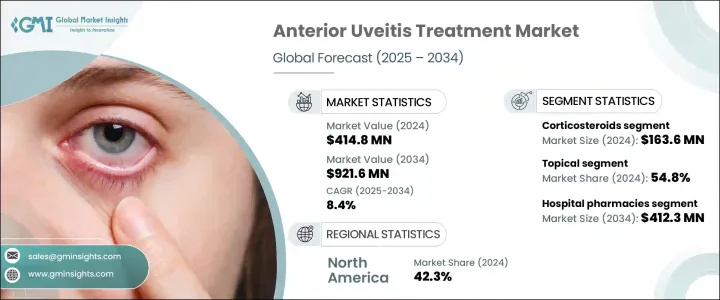

세계의 전부 포도막염 치료 시장은 2024년에는 4억 1,480만 달러로 평가되었고, 2034년에는 CAGR 8.4%로 성장할 전망이며, 9억 2,160만 달러에 이를 것으로 추정됩니다.

이는 전부 포도막염의 자가면역적 및 염증적 기반에 대한 깊은 인사이트가 조기적이고 치밀한 의료 개입의 필요성을 강조하고 있기 때문입니다. 진단 도구와 화상 기술의 진보로 임상의는 보다 신속하고 정확한 평가를 내릴 수 있게 되어 치료 방침의 결정이 가속화되고 있습니다. 자가면역질환이나 감염증의 증가에 따른 환자층의 확대는 신뢰성 높은 치료 접근법에 대한 수요를 더욱 높이고 있습니다.

유전자 검사 및 AI 지원 진단과 같은 기술의 진보는 보다 맞춤 치료 옵션에 대한 길을 열어 의료 제공업체와 제조업체 모두에게 새로운 기회를 제공합니다. 이러한 기술 혁신은 특정 환자의 요구를 보다 정확하게 식별할 수 있게 하여 치료 성과를 높입니다. 게다가 세계 인구의 고령화, 특히 미국에서는 염증성 안질환의 이환율이 상승하고 있어 고령 환자의 요구에 맞춘 특수한 치료법의 수요가 높아지고 있습니다. 이러한 인구 동태의 변화는 염증성 질환의 유병률 증가에 대처하기 위한 표적 치료 개발의 중요성을 강조하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034 |

| 시작 금액 | 4억 1,480만 달러 |

| 예측 금액 | 9억 2,160만 달러 |

| CAGR | 8.4% |

부신피질 스테로이드 약물 부문은 2024년에 1억 6,360만 달러를 창출하였습니다. 그 강력한 항염증 작용과 신속한 증상 완화 능력으로 안염증 관리 및 시력을 위협하는 합병증 예방의 첫 번째 선택약으로서의 역할이 확고해지고 있습니다. 이 약제들은 범용성이 높고 전신용과 국소용 제제가 있으며 염증의 중증도와 부위에 따라 선택됩니다. 부신피질 스테로이드의 전신 투여는 중증 후방염에 자주 사용되고, 국소적인 전방염에는 외용약이 자주 사용됩니다. 이러한 약제는 수십 년에 걸친 유효성 데이터에 힘입어 널리 임상 사용되고 있어 안과 치료의 요체가 되고 있습니다.

코르티코스테로이드 외용제의 2024년 점유율은 54.8%이며, 이는 의료 제공자와 환자 사이의 기호의 고조를 반영하고 있습니다. 국소 투여는 전신 흡수를 최소화하면서 국소적인 치료 효과를 가져와 경구제나 주사제에 비해 부작용 위험을 크게 낮춘다. 이 투여 방법은 특히 전부 포도막염이나 기타 안전염증성 질환에 적합하며 사용 편의성, 신속한 완화, 환자 컴플라이언스 향상을 가져옵니다. 연고제, 겔제, 점안제 등, 다양한 투여 옵션이나 제형을 이용할 수 있게 됨으로써, 편리성이 한층 더 향상되어 애드히어런스율의 향상이나 환자의 전귀의 개선에 기여하고 있습니다.

미국의 전부 포도막염 치료 시장은 2024년에 1억 5,950만 달러에 달했습니다. 이 나라의 강력한 헬스케어 인프라 및 자가면역질환의 높은 유병률이 눈 질환에 대한 관심을 높이고 있습니다. 코르티코스테로이드, 면역억제제, 생물학적 제제 등의 의약품은 여전히 치료 프로토콜의 중심이며, 임상연구에서는 생물학적 제제를 기반으로 한 새로운 선택지의 탐구가 진행되고 있습니다. 원격의료나 디지털 툴에 대한 규제의 개방성은 조기 평가와 지속적 치료에 대한 환자의 접근을 최적화하고 이 지역의 치료 파이프라인 전체를 강화합니다.

