차량 통합 태양전지 반도체 시장 : 시장 기회 및 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)

Vehicle-Integrated Solar Cell Semiconductors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1858854

리서치사:Global Market Insights Inc.

발행일:2025년 10월

페이지 정보:영문 220 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

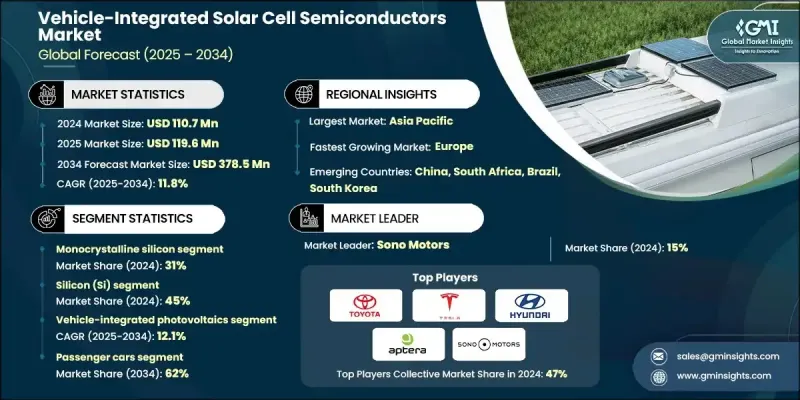

세계의 차량 통합 태양전지 반도체 시장은 2024년에는 1억 1,070만 달러로 평가되었고, CAGR 11.8%로 성장할 전망이며, 2034년에는 3억 7,850만 달러에 달할 것으로 예측되고 있습니다.

시장 성장의 원동력이 되고 있는 것은 전기자동차 보급의 가속, 반도체 기술의 계속적인 진보, 에너지 효율이 높고 안전한 전원 솔루션에 대한 수요 증가입니다. 이 기세는 스마트 모빌리티 혁신의 융합, 차재 전자의 강화, 차재 반도체 에코시스템 내의 경쟁 역학의 변화에 의한 영향이 큽니다. 특히 아시아와 유럽에서는 칩의 현지화 및 공급망의 강인성이 포스트 팬데믹에 중점을 두고 있는 것도 이 성장에 기여하고 있습니다. 이 지역은 전동화된 교통 및 디지털 인프라에 대한 투자 증가에 힘입어 첨단 반도체 제조의 핫스팟이 되고 있습니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시장 규모

1억 1,070만 달러

예측 금액

3억 7,850만 달러

CAGR

11.8%

세계 자동차의 전기화 및 자동차 에너지 효율 요구에 따라 자동차 제조업체와 Tier-1 공급업체는 태양전지가 스마트 인버터, 존 컨트롤러, 고급 전력 관리 IC와 원활하게 작동하는 칩 레벨 통합에 대한 투자를 추진하고 있습니다. 이러한 컴포넌트는 현재 태양전지 모듈과 직접 작동하도록 개발되어 있어 높은 에너지 효율과 보다 컴팩트한 시스템 설계를 가능하게 합니다. 자동차가 지능형 커넥티드 시스템으로 진화함에 따라 반도체 네트워킹 및 아키텍처 혁신은 이러한 변화를 지원하는 데 매우 중요해지고 있습니다.

재료별로 실리콘 부문은 2024년에 45%의 점유율을 차지하였고, 2034년까지 12%의 연평균 복합 성장률(CAGR)로 성장할 전망입니다. 실리콘의 이점은 높은 신뢰성, 성숙한 공급망 및 다양한 조명 조건 하에서의 성능을 뒷받침합니다. 동시에, 구리 인듐 갈륨 셀레나이드(CIGS)는 그 유연성과 자동차의 곡면에 대한 적합성에 의해 채용이 증가하고 있습니다.

단결정 실리콘 부문은 2024년에 31%의 점유율을 차지했으며, 2025-2034년 CAGR 12.6%로 성장할 것으로 예측됩니다. 안정적인 전력 공급과 내구성으로 EV와 하이브리드 모델의 바디 일체형 태양전지판과 루프탑 형 태양전지판에 최적입니다.

아시아태평양 차량 통합 태양전지 반도체 시장은 2024년에 42.3%의 점유율을 차지했으며, 자동차와 일렉트로닉스 제조의 강력한 진전이 그 원동력이 되고 있습니다. 한편 유럽은 엄격한 안전 규제, 급속한 EV 통합, 효율적이고 차량에 탑재 가능한 에너지 솔루션을 창출하기 위한 태양 기술과 반도체 로직의 융합이 진행되고 있는 점에서 급성장 지역으로 부상하고 있습니다.

