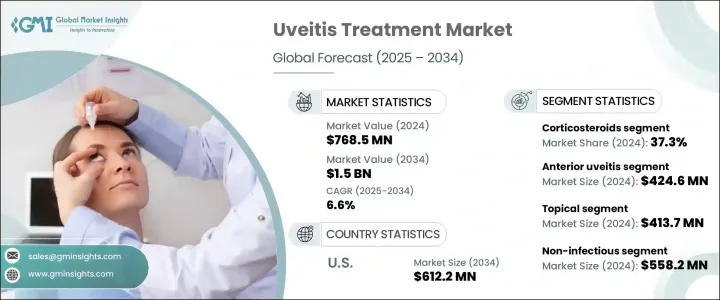

세계의 포도막염 치료 시장은 2024년 7억 6,850만 달러로 평가되었으며 CAGR 6.6%로 성장해 2034년까지 15억 달러에 이를 것으로 추정됩니다.

이 성장의 주요 요인은 루푸스, 크론 병, 류마티스 관절염과 같은자가 면역 질환의 이환율 증가이며, 특히 감염되지 않은 포도막염의 유병률 증가에 기여합니다. 한쪽 눈 또는 두 눈에 영향을 미칠 수 있으며 적절하게 관리되지 않으면 백내장, 녹내장 또는 영구적인 시력 저하와 같은 심각한 합병증을 유발할 수 있습니다.

포도막염 치료에는 염증을 조절하고 장기간 안구장애를 예방하는 것이 포함됩니다. 즉, 즉각적인 완화와 장기 관리를 모두 제공하는 약물에 대한 수요가 급증하고 있습니다. 자기면역 질환이 눈 염증을 일으키는 메커니즘에 대한 이해가 깊어짐에 따라 보다 전문적이고 효과적인 치료 옵션이 늘어났습니다. 증상 완화와 근본적인 질병 통제를 모두 통합하는 이 종합적인 접근법은 건강 관리 제공업체가 더 나은 치료를 제공하는 데 도움이되는 동시에 시장의 상승 궤도를 지원합니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 6,850만 달러 |

| 예측 금액 | 15억 달러 |

| CAGR | 6.6% |

치료 유형별로 분류하면 2024년에는 부신피질 스테로이드제이 시장의 37.3%를 차지했으며, 최대 매출 점유율을 차지했습니다. 주사약 등 여러 복용 형태가 있기 때문에 헬스케어 전문가는 개별 환자의 상태나 반응에 따라 치료 계획을 적응시킬 수 있습니다.

질병 유형별로는 전부 포도막염이 2024년 매출액 4억 2,460만 달러로 압도적인 점유율을 차지하고 있습니다. 스테로이드성 항염증제도 포함한 치료 옵션에 대한 수요는 중대합니다. 중증도나 환자의 요구에 따라 다양한 경로로 이러한 약제를 투여할 수 있는 것이, 보다 좋은 치료 성적에 기여해, 시장의 성장을 뒷받침하고 있습니다 재연을 억제해, 재발을 예방하기 위해서 표적 요법을 선택해 의사

약물 투여 방법에 따르면 국소 치료는 2024년 매출 4억 1,370만 달러로 시장을 선도하고 있습니다. 특히 헬스케어 예산이 제한되어 있는 지역에서는 비용 효과도 중요한 역할을 합니다.

병인별로는 비감염성 포도막염이 시장을 석권해, 2024년의 매출은 5억 5,820만 달러에 이르렀습니다. 이 분야는 자가면역 질환 증가에 대응해 확대를 계속하고 있습니다. 학적 제형의 진보는 염증의 근본 원인을 보다 정확하게 노릴 수 있게 되어, 보다 적은 부작용으로 더 나은 대조를 할 수 있게 되었습니다.

유통 채널별로는 병원 약국이 2024년 매출액 3억 2,910만 달러로 시장을 선도했습니다. 이러한 시설은 복잡한 치료 관리, 주사제 투여, 잠재적인 부작용에 대한 환자 모니터링에 필요한 인프라를 갖추고 있습니다.

미국 시장만으로도 대폭적인 성장이 예상되며, 2034년 시장 규모는 6억 1,220만 달러에 이를 것으로 추정되고 있습니다. 전자 기반의 치료제 등 주요 기업이 치료 성적 향상과 시장 점유율 확대를 위한 기술 혁신에 주력하고 있기 때문에 시장 내 경쟁 역학은 격화하고 있습니다.

