지합니다. 유망의 확대, 급속한 도시화가 트럭 탑재형 너클 붐 크레인과 같은 다목적 리프팅 솔루션의 필요성을 부추기고 있습니다.

Sono Motors, Volkswagen, Toyota Motor, BYD, Nissan Motor, Lightyear, Planet Solar, Aptera Motors, General Motors, Ford Motor와 같은 주요 업계 참여 기업들은 경쟁력을 유지하기 위해 전략적 제휴와 기술 업그레이드를 진행하고 있습니다. 태양전지기술기업과의 전략적 제휴와 대상시장에서의 시험차량의 전개도 일반적입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

원재료 공급자

부품 공급자

제조업체

서비스 제공업체

도매업체

최종 용도

트럼프 정권에 의한 관세에 대한 영향

무역에 미치는 영향

무역량의 혼란

보복 조치

업계에 미치는 영향

공급측의 영향(원재료)

주요 원재료의 가격 변동

공급망 재구성

생산 비용에 미치는 영향

수요측의 영향(고객에 대한 비용)

최종 시장에의 가격 전달

시장 점유율 동향

소비자의 반응 패턴

영향을 받는 주요 기업

전략적인 업계 대응

공급망 재구성

가격 설정 및 제품 전략

정책관여

전망과 향후 검토 사항

이익률 분석

기술과 혁신의 상황

특허 분석

주요 뉴스와 대처

규제 상황

가격 동향

제품

지역

코스트 내역 분석

영향요인

성장 촉진요인

전기자동차의 보급 증가

태양광 패널의 효율에 있어서의 기술적 진보

태양광 발전 기술의 비용 저하

신재생에너지에 대한 소비자의 의식의 고조

환경규제와 탄소삭감 목표

업계의 잠재적 위험 및 과제

통합의 높은 초기 비용

내구성과 안전성에 대한 우려

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

제4장 경쟁 구도

소개

기업의 시장 점유율 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 차량별, 2021-2034년

주요 동향

승용차

해치백

세단

SUV

상용차

소형 상용차

중형 상용차

대형 상용차

전기자동차(EV)

특수 차량

레크리에이션 차량(RV)

골프 카트

군용 차량 또는 긴급 차량

제6장 시장 추계 및 예측 : 솔라 패널별, 2021-2034년

주요 동향

단결정 태양전지판

다결정 태양전지판

박막 태양전지 패널

플렉서블 솔라 패널

제7장 시장 추계 및 예측 : 설치 방법별, 2021-2034년

주요 동향

지붕 장착

후드 장착

일체형 바디 패널

분리 가능 패널

제8장 시장 추계 및 예측 : 용도별, 2021-2034년

주요 동향

발전

배터리 충전

보조 전원

난방 시스템

제9장 시장 추계 및 예측 : 지역별, 2021-2034년

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

러시아

북유럽 국가

아시아태평양

중국

인도

일본

한국

호주 및 뉴질랜드

동남아시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

아랍에미리트(UAE)

사우디아라비아

남아프리카

제10장 기업 프로파일

Aptera Motors

BYD

Cruise Car

Ford Motor

General Motors

Hanergy Thin Film

Honda Motor

Hyundai Motor

Lightyear

LOMOcean

Mahindra & Mahindra

Nissan Motor

Planet Solar

Sono Motors

Surat Exim

Tesla

Toyota Motor

Venturi Automobiles

Volkswagen

Weifang Guangsheng New Energy

JHS

영문 목차

영문목차

The Global Vehicle-Integrated Solar Panels Market was valued at USD 652.4 million in 2024 and is estimated to grow at a CAGR of 11.9% to reach USD 1.69 billion by 2034, driven by the demand for vehicle-integrated solar systems with the widespread shift toward electric mobility and the growing global push for renewable energy. As transportation systems modernize, vehicle manufacturers are increasingly looking to integrate solar power directly into vehicles to reduce reliance on external charging systems. VISPs enable clean, self-sustaining energy generation, helping extend the operational range of electric vehicles while alleviating pressure on onboard batteries.

