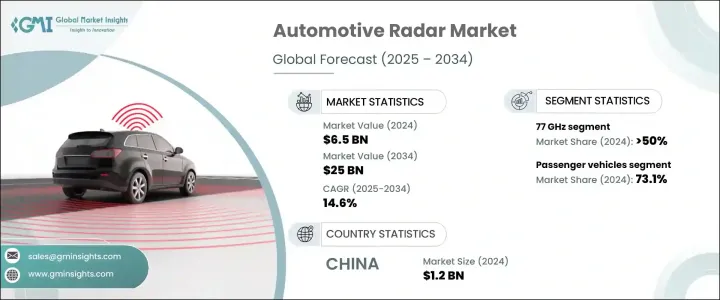

세계의 자동차용 레이더 시장은 2024년 65억 달러의 평가 금액에 이르렀으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 14.6%로 확대될 것으로 예측됩니다.

이 성장은 4D 이미징 그레이더, 디지털 빔포밍, AI 탑재 레이더 처리 등의 기술 혁신을 포함한 레이더 기술의 지속적인 진보에 의해 초래됩니다.

OTA(Over-the-Air) 소프트웨어 업데이트를 통해 차량은 레이더 기능의 업그레이드를 받을 수 있게 되어, 보급이 더욱 가속화되고 있습니다. 커넥티드 자동차가 증가함에 따라 업계는 단일 자동차 레이더 센서에서 다른 자동차, 인프라 및 클라우드 기반 시스템과의 실시간 통신을 용이하게 하는 통합 차량 네트워크로 전환하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 65억 달러 |

| 예측 금액 | 250억 달러 |

| CAGR | 14.6% |

주파수별로는 24GHz, 77GHz, 79GHz 레이더로 분류됩니다. 77GHz 부문은 2024년에 50% 이상의 최대 시장 점유율을 차지했습니다. 유럽과 북미의 규제와 정책에 따라 77GHz 레이더가 새로운 업계 표준으로 확립되어 중국에서는 모든 신차에 고주파 레이더 시스템의 탑재를 의무화하는 최근의 정책 변경으로 아시아태평양에서의 채용이 가속화되고 있습니다.

시장은 승용차와 상용차로 구분되며, 2024년 점유율은 승용차가 73.1%를 차지했습니다. 사각 감지 및 적응형 크루즈 컨트롤과 같은 기술은 규제 프레임 워크 및 안전 평가 시스템을 업데이트하는 데 도움이 되며 개인 소유 자동차에 표준으로 장착됩니다. 세계 정부가 보다 엄격한 가이드라인을 시행해, 충돌 회피와 탑승자 보호의 기준에 준거하기 위해 고주파 레이더가 필요 불가결이 되고 있습니다.

범위는 중거리 레이더(MRR), 단거리 레이더(SRR), 장거리 레이더(LRR)로 나뉘며, 2024년에는 MRR이 우위를 차지했습니다. 도시가 스마트 교통 시스템을 확대해, 라이드 헤일링 플릿, 전기자동차, 라스트 마일 딜리버리 서비스는 교통량이 많은 환경에서 안전한 네비게이션을 위해 MRR을 통합하는 경우가 늘어나고 있습니다.

또한 시장은 판매 채널별로 OEM과 애프터마켓으로 분류됩니다. 대기업 제조업체는 레이더 기술 프로바이더와 제휴하여 고급차와 중급차 모두에서 ADAS 기능의 대규모 전개를 가능하게 하고 있습니다.

아시아태평양은 세계 자동차용 레이더 시장을 선도하고 있으며, 2024년에는 중국에서만 12억 달러를 차지했습니다. 고속도로 시스템을 추진하는 정부의 이니셔티브가 강력하게 지원하고 있습니다. 신에너지 차량(NEV)에 레이더 채용을 장려하는 호의적인 정책에 의해 이 지역은 자동차 레이더 기술 혁신의 최전선에 위치하고 있습니다.

The Global Automotive Radar Market reached a valuation of USD 6.5 billion in 2024 and is projected to expand at a CAGR of 14.6% from 2025 to 2034. This growth is driven by the continuous advancement of radar technology, including innovations such as 4D imaging radar, digital beamforming, and AI-powered radar processing. These enhancements are improving range, resolution, and interference suppression, making radar systems more effective for advanced driver assistance systems (ADAS) and autonomous driving.

Over-the-air (OTA) software updates are allowing vehicles to receive radar capability upgrades, further accelerating adoption. The rise of electric and connected vehicles is also fueling demand, as radar technology plays a crucial role in safety features like blind spot monitoring, adaptive cruise control, and automated parking. With the increasing number of connected vehicles, the industry is transitioning from standalone radar sensors to integrated vehicle networks that facilitate real-time communication with other cars, infrastructure, and cloud-based systems. Strict safety regulations across key regions are further pushing automakers to implement radar-based solutions as standard features in their models.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $25 Billion |

| CAGR | 14.6% |

By frequency, the market is categorized into 24 GHz, 77 GHz, and 79 GHz radar. The 77 GHz segment held the largest market share of over 50% in 2024. Its widespread adoption is driven by its superior resolution and longer detection range, which are essential for critical safety features like lane-keeping assistance and automated emergency braking. Regulations in Europe and North America have established 77 GHz radar as the new industry standard, and recent policy changes in China mandating high-frequency radar systems in all new cars are accelerating adoption in the Asia Pacific region.

The market is segmented into passenger and commercial vehicles, with passenger cars holding a 73.1% share in 2024. Growing consumer preference for enhanced safety features has led to the widespread integration of radar-based driver assistance systems. Technologies such as blind spot detection and adaptive cruise control are becoming standard in personal vehicles, driven by regulatory frameworks and updated safety rating systems. Governments worldwide are enforcing stricter guidelines, making high-frequency radar a necessity for compliance with crash avoidance and occupant protection standards. Automakers are leveraging radar technology to enhance self-driving capabilities, particularly in Level 2 and Level 3 autonomous vehicles, where features like highway pilot and automated lane changes rely on high-precision radar sensors.

In terms of range, the market is divided into medium-range radar (MRR), short-range radar (SRR), and long-range radar (LRR), with MRR dominating in 2024. Its importance is growing in urban mobility, where self-parking and collision avoidance require 360-degree situational awareness. As cities expand smart transportation systems, ride-hailing fleets, electric vehicles, and last-mile delivery services are increasingly integrating MRR for safe navigation in high-traffic environments. The rise of intelligent transportation systems (ITS) is further driving adoption, as radar sensors play a key role in real-time traffic monitoring, predictive analytics, and accident prevention.

The market is also classified by sales channel into OEMs and aftermarket. In 2024, the OEM segment held the dominant share as automakers continued integrating radar systems directly into new vehicle models. Leading manufacturers are collaborating with radar technology providers to enable large-scale deployment of ADAS features in both luxury and mid-range vehicles. As consumer awareness of vehicle safety grows, automakers are increasingly including radar-based solutions as standard rather than optional features.

The Asia Pacific region leads the global automotive radar market, with China alone accounting for USD 1.2 billion in 2024. Investments in autonomous driving, AI-powered sensors, and vehicle electrification are driving growth, with strong support from government initiatives promoting smart transportation and intelligent highway systems. Favorable policies encouraging radar adoption in new energy vehicles (NEVs) are positioning the region at the forefront of innovation in automotive radar technology.