Engine Valve Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

상품코드:1716665

리서치사:Global Market Insights Inc.

발행일:2025년 03월

페이지 정보:영문 161 Pages

라이선스 & 가격 (부가세 별도)

ㅁ Add-on 가능: 고객의 요청에 따라 일정한 범위 내에서 Customization이 가능합니다. 자세한 사항은 문의해 주시기 바랍니다.

한글목차

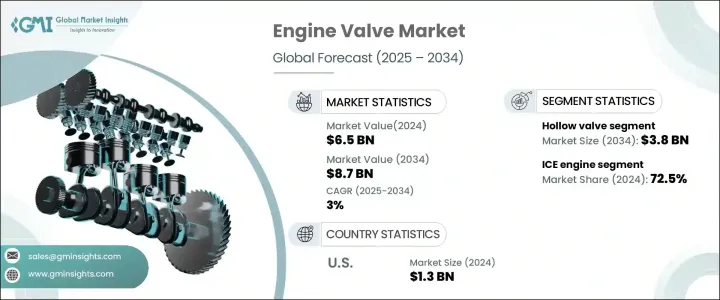

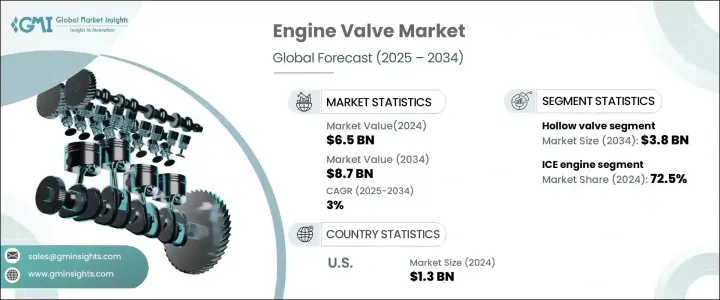

세계의 엔진 밸브 시장은 2024년에는 65억 달러가 되었고, 2025년부터 2034년에 걸쳐 CAGR 3%를 나타낼 것으로 예측되어 꾸준한 성장이 전망되고 있습니다.

저연비 차량에 대한 세계 수요 증가는 시장 확대에 영향을 미치는 주요 요인입니다. 세계 각국 정부가 연비·배가스 규제를 강화하는 가운데 자동차 제조업체는 첨단 엔진 기술을 급속히 도입하고 있습니다. 이 때문에 고성능 엔진 부품, 특히 연소 효율과 배기 가스 제어에서 매우 중요한 역할을 하는 밸브에 대한 수요가 급증하고 있습니다. 터보 과급이나 가변 밸브 타이밍 등 엔진 설계의 혁신이 진행됨에 따라 연료 연소를 최적화하고 차량 전체의 성능을 높이는 정밀 공학 밸브의 요구가 더욱 높아지고 있습니다. 자동차 제조업체가 엄격한 규제 요건을 충족하기 위해 가볍고 내구성이 뛰어난 엔진 부품에 초점을 맞추고 있는 동안, 엔진 밸브 시장은 재료 과학 및 제조 공정에서 현저한 발전을 이루고 있습니다.

시장은 밸브 유형에 따라 중공 밸브, 모노 메탈 밸브, 바이메탈 밸브로 구분됩니다. 이런 밸브는 속도와 열 관리가 중요한 고성능 엔진과 레이싱 엔진에서 특히 유익합니다.

시장 범위

시작 연도

2024년

예측 연도

2025-2034년

시작 금액

65억 달러

예측 금액

87억 달러

CAGR

3%

엔진 유형별로 볼 때 시장은 내연 엔진(ICE)과 전기 엔진으로 분류됩니다. 기술 진보에 의해 계속 리드하고 있습니다. 자동차 제조업체는 가솔린 엔진의 효율을 높이기 위해서, 직접 연료 분사나 기통 휴지 등의 저연비 기술을 도입하고 있습니다.

미국의 엔진 밸브 시장은 2024년에 13억 달러를 창출했고 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 2.4%를 나타낼 것으로 예측되고 있습니다. 자동차의 전동화로의 변화가 가속되고 있음에도 불구하고, 엔진 밸브를 포함한 내연 기관차 부품 수요는 계속 견조입니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 시장 인사이트

생태계 분석

원재료 분석

주요 뉴스와 대처

파트너십/제휴

합병/인수

투자

제품 출시와 혁신

규제 상황

영향요인

성장 촉진요인

자동차 생산 증가

밸브 기술의 혁신

엄격한 배기가스 규제 증가

업계의 잠재적 위험 및 과제

자동차용 밸브 제조 공정에서의 환경 문제

성장 가능성 분석

Porter's Five Forces 분석

PESTEL 분석

무역 분석

수출 데이터

수입 데이터

제4장 경쟁 구도

서론

기업별 시장 점유율

주요 시장 기업의 경쟁 분석

경쟁 포지셔닝 매트릭스

전략 전망 매트릭스

제5장 시장 추계·예측 : 밸브 유형별(2021-2034년)

주요 동향

중공

모노메탈릭

바이메탈

제6장 시장 추계·예측 : 목적별(2021-2034년)

주요 동향

흡기 밸브

배기 밸브

제7장 시장 추계·예측 : 엔진 유형별(2021-2034년)

주요 동향

ICE

전기

제8장 시장 추계·예측 : 재료별(2021-2034년)

