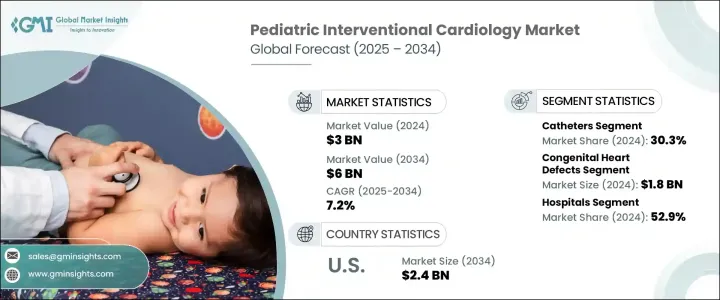

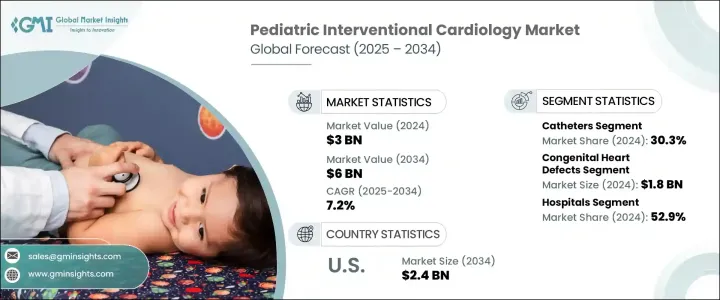

세계의 소아 심혈관 중재시술 시장은 2024년 30억 달러로 평가되었고, 유아의 선천성 심질환 진단 증가에 견인되어 CAGR 7.2%로 성장하며 2034년까지 60억 달러에 이를 것으로 추정되고 있습니다.

의료관계자는 현재 기존의 수술을 대체하는 보다 안전하고 효율적인 저침습 경경 카테터 수술을 널리 채용하고 있습니다. 이 분야의 기술 혁신이 가속화됨에 따라 소형화된 도구와 고급 이미지 시스템을 사용할 수 있게 되어 의사가 합병증이 적은 정확하고 어린이에게 특화된 치료를 실시할 수 있게 되었습니다.

기술 개발은 판막 협착과 중격 기형과 같은 선천성 결핍의 치료 접근법을 변화 시켰습니다. 소아 환자용으로 특별히 설계된 기구는 성인용 기구를 적응한 경우와 비교하여 보다 뛰어난 컨트롤이 가능하며, 수술 성적도 대폭 개선 카테터는 풍선 혈관성형술, 판막성형술, 결손부 폐쇄술 등의 수술을 최소한의 외상과 신속한 회복 시간으로 실시할 수 있도록 지원하는 것으로, 이러한 수술에 있어서 필수적인 것으로 어떤 것에는 변함이 없습니다. 뛰어난 생체 적합성을 갖춘 스티어러블하고 유연한 카테터와 같은 기술 혁신이 신생아와 유아 케어에서 카테터의 보급을 뒷받침하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 30억 달러 |

| 예측 금액 | 60억 달러 |

| CAGR | 7.2% |

2024년 시장 점유율은 카테터 부문이 30.3%로 선두 차세대 소아 전용 카테터에 대한 수요 증가가 이 우위성을 지지하고 있습니다. 기구는 유연성이 향상되고 직경이 작고 생체 적합성이 강화된 설계로 신생아와 유아의 섬세한 혈관계를 보다 안전하게 통과할 수 있도록 되어 있습니다.

선천성 심장 질환 응용 분야는 강화된 신생아 스크리닝 툴에 의한 조기 및 정확한 진단에 힘입어 2024년에 18억 달러를 만들어 냈습니다. 치아의 치료가 많은 CHD 사례의 표준 접근법이 되고 있습니다. 태아 심초음파 검사와 출생 후 진단 도구의 발전으로 임상가는 더 빨리 이상을 발견할 수 있게 되며, 종종 유아기의 초기 단계에서 치료를 계획하고 실시할 수 있습니다.