Environmental awareness, volatile fuel prices, and growing government support for decarbonized transportation solutions contribute to market growth. Automakers are responding by innovating more efficient solar materials, enhancing their integration with vehicle designs, and optimizing energy conversion rates. Consumer interest is expanding, especially in sunny regions, where solar-powered cars can deliver greater energy independence. Buyers prioritize advanced vehicle features such as thermal-resistant solar materials, seamless design integration, and real-time energy tracking. The evolution of direct-to-consumer digital sales channels boosts visibility for solar-enabled vehicles and related aftermarket kits, allowing manufacturers to reach a broader demographic base.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$652.4 Million

Forecast Value

$1.69 Billion

CAGR

11.9%

Passenger vehicles led the market in 2024, making up 62% share, and are expected to grow at 12.3% CAGR through 2034. These vehicles provide ideal platforms for VISP technology due to their flat, aerodynamic surfaces. This design allows solar systems to generate higher electricity outputs from limited space. In regions with high solar exposure, the ability to self-charge becomes especially valuable for urban and intercity mobility. With a strong appeal among environmentally conscious drivers, solar-integrated systems are rapidly becoming a differentiator in the EV space.

The monocrystalline solar panels segment held 62% share and is expected to grow at a CAGR of 12.2% through 2034. These panels are favored for their superior energy conversion efficiency and visual uniformity. Known for operating well in shaded and high-temperature environments, monocrystalline panels are ideal for vehicle rooftops and hoods. Their sleek appearance and consistent texture make them popular for premium EVs where performance and aesthetics matter.

Asia Pacific Vehicle- Integrated Solar Panels Market held a 48% share in 2024. Strong domestic production capabilities, cost-effective manufacturing, and government-led renewable mobility policies have propelled China's leadership in VISP adoption. Additionally, the country's robust infrastructure development, expansion of smart logistics networks, and rapid urbanization have fueled the need for versatile lifting solutions like truck-mounted knuckle boom cranes. Local manufacturers benefit from economies of scale and streamlined supply chains, enabling faster production and competitive pricing.

Key industry participants such as Sono Motors, Volkswagen, Toyota Motor, BYD, Nissan Motor, Lightyear, Planet Solar, Aptera Motors, General Motors, and Ford Motor are pursuing strategic collaborations and technology upgrades to stay competitive. Many invest in R&D to enhance solar cell durability, energy efficiency, and integration with EV platforms. Strategic partnerships with solar tech firms and the rollout of pilot vehicles in target markets are also common. Some players optimize direct-to-consumer online sales models, while others focus on modular VISP solutions for fleet adoption and last-mile logistics applications.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Research design

1.1.1 Research approach

1.1.2 Data collection methods

1.2 Base estimates and calculations

1.2.1 Base year calculation

1.2.2 Key trends for market estimates

1.3 Forecast model

1.4 Primary research & validation

1.4.1 Primary sources

1.4.2 Data mining sources

1.5 Market definitions

Chapter 2 Executive Summary

2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.2 Supplier landscape

3.2.1 Raw material supplier

3.2.2 Component supplier

3.2.3 Manufacturer

3.2.4 Service provider

3.2.5 Distributor

3.2.6 End use

3.3 Impact of Trump administration tariffs

3.3.1 Trade impact

3.3.1.1 Trade volume disruptions

3.3.1.2 Retaliatory measures

3.3.2 Impact on industry

3.3.2.1 Supply-side impact (raw materials)

3.3.2.1.1 Price volatility in key materials

3.3.2.1.2 Supply chain restructuring

3.3.2.1.3 Production cost implications

3.3.2.2 Demand-side impact (Cost to customers)

3.3.2.2.1 Price transmission to end markets

3.3.2.2.2 Market share dynamics

3.3.2.2.3 Consumer response patterns

3.3.3 Key companies impacted

3.3.4 Strategic industry responses

3.3.4.1 Supply chain reconfiguration

3.3.4.2 Pricing and product strategies

3.3.4.3 Policy engagement

3.3.5 Outlook & future considerations

3.4 Profit margin analysis

3.5 Technology & innovation landscape

3.6 Patent analysis

3.7 Key news & initiatives

3.8 Regulatory landscape

3.9 Pricing trend

3.9.1 Product

3.9.2 Region

3.10 Cost breakdown analysis

3.11 Impact on forces

3.11.1 Growth drivers

3.11.1.1 Rising adoption of electric vehicles

3.11.1.2 Technological advancements in solar panel efficiency

3.11.1.3 Decreasing cost of solar technology

3.11.1.4 Growing consumer awareness of renewable energy

3.11.1.5 Environmental regulations and carbon reduction goals