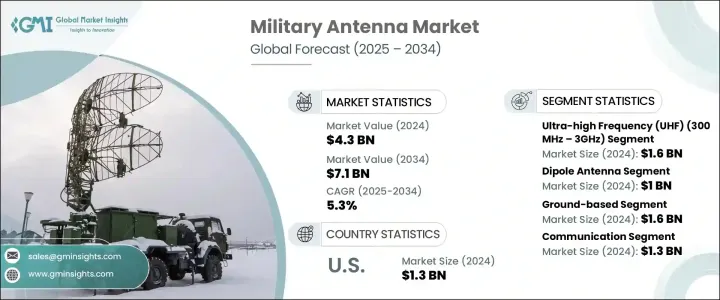

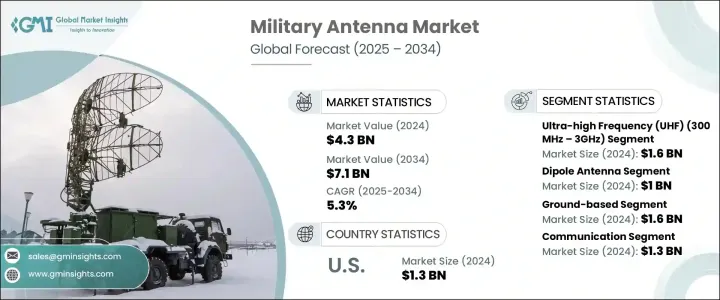

세계의 군용 안테나 시장은 2024년에는 43억 달러로 평가되었고, CAGR 5.3%로 성장할 전망이며, 2034년에는 71억 달러에 이를 것으로 추정됩니다.

현대의 군사 작전에서는 육지, 하늘, 바다의 각 영역에서 신속하고 안전한 통신이 요구됩니다. 상호 운용성, 암호화, 멀티 도메인 통합에 대한 주목이 높아지는 가운데 세계 각국의 정부는 선진적인 안테나 시스템에 대한 투자를 가속화하고 있습니다. 이러한 기술은 실시간 전장 조정, 원격 무기 시스템, 위성 통신을 지원합니다. 또한 진화하는 지정학적 긴장과 군사 현대화 프로그램은 고성능의 미션 크리티컬 통신 컴포넌트에 크게 의존하는 선진적 플랫폼 조달에 박차를 가하고 있습니다.

미국의 정책 결정도 시장 상황의 형성에 큰 역할을 하고 있습니다. 트럼프 행정부 하에서 중국산 전자기기에 부과된 관세는 세계 공급망에 큰 영향을 미쳤습니다. RF 모듈, 커넥터, 회로 기판 등 필수 부품의 비용은 상승하여 생산 일정을 압박했습니다. 미국 내 국방 도급업체는 조달 지연과 비용 상승에 직면하여 국내 공급업체와 동맹국의 제조 파트너십으로 축을 옮길 수밖에 없게 되었습니다. 원래의 목적은 국가 안보와 국내 능력을 높이는 것이었지만, 이러한 행동은 일시적으로 중요한 군용 부품에 대한 접근을 방해하고 국제 의존의 취약성을 부각시켰습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 43억 달러 |

| 예측 금액 | 71억 달러 |

| CAGR | 5.3% |

주파수 부문 내에서 초고주파(UHF) 안테나가 16억 달러의 평가 금액으로 2024년 시장을 선도했습니다. 이러한 안테나는 특히 밀집된 지형이나 복잡한 도시경관과 같은 신호의 장애물이 있는 지역으로 고기동 군사통신 시스템에서 그 신뢰성 때문에 널리 채택되고 있습니다. 그 운용상의 유연성과 중단거리 통신 요구와의 호환성은, 복수의 플랫폼으로 수요를 계속 견인하고 있습니다. 게다가 주파수 프로토콜의 표준화가 UHF 기술에 대한 새로운 투자를 재촉하고 있습니다.

제품 유형별로는 다이폴 안테나가 톱으로, 2024년의 매출은 10억 달러였습니다. 다이폴 안테나는 심플한 설계, 무지향성 방사, 폭넓은 주파수 호환성에 의해 모바일 및 지상 기반의 군사 플랫폼에 통합된 통신 시스템으로 바람직한 선택지가 되고 있습니다. 또, 이러한 안테나는 비용 효율이 높고 통합이 용이하기 때문에 오랜 시스템과 새로운 배치를 지원합니다.