미국 소아 심혈관 중재시술 2024년 시장 규모는 12억 달러로, 2034년에는 24억 달러에 이를 것으로 예측됩니다. 메디케이드와 민간 의료 보험을 포함한 종합적인 보험 적용으로 최첨단 치료에 대한 액세스가 개선되어 소아를 대상으로 한 심혈관 치료가 세계적으로 확대되고 있습니다.

경쟁 우위를 얻기 위해 Abbott Laboratories, Osypka, Cordis, SMT, Termo, Medtronic, Lifetech Scientific과 같은 기업은 어린이들에게 전문화된 인터벤셔널 툴을 출시하기 위해 연구 개발에 많은 투자를 하고 있습니다. 판매 제휴, 소아 순환기 전문의용의 교육 및 트레이닝 프로그램등이 있습니다. 특주 설계의 카테터 시스템과 폐쇄 기구는 주요한 중점 분야이며, 제품 포트폴리오와 세계 시장에의 리치를 강화하고 있습니다.

The Global Pediatric Interventional Cardiology Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 6 billion by 2034, driven by the rising diagnoses of congenital heart defects among infants. Medical professionals are now widely adopting minimally invasive transcatheter procedures that offer safer and more efficient alternatives to traditional surgery. These modern techniques contribute to better survival rates and faster recovery for pediatric patients, which continues to expand the market. As innovation in this space accelerates, the availability of miniaturized tools and advanced imaging systems enables physicians to conduct precise and child-specific treatments with fewer complications.

Technological development has transformed the approach to treating congenital defects like valve stenosis and septal malformations. Rather than relying on invasive open-heart procedures, healthcare providers now favor catheter-based interventions tailored to pediatric anatomical requirements. Devices designed specifically for young patients offer better control and significantly improve procedural outcomes compared to adapted adult tools. Catheters remain essential in these interventions, helping clinicians perform tasks such as balloon angioplasty, valvuloplasty, defect closure with minimal trauma and quicker recovery times. Innovations like steerable, highly flexible catheters with superior biocompatibility drive their widespread adoption in neonatal and infant care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $6 Billion |

| CAGR | 7.2% |

The catheters segment led the market with a 30.3% share in 2024. Increasing demand for next-generation pediatric-specific catheters supports this dominance. The ability to minimize surgical complexity and shorten hospital stays continues to make these tools a preferred choice among specialists. These devices are designed with improved flexibility, smaller diameters, and enhanced biocompatibility, allowing safer navigation through delicate vascular systems in neonates and infants. Their precision supports interventions, from balloon valvuloplasty to defect closures, all while reducing trauma and recovery time.

The congenital heart defects application segment generated USD 1.8 billion in 2024, supported by earlier and more accurate diagnosis through enhanced neonatal screening tools. Timely intervention through non-surgical methods contributes to improved infant survival, making catheter-based treatments the standard approach for many CHD cases. Advancements in fetal echocardiography and postnatal diagnostic tools allow clinicians to detect abnormalities sooner, often enabling procedures to be planned and performed in early infancy.

U.S. Pediatric Interventional Cardiology Market stood at USD 1.2 billion in 2024 and is expected to reach USD 2.4 billion by 2034. The U.S. benefits from an advanced network of pediatric specialty hospitals and academic centers that conduct high volumes of interventional cardiology procedures. Comprehensive insurance coverage, including Medicaid and private health plans, improves access to cutting-edge treatments and expands the reach of pediatric-focused cardiovascular services globally.

To gain a competitive edge, companies like Abbott Laboratories, Osypka, Cordis, SMT, Terumo, Medtronic, and Lifetech Scientific are investing heavily in R&D to launch pediatric-specific interventional tools. Key strategies include regulatory approvals for new device types, international distribution partnerships, and education & training programs for pediatric cardiologists. Custom-designed catheter systems and closure devices are a major focus area, enhancing product portfolios and market reach globally.