The Global Uveitis Treatment Market was valued at USD 768.5 million in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 1.5 billion by 2034. This growth is fueled primarily by the increasing incidence of autoimmune disorders such as lupus, Crohn's disease, and rheumatoid arthritis, which contribute to a higher prevalence of uveitis-particularly the non-infectious types. Uveitis is an inflammatory condition affecting the uvea, the middle layer of the eye, and may result from infections, immune system disorders, or inflammatory diseases. It can impact one or both eyes and, if not properly managed, may cause serious complications like cataracts, glaucoma, or even permanent vision loss.

Treating uveitis involves controlling inflammation and preventing long-term ocular damage. As the condition varies widely in severity and origin, therapies must be tailored accordingly. The market has seen a surge in demand for medications that offer both immediate relief and long-term management. Increased awareness, better diagnostics, and the development of targeted therapies have contributed to market expansion. In particular, the growing understanding of how autoimmune diseases trigger ocular inflammation has led to more specialized and effective treatment options. Innovations in treatment delivery-like localized therapies that reduce systemic side effects-are also gaining traction. This comprehensive approach, which incorporates both symptom relief and underlying disease control, is helping healthcare providers offer better care while supporting the market's upward trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $768.5 Million |

| Forecast Value | $1.5 Billion |

| CAGR | 6.6% |

When categorized by treatment type, corticosteroids commanded the largest revenue share in 2024, accounting for 37.3% of the market. These drugs are highly effective at rapidly reducing inflammation, making them a first-line treatment for many patients with both acute and chronic uveitis. They are available in multiple forms including topical, oral, and injectable, allowing healthcare professionals to adapt treatment plans based on the individual's condition and response. Continued use of corticosteroids in chronic cases ensures ongoing demand and reinforces their role in preventing complications like intraocular pressure increase and optic nerve damage.

In terms of disease type, anterior uveitis emerged as the dominant segment with revenue of USD 424.6 million in 2024. It is the most frequently diagnosed form, comprising 40% to 50% of all uveitis cases. Given its prevalence, especially in younger adults, there is significant demand for treatment options that include not only corticosteroids but also immunosuppressants and NSAIDs. The ability to administer these medications through various routes-depending on severity and patient needs-contributes to better outcomes and drives market growth. Physicians are increasingly choosing targeted therapies to reduce flare-ups and prevent recurrence.

Based on how the drugs are administered, topical treatments led the market with revenue of USD 413.7 million in 2024. Eye drops containing corticosteroids and NSAIDs are widely used due to their targeted action, which helps minimize systemic side effects associated with oral or injectable drugs. Their cost-effectiveness also plays a key role, particularly in regions with limited healthcare budgets. Topical formulations are easier to use and more accessible for patients, which encourages better adherence to treatment protocols.

Looking at disease etiology, non-infectious uveitis dominated the market with revenue reaching USD 558.2 million in 2024. This segment continues to expand in response to the rising number of autoimmune conditions. Many of these diseases have ocular manifestations that require long-term management. Recent advances in immunosuppressive and biologic therapies have made it possible to target the root cause of inflammation more precisely, offering better control with fewer adverse effects. These treatments are especially important in cases where corticosteroids are insufficient or lead to significant side effects.

In the distribution channel segment, hospital pharmacies led the market with USD 329.1 million in revenue in 2024. The increasing use of biologics and immunosuppressive agents-which often require specialized handling and close monitoring-has elevated the role of hospital pharmacies. These facilities are equipped with the infrastructure needed to manage complex therapies, administer injectables, and monitor patients for potential adverse reactions. Investments in pharmacy services across hospitals are enabling more comprehensive care for those living with chronic or severe uveitis.

The U.S. market alone is projected to grow substantially, with forecasts estimating a total market size of USD 612.2 million by 2034. Regulatory support, particularly the timely approval of new therapies by relevant health authorities, plays a pivotal role in ensuring patients gain access to cutting-edge treatments. Competitive dynamics within the market are intensifying as key players focus on innovation-such as biologic agents, steroid-releasing implants, and gene-based therapies-to improve therapeutic outcomes and capture a larger market share. Collaborations with research centers and healthcare institutions are becoming more common as companies work to integrate modern technologies, expand global reach, and meet the rising demand for effective, affordable uveitis treatments.