세계의 차량 통합 태양전지 반도체 시장을 형성하는 주요 기업으로는 Tesla, BYD, Aptera, Toyota, Go Ford, Lightyear, PlanetSolar, Hyundai, Sono Motors 등이 있습니다. 이러한 기업들은 차세대 반도체를 태양광 기술과 통합함으로써 스마트 에너지 생산 차량의 진화에 적극적으로 기여하고 있습니다. 업계별 시장의 주요 기업은 혁신, 협업, 수직 통합을 조합하여 활용하여 시장에서의 존재감을 높이고 있습니다. 많은 기업들은 고효율 에너지 변환 및 태양전지와의 원활한 통합을 가능하게 하는 반도체를 개발하기 위해 연구개발에 많은 투자를 하고 있습니다. 자동차 제조업체와 Tier-1 공급업체와의 전략적 파트너십은 EV에서 태양에너지 이용을 최적화하는 에너지 관리 시스템의 공동 개발을 촉진하고 있습니다.

목차

제1장 조사 방법

시장 범위 및 정의

조사 디자인

조사 접근

데이터 수집 방법

데이터 마이닝 정보원

세계

지역 및 국가

기본 추정 및 계산

기준 연도의 산출

시장 추계의 주요 동향

1차 조사 및 검증

1차 정보

예측 모델

조사의 전제조건 및 한계

제2장 주요 요약

제3장 업계 인사이트

생태계 분석

공급자의 상황

이익률 분석

비용 구조

각 단계에서의 부가가치

밸류체인에 영향을 주는 요인

혁신

업계에 미치는 영향요인

성장 촉진요인

전기차 및 하이브리드차의 보급 확대

태양전지 반도체의 효율 향상

그린 모빌리티 및 에너지 효율이 높은 자동차에 대한 정부의 인센티브

에너지 자율주행차 및 스마트카로의 시프트

지속가능하고 프리미엄 자동차 설계에 대한 소비자 수요 증가

업계의 잠재적 위험 및 과제

가혹한 자동차 환경 하에서의 내구성 및 신뢰성

높은 제조 및 통합 비용

시장 기회

페로브스카이트 반도체 및 탠덤 반도체의 연구개발 투자 증가

항속 거리 연장을 위한 EV 및 하이브리드 플랫폼과의 통합

이륜차 및 삼륜차 시장에 대한 진출

투명 및 유리 일체형 PV 시스템의 등장

성장 가능성 분석

규제 상황

지역별 태양전지 통합 규제

국제 규격의 조화

환경 규제의 영향

수출입 규제

Porter's Five Forces 분석

PESTEL 분석

기술 혁신의 전망

현재의 기술 동향

신흥 기술

특허 분석

비용 내역 분석

지속가능성 및 환경면

지속가능한 실천

폐기물 감축 전략

생산에서의 에너지 효율

환경 친화적인 노력

탄소발자국

향후 전망 및 로드맵

지속가능한 에너지 솔루션

이업종 융합 동향

규제의 진화 및 표준화

시장 통합 및 파트너십 전략

차재 등급 솔라 반도체 공급망

자동차 자격 요건

장기 공급 보증 전략

품질 경영 시스템 요건

공급망의 위험 완화

태양전지 공급에 대한 지정학적 영향

비용 효과 및 에너지 생성 최적화

태양전지의 와트 단가 분석

설치 및 통합 비용 요인

에너지 회수 시간의 계산

총소유 비용 모델

성능과 가격의 트레이드오프 분석

자동차 안전 기준 및 태양광 통합

전기 안전 요건(ISO 6469)

화재 안전성 및 열폭주 방지

충돌 안전성 및 태양전지판의 거동

고전압 시스템 통합의 안전성

긴급 대응 순서

차세대 솔라 기술의 진화

페로브스카이트 태양전지 개발

유기 태양전지의 진보

투명 태양전지의 혁신

플렉서블 솔라 필름의 진화

다접합 셀의 통합

집광형 태양광 발전 용도

에너지 관리 및 차량 시스템 통합

태양에너지 수확 최적화

배터리 관리 시스템의 통합

파워 일렉트로닉스 및 변환 효율

에너지 저장 전략 최적화

부하 관리 및 우선 순위 지정

제4장 경쟁 구도

서문

기업의 시장 점유율 분석

북미

유럽

아시아태평양

라틴아메리카

중동 및 아프리카

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략적 전망 매트릭스

주요 발전

합병 및 인수

파트너십 및 협업

신제품 발표

확장계획 및 자금조달

제5장 시장 추계 및 예측 : 반도체별(2021-2034년)