주요 동향

니켈 합금

크롬 도금

스테인레스 스틸

기타(질산염, 스텔라이트 합금 등)

제9장 시장 추계·예측 : 기술별(2021-2034년)

주요 동향

공압식

유압식

전기식

제10장 시장 추계·예측 : 용도별(2021-2034년)

주요 동향

자동차

상업차

승용차

이륜차

해양

천연가스엔진

군사 및 방위

농업 및 토목 기계

철도 및 기관차

발전기 및 산업용 엔진

기타

제11장 시장 추계·예측 : 유통 채널별(2021-2034년)

주요 동향

OEM

애프터마켓

제12장 시장 추계·예측 : 지역별(2021-2034년)

주요 동향

북미

미국

캐나다

유럽

영국

독일

프랑스

이탈리아

스페인

아시아태평양

중국

인도

일본

한국

호주

말레이시아

인도네시아

라틴아메리카

브라질

멕시코

중동 및 아프리카

사우디아라비아

UAE

남아프리카

제13장 기업 프로파일

AVR(Vikram) Valves

Bosch

Continental AG

Denso

Eaton Corporation

Federal-Mogul

Fuji Oozx

Grindtech

Hitachi Ltd

Rane

KTH

영문 목차

영문목차

The Global Engine Valve Market, valued at USD 6.5 billion in 2024, is set to experience steady growth, projected to expand at a CAGR of 3% between 2025 and 2034. The increasing global demand for fuel-efficient vehicles is a major factor influencing market expansion. With governments worldwide enforcing stricter fuel economy and emissions regulations, automakers are rapidly adopting advanced engine technologies. This has led to a surge in demand for high-performance engine components, particularly valves, which play a pivotal role in combustion efficiency and emission control. Ongoing innovations in engine design, including turbocharging and variable valve timing, are further boosting the need for precision-engineered valves that optimize fuel combustion and enhance overall vehicle performance. As automakers focus on lightweight and durable engine components to meet stringent regulatory requirements, the engine valve market is witnessing significant advancements in material science and manufacturing processes.

The market is segmented based on valve type into hollow, monometallic, and bimetallic valves. The hollow valve segment accounted for USD 2.9 billion in 2024, gaining traction due to its superior lightweight characteristics. Hollow valves offer a significant advantage over solid valves by enabling faster and more precise valve movement, which enhances engine efficiency. These valves are particularly beneficial in high-performance and racing engines where speed and thermal management are crucial. The ability of hollow valves to improve heat dissipation ensures that engines operate at optimal temperatures, thereby extending the lifespan of engine components subjected to high stress and extreme conditions.

Market Scope

Start Year

2024

Forecast Year

2025-2034

Start Value

$6.5 Billion

Forecast Value

$8.7 Billion

CAGR

3%

In terms of engine type, the market is categorized into internal combustion engines (ICE) and electric engines. ICE engines held a dominant 72.5% share in 2024 and are projected to grow at a CAGR of 2.8% through 2034. While electric vehicles are gradually reshaping the automotive landscape, ICE vehicles continue to lead due to their widespread infrastructure and ongoing technological advancements. Automakers are integrating fuel-efficient technologies such as direct fuel injection and cylinder deactivation to enhance the efficiency of gasoline-powered engines. At the same time, stricter emission norms are driving the development of lightweight, heat-resistant engine valves that minimize emissions without compromising performance.

U.S. Engine Valve Market generated USD 1.3 billion in 2024 and is forecasted to expand at a CAGR of 2.4% from 2025 to 2034. Despite the accelerating shift toward vehicle electrification, the demand for ICE components, including engine valves, remains strong. Automakers in the U.S. are investing in advanced valve materials and coatings that enhance durability and efficiency, ensuring compliance with stringent emission regulations while meeting consumer demand for high-performance gasoline-powered vehicles.

Table of Contents

Chapter 1 Methodology & Scope

1.1 Market scope & definition

1.2 Base estimates & calculations

1.3 Forecast calculation

1.4 Data sources

1.4.1 Primary

1.4.2 Secondary

1.4.2.1 Paid sources

1.4.2.2 Public sources

Chapter 2 Executive Summary

2.1 Market 3600 synopsis, 2021 - 2034

2.2 Business trends

2.3 Regional trends

2.4 Product type trends

2.5 End use trends

2.6 Distribution channel trends

Chapter 3 Market Insights

3.1 Industry ecosystem analysis

3.2 Raw material analysis

3.3 Key news and initiatives

3.3.1 Partnership/Collaboration

3.3.2 Merger/Acquisition

3.3.3 Investment

3.3.4 Product launch & innovation

3.4 Regulatory landscape

3.5 Impact forces

3.5.1 Growth drivers

3.5.1.1 Increase production of vehicles

3.5.1.2 Increase innovation in valve technology

3.5.1.3 Rise in stringent emission regulations

3.6 Industry pitfalls & challenges

3.6.1.1 Manufacturing process of automotive valves involves environmental concerns

3.7 Growth potential analysis

3.8 Porter's analysis

3.9 PESTEL analysis

3.10 Trade analysis

3.10.1 Export data

3.10.2 Import data

Chapter 4 Competitive Landscape, 2024

4.1 Introduction

4.2 Company market share, 2024

4.3 Competitive analysis of major market players, 2024

4.4 Competitive positioning matrix, 2024

4.5 Strategic outlook matrix, 2024

Chapter 5 Market Estimates & Forecast, By Valve Type 2021 - 2034, (USD Billion)