독일의 군용 안테나 시장은 2024년에 2억 4,340만 달러를 창출했으며, 소프트웨어 정의 및 복수 규격의 통신 아키텍처에 중점을 두게 되어, 어댑티브하고 안전한 안테나 시스템에 대한 왕성한 수요를 만들어 냈습니다. 이러한 진화는 고성능의 주파수 적응성이 높은 안테나가 실시간 상황 인식과 상호 운용성에 필수적인 공중 및 지상의 방위 플랫폼의 현대화 노력에 의해 촉진되고 있습니다. 디지털 전장 능력 및 전자전의 회복력 강화를 위한 추진력은 선진 안테나 기술의 국내 연구 개발을 뒷받침하고 있습니다.

세계의 군용 안테나 시장의 주요 기업은 시장에서의 지위를 확보하기 위해 기술 혁신, 파트너십, 제품 확대에 주력하고 있습니다. 록히드 마틴과 RTX는, 미래의 전투 환경에 대응하는 고도 통신 시스템에 고액의 투자를 실시하고 있습니다. Thales와 BAE Systems는 상호운용성과 모듈성을 지원하기 위해 제품 라인을 확대하고 있습니다. Viasat와 L3 Harris Technologies는 위성 기반 안테나 포트폴리오를 강화하고 있습니다. 한편, 코브햄 어드밴스드 일렉트로닉 솔루션스와 로데 슈워츠는 생산 효율을 높이기 위해 전략적 파트너십을 맺고 있습니다. MTI 무선 엣지와 앤트컴은 전술적인 요구에 부응하는 컴팩트하고 견고한 안테나 시스템을 개발하고 있습니다.

The Global Military Antenna Market was valued at USD 4.3 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 7.1 billion by 2034, driven by the rising defense spending across multiple regions, as well as a surge in the deployment of unmanned systems. Modern military operations demand rapid, secure communication across land, air, and sea domains-requirements that make antennas central to mission success. With increased focus on interoperability, encryption, and multi-domain integration, governments worldwide are accelerating investments in advanced antenna systems. These technologies support real-time battlefield coordination, remote weapon systems, and satellite communications. Furthermore, evolving geopolitical tensions and military modernization programs fuel the procurement of advanced platforms that rely heavily on high-performance, mission-critical communication components.

U.S. policy decisions have also played a major role in reshaping the market landscape. Tariffs imposed on Chinese electronics under the Trump administration significantly impacted global supply chains. Costs of essential components like RF modules, connectors, and circuit boards escalated, straining production timelines. Defense contractors within the United States faced procurement delays and rising expenses, which forced a pivot toward domestic suppliers and allied manufacturing partnerships. While the original goal was to boost national security and domestic capability, these actions temporarily disrupted access to critical military-grade parts, highlighting the vulnerability of international dependency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.3 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 5.3% |

Among the frequency segments, ultra-high frequency (UHF) antennas led the market in 2024 with a valuation of USD 1.6 billion. These antennas are widely adopted for their reliability in high-mobility military communication systems, particularly in areas with signal obstruction like dense terrain or complex urban landscapes. Their operational flexibility and compatibility with short-to-mid-range communication needs continue to drive demand across multiple platforms. Additionally, standardized frequency protocols are encouraging further investment in UHF technologies.

Dipole antennas topped the product type segment, generating revenues of USD 1 billion in 2024. Their simple design, omnidirectional radiation, and broad frequency compatibility make them a preferred option in communication systems integrated into mobile and ground-based military platforms. These antennas are also cost-efficient and easy to integrate, supporting long-standing systems and new deployments.

Germany Military Antenna Market generated USD 243.4 million in 2024, driven by advancing its focus on software-defined and multi-standard communication architectures, creating robust demand for adaptive and secure antenna systems. This evolution is fueled by modernization efforts across both aerial and terrestrial defense platforms, where high-performance, frequency-agile antennas are essential for real-time situational awareness and interoperability. The push toward digital battlefield capabilities and enhanced electronic warfare resilience encourages domestic R&D in advanced antenna technologies.

Leading companies in the Global Military Antenna Market focus on innovation, partnerships, and product expansion to secure their market position. Lockheed Martin and RTX invest heavily in advanced communication systems for future combat environments. Thales and BAE Systems are expanding their product lines to support interoperability and modularity. Viasat and L3Harris Technologies are strengthening their satellite-based antenna portfolios. Meanwhile, Cobham Advanced Electronic Solutions and Rohde & Schwarz are forming strategic partnerships to increase production efficiency. MTI Wireless Edge and Antcom are developing compact, rugged antenna systems to meet tactical demands.