주요 동향

단결정 실리콘

다결정 실리콘

박막

페로브스카이트 태양전지

멀티 정션

유기 태양전지(OPV)

제6장 시장 추계 및 예측 : 재료 유형별(2021-2034년)

주요 동향

실리콘(Si)

구리 인듐 갈륨 셀레늄화물

카드뮴 텔룰라이드(CdTe)

페로브스카이트 화합물

투명 전도성 산화물

폴리머 기판

제7장 시장 추계 및 예측 : 통합 유형별(2021-2034년)

주요 동향

차재용 태양광 발전

차재용 태양광 발전

유리 통합형 PV

바디 패널 일체형 PV

제8장 시장 추계 및 예측 : 자동차 유형별(2021-2034년)

주요 동향

승용차

상용차

전기자동차

이륜차 및 삼륜차

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

주요 동향

트랙션 파워 보충제

배터리 충전

에어컨

텔레매틱스

에너지 수확

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

독일

영국

프랑스

이탈리아

스페인

러시아

북유럽 국가

포르투갈

크로아티아

아시아태평양

중국

인도

일본

호주

한국

싱가포르

태국

인도네시아

라틴아메리카

브라질

멕시코

아르헨티나

중동 및 아프리카

남아프리카

사우디아라비아

아랍에미리트(UAE)

튀르키예

제11장 기업 프로파일

세계 기업

Toyota

Hyundai

Lightyear

BMW Group

Mercedes-Benz

Audi AG

Nissan Motor

BYD Company

Tesla

Suno

Aptera

Goford

지역 기업

Panasonic

Sharp

SunPower

Hanwha Q CELLS

First Solar

Canadian Solar

JinkoSolar Holding

LONGi Solar

신흥 기업

Ubiquitous Energy

Heliatek

Oxford Photovoltaics

Saule Technologies

Solarmer Energy

Armor

Infinite Power Solutions

AJY

영문 목차

영문목차

The Global Vehicle-Integrated Solar Cell Semiconductors Market was valued at USD 110.7 million in 2024 and is estimated to grow at a CAGR of 11.8% to reach USD 378.5 million by 2034.

Market growth is fueled by the acceleration of electric vehicle adoption, ongoing advances in semiconductor technology, and increasing demand for energy-efficient and secure power solutions. This momentum is largely influenced by the convergence of smart mobility innovations, enhanced vehicle electronics, and shifting competitive dynamics within the automotive semiconductor ecosystem. Post-pandemic emphasis on chip localization and supply chain resilience has also contributed to this growth, particularly across Asia and Europe. These regions are becoming hotspots for advanced semiconductor manufacturing, supported by rising investments in electrified transportation and digital infrastructure.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$110.7 Million

Forecast Value

$378.5 Million

CAGR

11.8%

Global vehicle electrification and the demand for in-vehicle energy efficiency are pushing automakers and Tier-1 suppliers to invest in chip-level integration, where solar cells work seamlessly with smart inverters, zonal controllers, and advanced power management ICs. These components are now being developed to operate directly with photovoltaic modules, enabling greater energy efficiency and more compact system designs. As vehicles evolve into intelligent, connected systems, innovations in semiconductor networking and architecture are becoming crucial in supporting this transformation.

In terms of materials, the silicon segment held a 45% share in 2024 and is forecasted to grow at a 12% CAGR through 2034. Silicon's dominance is backed by its high reliability, mature supply chains, and performance in diverse lighting conditions. At the same time, copper indium gallium selenide (CIGS) is seeing rising adoption due to its flexibility and suitability for curved vehicle surfaces.

The monocrystalline silicon segment accounted for a 31% share in 2024 and is expected to grow at a CAGR of 12.6% during 2025-2034. Its consistent power delivery and durability make it ideal for body-integrated and rooftop solar panels in EVs and hybrid models.

Asia-Pacific Vehicle-Integrated Solar Cell Semiconductors Market held 42.3% share in 2024, driven by strong progress in automotive and electronics manufacturing. Meanwhile, Europe is emerging as the fastest-growing region due to stringent safety regulations, rapid EV integration, and increasing fusion of solar technology with semiconductor logic to create efficient, vehicle-ready energy solutions.

Key players shaping the Global Vehicle-Integrated Solar Cell Semiconductors Market include Tesla, BYD, Aptera, Toyota, Go Ford, Lightyear, PlanetSolar, Hyundai, and Sono Motors. These companies are actively contributing to the evolution of smart, energy-producing vehicles by integrating next-gen semiconductors with solar technologies. Leading companies in the Vehicle-Integrated Solar Cell Semiconductors Market are leveraging a mix of innovation, collaboration, and vertical integration to expand their market presence. Many are investing heavily in R&D to develop semiconductors that enable high-efficiency energy conversion and seamless integration with solar cells. Strategic partnerships with automakers and Tier-1 suppliers are facilitating the co-development of energy management systems that optimize solar energy usage in EVs.