세계의 전부 포도막염 치료 시장에서 활약하는 유력 기업은 Pfizer, Aldeyra Therapeutics, Tarsier Pharma, Novartis, Clearside Biomedical, UCB, AbbVie, Amgen, Kiora Pharmaceuticals, Alcon, EyePoint Pharmaceuticals, Sun Pharmaceutical Industries 및 Santen Pharmaceutical 등입니다. 이러한 기업은 전부 포도막염 치료 시장에서의 지위를 강화하기 위해 혁신적인 치료법을 보다 빨리 시장에 도입하고 있습니다. 아이포인트 파마슈티컬스나 암젠 등의 기업은 치료의 유효성과 환자의 편의성을 높이기 위해 선진적인 약물 전달 기술을 우선시하고 있습니다. 화이자와 노바티스 등 대형 제약사와 바이오테크놀로지 혁신기업과의 제휴는 치료 포트폴리오를 확대하는 전략으로 떠오르고 있습니다.

The Global Anterior Uveitis Treatment Market was valued at USD 414.8 million in 2024 and is estimated to grow at a CAGR of 8.4% to reach USD 921.6 million by 2034, driven by deeper insights into the autoimmune and inflammatory underpinnings of anterior uveitis, which underscore the need for early and targeted medical intervention. Advancements in diagnostic tools and imaging technologies are helping clinicians make faster and more accurate assessments, which is accelerating treatment decisions. The expanding patient pool, linked to rising autoimmune and infectious diseases, further fuels demand for reliable therapeutic approaches.

Advancements in technologies such as genetic testing and AI-assisted diagnostics are paving the way for more personalized treatment options, offering new opportunities for both healthcare providers and manufacturers. These innovations allow for more accurate identification of specific patient needs, enhancing treatment outcomes. Furthermore, the aging global population, especially in the U.S., is driving a higher incidence of inflammatory eye conditions, which in turn is fueling the demand for specialized therapies tailored to meet the needs of older patients. This demographic shift underscores the importance of developing targeted treatments to address the growing prevalence of such conditions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $414.8 Million |

| Forecast Value | $921.6 Million |

| CAGR | 8.4% |

The corticosteroids segment generated USD 163.6 million in 2024. Their potent anti-inflammatory properties and ability to deliver rapid symptom relief have cemented their role as the first-line therapy for managing ocular inflammation and preventing vision-threatening complications. These drugs are versatile, available in systemic and topical formulations, and are selected based on the severity and location of inflammation. Systemic corticosteroids are commonly used for severe or posterior segment inflammation, while topical agents remain the go-to option for more localized anterior segment conditions. Their widespread clinical use is supported by decades of efficacy data, making them a cornerstone in ophthalmic care.

The topical corticosteroid segment held a 54.8% share in 2024, reflecting its growing preference among healthcare providers and patients. Topical administration offers a localized therapeutic effect with minimal systemic absorption, significantly lowering the risk of adverse reactions compared to oral or injectable forms. This delivery method is especially suitable for anterior uveitis and other front-of-eye inflammatory disorders, offering ease of use, faster relief, and better patient compliance. The availability of various dosing options and formulations, such as ointments, gels, and eye drops, has further enhanced convenience, contributing to higher adherence rates and improved patient outcomes.

United States Anterior Uveitis Treatment Market reached USD 159.5 million in 2024. The country's strong healthcare infrastructure and high prevalence of autoimmune disorders have amplified attention to ocular diseases. Pharmaceuticals such as corticosteroids, immunosuppressants, and biologics remain central to therapeutic protocols, while clinical research increasingly explores novel biologic-based options. Regulatory openness toward telehealth and digital tools optimizes patient access to early evaluations and ongoing care, strengthening the overall treatment pipeline in the region.

Prominent players active in the Global Anterior Uveitis Treatment Market include Pfizer, Aldeyra Therapeutics, Tarsier Pharma, Novartis, Clearside Biomedical, UCB, AbbVie, Amgen, Kiora Pharmaceuticals, Alcon, EyePoint Pharmaceuticals, Sun Pharmaceutical Industries, and Santen Pharmaceutical. To strengthen their position in the anterior uveitis treatment market, companies such as Clearside Biomedical, Alcon, and Santen Pharmaceutical are heavily investing in research and development to bring innovative therapies to market faster. Players like EyePoint Pharmaceuticals and Amgen prioritize advanced drug delivery technologies to boost treatment efficacy and patient convenience. Collaborations between large pharma firms, including Pfizer and Novartis, with biotech innovators have emerged as a strategy to expand therapeutic portfolios.