Table of Contents

Chapter 1 Methodology

1.1 Market scope and definition

1.2 Research design

1.2.1 Research approach

1.2.2 Data collection methods

1.3 Data mining sources

1.3.1 Global

1.3.2 Regional/Country

1.4 Base estimates and calculations

1.4.1 Base year calculation

1.4.2 Key trends for market estimation

1.5 Primary research and validation

1.5.1 Primary sources

1.6 Forecast model

1.7 Research assumptions and limitations

Chapter 2 Executive Summary

2.1 Industry 360° synopsis, 2021 - 2034

2.2 Key market trends

2.2.1 Regional

2.2.2 Semiconductor

2.2.3 Material Type

2.2.4 Integration Type

2.2.5 Vehicle

2.2.6 Application

2.3 TAM Analysis, 2025-2034

2.4 CXO perspectives: Strategic imperatives

2.4.1 Executive decision points

2.4.2 Critical success factors

2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

3.1 Industry ecosystem analysis

3.1.1 Supplier landscape

3.1.2 Profit margin analysis

3.1.3 Cost structure

3.1.4 Value addition at each stage

3.1.5 Factor affecting the value chain

3.1.6 Disruptions

3.2 Industry impact forces

3.2.1.1 Growth drivers

3.2.1.2 Rising adoption of electric and hybrid vehicles

3.2.1.3 Advancements in solar semiconductor efficiency

3.2.1.4 Government incentives for green mobility and energy-efficient vehicles

3.2.1.5 Shift toward energy-autonomous and smart vehicles

3.2.1.6 Growing consumer demand for sustainable and premium vehicle designs

3.2.2 Industry pitfalls and challenges

3.2.2.1 Durability and reliability under harsh automotive conditions

3.2.2.2 High manufacturing and integration costs

3.2.3 Market opportunities

3.2.3.1 Rising investments in perovskite and tandem semiconductor R&D

3.2.3.2 Integration with EV and hybrid platforms for range extension

3.2.3.3 Expansion into two- and three-wheeler markets

3.2.3.4 Emergence of transparent and glass-integrated PV systems

3.3 Growth potential analysis

3.4 Regulatory landscape

3.4.1 Regional solar integration regulations

3.4.2 International standards harmonization

3.4.3 Environmental Regulation Impact

3.4.4 Import/Export Restrictions

3.5 Porter's analysis

3.6 PESTEL analysis

3.7 Technology and innovation landscape

3.7.1 Current technological trends

3.7.2 Emerging technologies

3.8 Patent analysis

3.9 Cost breakdown analysis

3.10 Sustainability and environmental aspects

3.10.1 Sustainable practices

3.10.2 Waste reduction strategies

3.10.3 Energy efficiency in production

3.10.4 Eco-friendly Initiatives

3.11 Carbon footprint considerations

3.12 Future outlook and roadmap

3.12.1 Sustainable energy solutions

3.12.2 Cross-industry convergence trends

3.12.3 Regulatory evolution and standards development

3.12.4 Market consolidation and partnership strategies

3.13 Automotive-Grade Solar Semiconductor Supply Chain

3.13.1 Automotive qualification requirements

3.13.2 Long-term supply assurance strategies

3.13.3 Quality management system requirements

3.13.4 Supply chain risk mitigation

3.13.5 Geopolitical impact on solar supply

3.14 Cost-Effectiveness vs Energy Generation Optimization

3.1.1 Solar cell cost per watt analysis

3.14.2 Installation & integration cost factors

3.14.3 Energy payback time calculations

3.14.4 Total cost of ownership models

3.14.5 Performance vs price trade-off analysis

3.15 Automotive Safety Standards & Solar Integration

3.15.1 Electrical safety requirements (iso 6469)

3.15.2 Fire safety & thermal runaway prevention

3.15.3 Crash safety & solar panel behavior

3.15.4 High voltage system integration safety

3.15.5 Emergency response procedures

3.16 Next-Generation Solar Technology Evolution

3.16.1 Perovskite solar cell development

3.16.2 Organic photovoltaic advancement

3.16.3 Transparent solar cell innovation

3.16.4 Flexible solar film evolution

3.16.5 Multi-junction cell integration

3.16.6 Concentrated photovoltaic applications

3.17 Energy Management & Vehicle System Integration